My updated estimate of Berkshire Hathaway's intrinsic value; Sam Bankman-Fried Bows to Rescue From Binance's CZ as FTX Buckles; My dad is in the operating room

1) In yesterday's e-mail, I shared my friend and former partner Glenn Tongue's analysis of Berkshire Hathaway's (BRK-B) third-quarter earnings, which the company reported on Saturday.

Today, as I do every quarter, I'd like to update my estimate of the stock's intrinsic value. To do so, I apply a methodology I've used – and that I think CEO Warren Buffett himself uses – to value Berkshire for more than two decades.

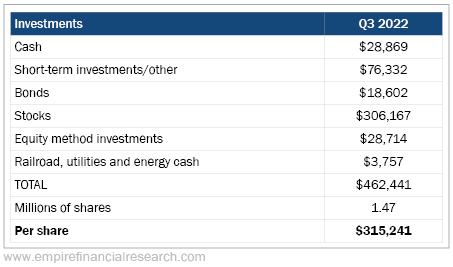

I start by taking cash and investments (valued at market), which were valued as follows as of the end of the third quarter:

I then adjust this to reflect the current value of the stock portfolio by using CNBC's Berkshire Hathaway Portfolio Tracker, which estimates that the company's stocks, as of yesterday's close, have risen in value to $332 billion. This $26 billion increase brings total cash and investments to $333,000 per A-share.

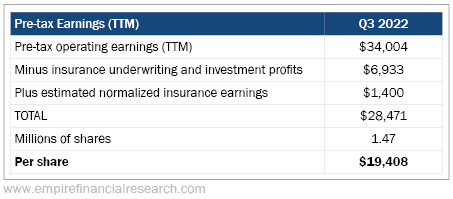

Then I value the wholly owned businesses, starting with their pre-tax earnings, which I calculate as follows:

Note that I subtract all of the underwriting and investment profits from Berkshire's massive insurance operations but add back a rough estimate of the average insurance underwriting profits over the past decade ($1.4 billion annually).

This results in $19,408 in adjusted pre-tax earnings per share over the past 12 months, to which I apply a multiple of 11 times to arrive at a value for the operating businesses of $213,000 per A-share.

Now add the $333,000 in cash and investments per share to arrive at a total intrinsic value of $546,000 per A-share (or $364 per B-share).

With the A-shares closing yesterday at $442,100, that means the stock is trading 19% below my estimate of its intrinsic value.

You can see why I call Berkshire "America's No. 1 Retirement Stock"...

Many companies have excellent growth prospects, a strong balance sheet (though none as strong as Berkshire's), and exceptional management (though, again, none as exceptional as Berkshire's, I'd argue), but I can't think of a single one that has these three traits and a stock that's significantly undervalued.

In my opinion, Berkshire should be the foundation of any conservative portfolio.

2) In my May 12 e-mail entitled "Sell your cryptos," I explained that I was "super bearish on the crypto sector" because "the odds of a very bad outcome have clearly risen quite a bit, so my Spidey sense is telling me that it's time to get out and wait for another time to rejoin the game."

At the time, the two leading cryptocurrencies, bitcoin (BTC) and ethereum (ETH), were trading at $29,048 and $1,962, respectively. Since then, as of earlier this morning, they're down 39% and 37%, respectively.

My view hasn't changed a bit, especially in light of the turmoil in the sector over the past week...

Two of the leading players who control the two largest crypto exchanges, Changpeng Zhao ("CZ"), the co-founder and CEO of Binance, and Sam Bankman-Fried ("SBF"), the founder and CEO of FTX, have engaged in an epic battle royale in recent months that came to a head recently when Zhao tweeted on Sunday that he was dumping Binance's holdings in FTX's cryptocurrency, FTT:

This triggered a run on the bank at FTX, which resulted in Binance agreeing to buy it (likely for little or no consideration). Here are four Bloomberg articles about the saga:

- Binance's CZ and FTX's Sam Bankman-Fried Trade Barbs Over Twitter

- Sam Bankman-Fried Bows to Rescue From Binance's CZ as FTX Buckles

- Crypto Prices Fall Most in Two Weeks Amid FTT and Macro Risks

- CZ SBF'ed SBF (Matt Levine's take)

