Why we recommend short-selling... A study in protecting your portfolio... How we've fared in Stansberry's Investment Advisory... Don't miss our presentation from famed short-seller Andrew Left...

Porter often says that his Friday Digests generate waves of cancellation requests on Mondays. Today, I (Bryan Beach) may break the record…

Porter often says that his Friday Digests generate waves of cancellation requests on Mondays. Today, I (Bryan Beach) may break the record…

That's because I'm going to cover what is perhaps the most unpopular advice we give at S&A. It sparks as much angry feedback as anything we write. And for a company whose founder has had a subscriber threaten to punch him in the mouth – that's saying something…

It's a topic that has many of you questioning the sanity of the Stansberry's Investment Advisory team...

Today, I'm going to talk about short-selling.

For the uninitiated, short-selling means you profit when a company's share price falls. To open the trade, you borrow shares and sell them into the market. To close the trade, you buy back shares.

In our flagship newsletter Stansberry's Investment Advisory, we continue to recommend using a portion of your portfolio to short stocks... which may seem crazy at the height of a six-year raging bull market.

The results of our recent short-selling have been less than stellar. One subscriber recently called our short portfolio "a stinkfarm of epic proportions."

Here are all of our short recommendations since 2012. You can see what he's talking about…

|

Recommendation

|

Open Date

|

Status

|

Duration

|

Return

|

|

iShares 20+ Yr Treasury Fund (TLT)

|

Jan. '12

|

Closed

|

27 mo.

|

0.9%

|

|

Consol Energy (CNX)

|

June '12

|

Stopped out

|

2 mo.

|

-19.4%

|

|

Canadian Oil Sands (COS.TO)

|

Sept. '12

|

Stopped out

|

19 mo.

|

-11.1%

|

|

Hewlett-Packard (HPQ)

|

May '13

|

Stopped out

|

2 mo.

|

-23.3%

|

|

Salesforce (CRM)

|

June '13

|

Stopped out

|

2 mo.

|

-31.2%

|

|

Suncor (SU)

|

July '13

|

Closed

|

9 mo.

|

-15.8%

|

|

J.C. Penney (JCP)

|

Aug. '13

|

Stopped out

|

3 mo.

|

31.1%

|

|

Simon Property Group (SPG)

|

Feb. '14

|

Open

|

6 mo.

|

-16.5%

|

|

General Motors (GM)

|

March '14

|

Closed

|

1 mo.

|

2.3%

|

|

GameStop (GME)

|

May '14

|

Stopped out

|

3 mo.

|

-7.7%

|

|

Tesla Motors (TSLA)

|

June '14

|

Stopped out

|

2 mo.

|

-25.3%

|

We understand that real subscribers lost real money on average by following these short recommendations. And no one hates booking losses as much as we do.

But I want to take a step back and remind readers why we short… And why we don't worry about taking losses along the way.

We've been advocating shorting stocks as a form of "portfolio insurance" for years. Back in December 2006, Porter explained...

|

A couple months later, in the February 2007 issue, he elaborated on the "shorts as a hedge" concept...

|

As you can see, our short strategy is not designed to make big money consistently... but rather, to guard against broad-market downturns. That's why we call short-selling "portfolio insurance"... and success is measured as doing "a little better than breakeven" with your short picks.

Think about it... If you can break even on a series of trades that protect your overall portfolio from a broad market selloff, why wouldn't you? Makes sense. But… does it really work out that way?

We've written about this strategy for years. Today, we're going to look at the data. Over the past 15 years, has the Stansberry's Investment Advisory portfolio been able to break even by shorting? Has short-selling actually protected us from broad market pullbacks? In other words... does the "short-selling is portfolio insurance" strategy actually hold up?

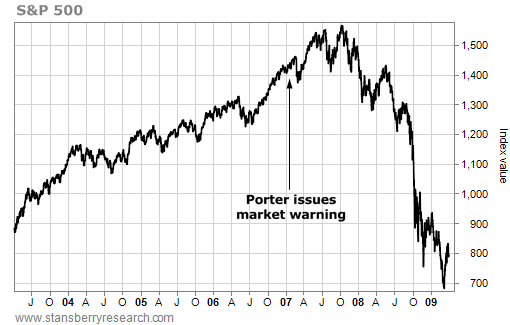

To answer these questions, we are going to use the actual track record from the Stansberry's Investment Advisory portfolio. We have painstakingly compiled this over the past several months. To start off, let's take a look at the broad market from when Stansberry's Investment Advisory was launched in September 1999 to last month.

Two parts of this chart are particularly noteworthy. First, look at the arrows. When our indicators tell us that the market is pervasively bullish, we step up our short-selling as additional portfolio insurance. These arrows reflect those calls.

Second, note that there have been five broad-market trends over the period we're evaluating: three bull markets and two bear markets. As we've written many times, it's difficult to make money short-selling during bull markets... but when the market drops, you'll be glad you have that short exposure.

In a sense, you can think of bull markets as periods when we're "paying premiums" on this portfolio insurance. While bear markets are when we reap the benefits of our short exposure... In essence, that's when we "collect" on our insurance policies.

That's why it makes sense to evaluate an entire insurance cycle, covering both the bull market (when you pay your premiums) and the bear market (when you collect on your policy)...

Here's a chart of the first insurance cycle, covering the bull market from 1999 through the end of the bear market in late 2003.

In the October 2000 issue of Stansberry's Investment Advisory, Porter wrote...

|

In hindsight, the timing of the warning was spot on. (As you'll see, our predictions aren't always so prescient.) And the Stansberry's Investment Advisory portfolio actually had already been shorting prior to this market call.

Regardless, let's see what happened to our shorts over this bull/bear insurance "cycle"...

|

Type

|

Open Date

|

Close Date

|

Avg Return

|

Avg Return

(Long Only)

|

|

Bull

|

Sept. '99

|

Sept. '00

|

-9.7%

|

-8.2%

|

|

Bear

|

Oct. '00

|

March '03

|

-4.9%

|

-9.9%

|

|

* All returns are on an annualized basis.

|

||||

The "Average Return" column shows average annualized returns for all the Stansberry's Investment Advisory recommendations made during that period, including all short picks. The last column, "Average Return (Long Only)," is a hypothetical portfolio that ignores our short recommendations. (We tend to hold short positions for less time than our long positions, which skews the data. Using annualized returns minimizes this imbalance.)

As you can see, adding shorts to our portfolio during the bull market "cost" us about 1.5 percentage points in returns (a 9.7% loss versus an 8.2% loss). However, those short positions really saved us when the bear market arrived. Having shorts in our portfolio from October 2000 to March 2003 (including those added during the bear market) "paid" us an additional five percentage points (-4.9% versus -9.9%).

And while Stansberry's Investment Advisory underperformed the broader market during the tail end of the bull market (a "stub period" covering only the period after Stansberry's Investment Advisory was launched), having portfolio insurance helped us minimize losses during the broader-market downturn. Stansberry's Investment Advisory picks throughout the bear market ultimately lost "only" 5%, during a period when the broader market fell 17%.

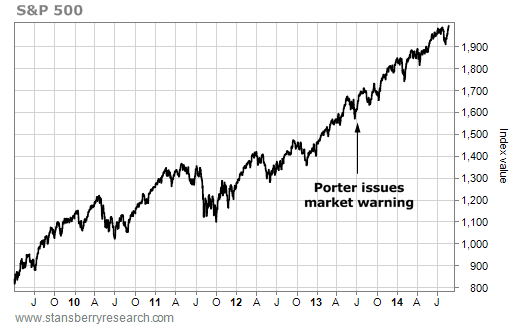

These results are interesting. But the much more telling data will come from the next bear/bull market cycle. Unlike the first cycle, Stansberry's Investment Advisory made recommendations throughout this entire period...

In the February 2007 issue of Stansberry's Investment Advisory, Porter warned...

|

The market peaked eight months later. The following table summarizes the results of Stansberry's Investment Advisory recommendations during this bull/bear cycle...

|

Type

|

Open Date

|

Close Date

|

Average Return

|

Average Return

(Long Only)

|

|

Bull

|

April '03

|

Sept. '07

|

14.7%

|

16.3%

|

|

Bear

|

Oct. '07

|

March '09

|

20.6%

|

13.7%

|

|

* All returns are on an annualized basis.

|

||||

14.7%... versus 16.3% for the hypothetical "long only" portfolio. Including shorts cost about 1.6 percentage points in annualized returns.

However, as expected, having a short strategy in place really paid off during the bear market, and boosted annualized returns by nearly seven percentage points (20.6% versus 13.7%).

When reviewing the numbers above, remember… from late 2007 to early 2009, the market fell 33%, while the recommendations we made during that period ultimately posted healthy gains.