Levine's missive concludes (correctly):

We talked about this situation yesterday, back when Bankman-Fried was tweeting "A competitor is trying to go after us with false rumors. FTX is fine. Assets are fine." I wrote:

If you are the CEO of a big crypto firm there are negative rumors about a big competitor, do you take to Twitter to say "we're not a scam like those guys"? One advantage of doing that is that you might win some business and harm a competitor; crypto is a smaller business than it was a year ago, so winning market share is very valuable. Another advantage is that you don't want people thinking that you're a scam; saying "we're not a scam like those guys" is one way to persuade people that you aren't.

The disadvantage is that it is probably in your long-term interest for people to be confident that none of the big crypto businesses are scams. "Crypto is full of scams and you can't trust even the biggest exchanges" is a bad message for a crypto exchange to send; adding "except us, you can trust us" does not help.

Well. Another advantage of doing it is that a day later you might be able to buy your valuable competitor for peanuts. One possible reading of this situation is that CZ did some tweets and got himself a $30 billion crypto exchange for pennies on the dollar. But it seems like a dangerous game to play. Bankman-Fried was rescuing crypto firms a few months ago; now he needs a rescue. What lessons should Zhao learn from that?

Not surprisingly, FTT has collapsed (and, I confidently predict, will soon be at zero): FTX Token Falls 80% Despite Binance Bailout as Alameda Contagion Spreads to Bitcoin. Here's FTT's stock chart over the past week:

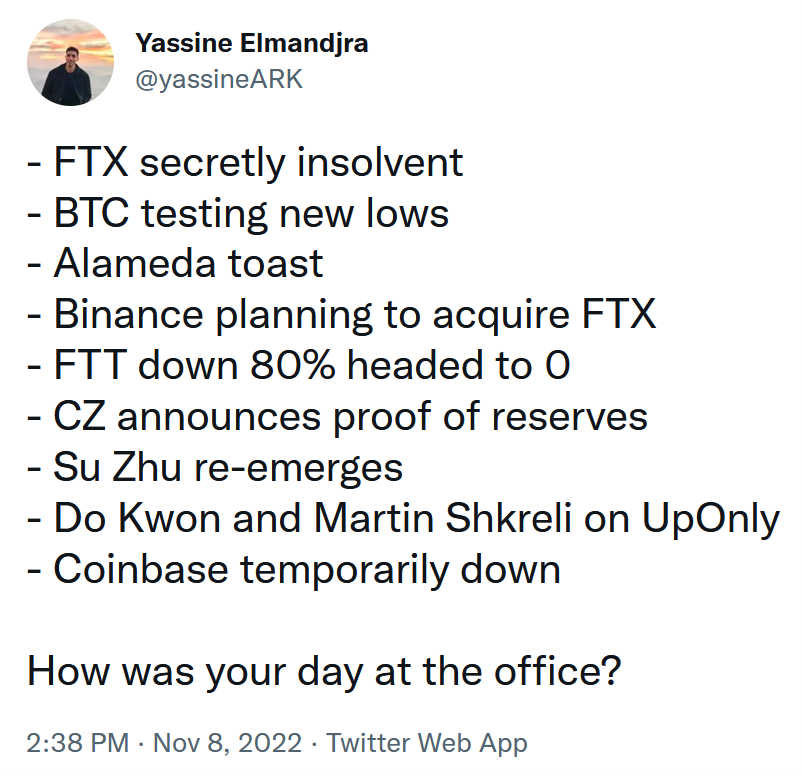

Not surprisingly, commentators are having a field day with this. Here's one tweet:

And another:

And lastly, here's a hilarious video clip referencing the schadenfreude Charlie Munger must be feeling after his many warnings about the crypto sector:

3) Thank you for the many kind wishes for my dad.

I drove five hours last night from New York City to New Hampshire, slept from 1 a.m. to 5 a.m., and then drove my parents to the Dartmouth Hitchcock Medical Center, where my dad is having a second catheter/cardiac ablation right now to address his atrial fibrillation (A-fib).

Here's a picture of us just before they took him into the operating room:

I'll let you know tomorrow how it goes...

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.