This leads us back to where we started... The frustrating performance of our recent short recommendations. As you can see, we are right in the middle of a six-year bull market, with no end in sight...

We devoted the June 2013 issue to various market warning signs flashing around the world, which we responded to by trimming our portfolio and increasing our short exposure in the subsequent months. Here's what we wrote...

|

In hindsight, we were obviously way early on this call. (Somewhere, my friends and colleagues Dr. David "Doc" Eifrig and Steve Sjuggerud are smiling. Both called for the bull market to keep on going.) Our portfolio insurance "premiums" may well end up costing more during this bull market. The following table summarizes how effective the "short-selling as portfolio insurance" strategy is playing out, including the recent poor results...

|

Type

|

Open Date

|

Close Date

|

Avg Return

|

Avg Return

(Long Only)

|

Insurance Benefit

(Cost) |

|

Bull

|

Sept. '99

|

Sept. '00

|

-9.7%

|

-8.2%

|

-1.5%

|

|

Bear

|

Oct. '00

|

March '03

|

-4.9%

|

-9.9%

|

5.0%

|

|

Bull

|

April '03

|

Sept. '07

|

14.7%

|

16.3%

|

-1.6%

|

|

Bear

|

Oct. '07

|

March '09

|

20.6%

|

13.7%

|

6.9%

|

|

Total

|

Sept. '99

|

March '09

|

9.0%

|

8.6%

|

0.4%

|

|

Bull

|

March '09

|

July '14

|

18.0%

|

20.1%

|

-2.1%

|

|

* All returns are on an annualized basis.

|

|||||

As you can see, holding shorts during bull markets "costs" us about two percentage points of annualized performance. But stocking up on shorts as the market peaks more than offsets these costs.

In the past two bear markets, having an active short portfolio – including shorts we began stockpiling before the market tanked – garnered an extra 5%-7% of annualized returns. Hopefully, you are beginning to see the recent performance of our short portfolio in a different light. Try to think of these picks not as individual bets... but as part of a broader strategy of protecting yourself in an uncertain market.

Many of our readers are nervous about shorting individual stocks. That's understandable. But shorting shares requires no additional effort. Your broker handles all the additional back-office intricacies. And whether you follow our advice or not, you should consider protecting yourself when market indicators begin warning about a top. The February 2007 issue of Stansberry's Investment Advisory describes one alternative to trying to handpick stocks to short...

|

Shorting a market index with a small portion of your portfolio offers another alternative for hedging your risk of a broad-market selloff. No matter how you do it, we advise readers to keep at least some short exposure at all times – especially as the market flashes warning signs.

One of the best-known short-sellers out there – Citron Research's Andrew Left – is presenting tomorrow at the S&A Conference Series event in Los Angeles.

He will share the names of two Internet darlings he thinks are poised to collapse. I can't share any more details... I don't want to ruin the surprise.

It's too late for you to join us in person... However, you can join us from the convenience of your own home... We're streaming the entire event live.

In addition to Left, you'll see presentations from Porter, Steve Sjuggerud, and famed satirist P.J. O'Rourke... Plus, you'll see Porter's on-stage debate with electric-car maker Tesla's cofounder J.B. Straubel.

If you sign up to watch our L.A. show, we'll also give you free online access to our last event of the year in Nashville – where you'll hear from former Congressman and presidential candidate Ron Paul and currency expert Jim Rickards. To learn more about the event – and make sure you don't miss out on all the action – click here.

New 52-week highs (as of 8/21/14): Apple (AAPL), Automatic Data Processing (ADP), Advent Claymore Convertible Securities and Income Fund (AVK), Brookfield Asset Management (BAM), Berkshire Hathaway (BRK), Dolby Laboratories (DLB), Integrated Device Technology (IDTI), Intel (INTC), KLA-Tencor (KLAC), PowerShares Achievers Fund (PKW), PowerShares QQQ Fund (QQQ), ProShares Ultra Technology Fund (ROM), RPM International (RPM), ProShares Ultra Health Care Fund (RXL), Sprott Resource Corp. (SCP.TO) ProShares Ultra S&P 500 Fund (SSO), Cambria Shareholder Yield Fund (SYLD), Union Pacific (UNP), and W.R. Berkley (WRB).

In today's mailbag, a subscriber offers his thoughts on hotly debated electric-car maker Tesla. Send your thoughts to feedback@stansberryresearch.com.

"Wow! For the first time since I became a subscriber (this year), Porter has his facts straight on Tesla. Although he sticks by his former theme, it has now become at least arguable. I still disagree with Porter's conclusions – but the disagreements are no longer on facts but on prospects. So, I like his analysis today a whale of a lot better than those he wrote weeks and months ago.

New 52-week highs (as of 8/21/14): Apple (AAPL), Automatic Data Processing (ADP), Advent Claymore Convertible Securities and Income Fund (AVK), Brookfield Asset Management (BAM), Berkshire Hathaway (BRK), Dolby Laboratories (DLB), Integrated Device Technology (IDTI), Intel (INTC), KLA-Tencor (KLAC), PowerShares Achievers Fund (PKW), PowerShares QQQ Fund (QQQ), ProShares Ultra Technology Fund (ROM), RPM International (RPM), ProShares Ultra Health Care Fund (RXL), Sprott Resource Corp. (SCP.TO) ProShares Ultra S&P 500 Fund (SSO), Cambria Shareholder Yield Fund (SYLD), Union Pacific (UNP), and W.R. Berkley (WRB).

In today's mailbag, a subscriber offers his thoughts on hotly debated electric-car maker Tesla. Send your thoughts to feedback@stansberryresearch.com.

"Wow! For the first time since I became a subscriber (this year), Porter has his facts straight on Tesla. Although he sticks by his former theme, it has now become at least arguable. I still disagree with Porter's conclusions – but the disagreements are no longer on facts but on prospects. So, I like his analysis today a whale of a lot better than those he wrote weeks and months ago.

"Related news: Mercedes is now preparing to offer a fully electric car of its own. It will have a smaller range – 250 km or 150 miles – than the Tesla Model S range of 200 to 250 miles. It will be a snazzy sports car with gullwing doors and all the trimmings. It has 4 electric motors, one at each wheel, so it is automatically an all-wheel drive car. Unlike any of the phony so-called hybrids, it has no combustion engine – it's pure bred, just like the Tesla model S. The MB is far more powerful even than the model S – some 580 hp if I remember the number correctly. The MB (AMG) will sell for abt. EUR 400,000 beginning next year. That's 1/2 million dollars. For that, one can buy a handful or more of Tesla model Ss. So, the Benz is an interesting alternative for those who want to best other electric cars – but its price makes it a super-expensive toy rather than a mode of transportation.

"Longer term, MB is rumored to plan selling a fully electric car with an auxiliary power plant for longer distance driving, based on advanced fuel cell technology. Again, no combustion engine, purely electric drive, with a fuel cell power plant for keeping the batteries charged on trips and for re-charging them while stationary. That is so much more sensible than the Rube-Goldberg-like hybrids – it will leave those in the dust. So, I look to be in a Tesla Model S next year – and in an electric MB with fuel cell auxiliary after that. If I live that long. Porter: have fun debating Tesla!" – Paid-up subscriber Goetz Oertel

"I must agree with reader Joe Severa. In the chaotic scenario many (of you) experts envision as possible transacting with high-value gold Eagles or Krugerrands is to paint a target on your family's back. I seem to remember Porter ridiculing such fears and recommending the internet. In normal times, sure. But for most of us when the culture is falling apart? I suggest pre-1965 dimes, quarters and half-dollars." – Paid-up subscriber Randall Ward

Regards,

Bryan Beach

August 22, 2014

Doug Casey: The biggest danger to your wealth...

When it comes to economics, social issues, and speculations, our friend Doug Casey, founder of Casey Research, is one of the best in the business.

In today's Digest Premium – excerpted from his latest book – Doug discusses the biggest danger to your wealth...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

Doug Casey: The biggest danger to your wealth...

Editor's note: When it comes to economics, social issues, and speculations, our friend Doug Casey, founder of Casey Research, is one of the best in the business. Earlier this year, Doug published a book titled Right on the Money in which he discusses economics, investing, and his perspectives on the world. In today's Digest Premium – excerpted from his book – Doug and Casey Research editor Louis James discuss the biggest danger to your wealth...

Louis James: Good morning, Doug. This week, I'd like to ask you about diversifying your assets outside of your home country. What is the danger for investors who keep all their assets at home, and what are the alternatives? It looks like there's a real risk of exchange controls blocking capital from leaving the U.S. The Obama tough talk on tax havens is one sign. What should people do, while there's still time, to avoid getting trapped?

Doug Casey: Well, investment risks are huge in today's world. But political risks are even greater, and most Americans are completely unprepared. The biggest danger to your wealth isn't the markets, as ugly as they are. The biggest risk today is your own government.

The only way you can protect yourself is by internationalizing your assets. So, while it is still possible – and I don't think it's going to be possible for very much longer – you should get as much money out of the U.S. as you can and put it into something that will be hard for them to force you to repatriate.

If you open a foreign bank account or brokerage account, that's a step in the right direction, and you may be grandfathered in somehow, but those things are liquid, so you could be forced to bring the assets back before you want to. I think the best thing that you can do is to either buy foreign real estate or to buy gold coins and put them in a foreign safe deposit box.

Louis: You mentioned something that Americans aren't familiar with – political risk. You've traveled and done business in a lot of countries. What kinds of negative policies are common in other parts of the world that you think are coming here?

Doug: Well, governments are capable of absolutely anything because they consider their citizens a national resource available for exploitation, almost like cattle. There are numerous things that the U.S. government might do, now that it has become so much like all the other governments.

They could put a tax on foreign investments, to discourage you from buying them. You'd still be able to send money out of the country, but you'd be charged an exit tax of 10% or 15%, or whatever the government wants. There might be a tax on foreign travel to cut down on Americans spending money abroad.

There might be a prohibition on opening up new bank or brokerage accounts outside the U.S. There are all kinds of possibilities. It would probably be politically popular; the average guy thinks that foreign investment is somehow unpatriotic, and foreign travel is frivolous, something for only "the wealthy."

Louis: If you have assets outside the United States but you're a U.S. citizen, aren't you at risk anyway?

Doug: Yes, you absolutely are. It's unfortunate that the tax laws have turned U.S. citizenship into an albatross. The United States is the only major country that demands taxes from citizens living outside the country. And even if you renounce your citizenship, they still want taxes from you.

First of all, they tax you at the time you expatriate, as though you had sold everything you own. Second, they still tax you on any income you earn in the U.S. for the next 10 years. And they levy a special tax on anyone in the U.S. who receives a gift or inheritance from you. So, over the years, America has become a roach motel for capital.

Louis: Planning can help, but it is getting more complex?

Doug: Yes. It is becoming very complex, and setting up a foreign company is subject to all kinds of reporting requirements. It's quite problematic. Really, the simplest and best way to gain some measure of political insulation is to buy gold and put it in a safe-deposit box and/or buy foreign real estate. Neither move triggers any special reporting requirements.

Louis: Let's talk about your first recommendation, buying gold and storing it abroad. How do I go about it?

Doug: We had an article recently in BIG GOLD, one of our letters that covers that question pretty thoroughly. In essence, you need a safe deposit box or a secure safe if you hold offshore property.

Louis: Over the years, you've bought real estate in many places – Spain, New Zealand, Canada, Hong Kong, Africa, South America, and elsewhere. I understand that you've recently invested in Argentina and Uruguay. Aren't you also at the mercy of the governments there?

Doug: The Argentine government has been amazingly stupid over the last 60 years, destroying the currency repeatedly, among other things. Now the U.S. government seems to be taking lessons from them. But on the plus side, the average Argentine has little love or respect for the government; most of them are transplanted Italians who seem to have a natural aversion to taxes.

It's demographically about the most European country in the world, has by far the largest community and tradition of classical liberalism in Latin America, and is socially very stable. It's quite different from places like El Salvador or Bolivia where there are masses of disenfranchised and landless peasants. Further, Argentines long ago learned how to deal with the nonsense the government specializes in; Americans have just enrolled for what's going to be an unpleasant learning experience.

One of many things I like about Argentina – and I've been to 175 countries and lived in 12 – is its extremely low cost of living, combined with a very high and sophisticated standard of living. That's why we chose Argentina to build what I intend to be the finest residential resort in the world.

Editor's note: Tomorrow, Doug will present live at our S&A Conference Series event in Los Angeles. Joining him are S&A editors Steve Sjuggerud, Frank Curzio, and Kim Iskyan... along with Tesla cofounder J.B. Straubel and 3D Robotics cofounder Chris Anderson, who Time magazine named one of the most influential people in the world. If you're interested in joining us for this event, it's not too late. You can view it live from the convenience of your own home. Click here to learn more.

Doug Casey: The biggest danger to your wealth...

When it comes to economics, social issues, and speculations, our friend Doug Casey, founder of Casey Research, is one of the best in the business.

In today's Digest Premium – excerpted from his latest book – Doug discusses the biggest danger to your wealth...

To continue reading, scroll down or click here.