A major bank's ludicrous advice... Leveraging into a crashing high-yield market... Why lower oil means lower junk bonds... We're seeing the 'melt-up'... Munis are still outperforming... Momentum stocks come back down...

Do you remember back in September when financial-services giant Citigroup advised its clients to lever up and buy high-yield debt?

Do you remember back in September when financial-services giant Citigroup advised its clients to lever up and buy high-yield debt?

At the time, high-yield (aka "junk") bonds were trading at all-time highs. But Citi said investors should borrow money and buy junk bonds to achieve their desired annual returns. Bloomberg reported on the call...

|

Keep that final quote – about high-yield bonds being less risky than Treasury securities – in mind throughout today's Digest.

Of course, we don't have a $161 billion market cap like Citi... Nor do we have nearly 250,000 employees around the globe to produce our research. But we do have some common sense. And we know that buying the riskiest corporate debt at record-high prices (and therefore record-low yields) on margin wasn't a safe strategy. We called it "return-free risk."

Porter shared his views on high yield in the June 18 Digest...

|

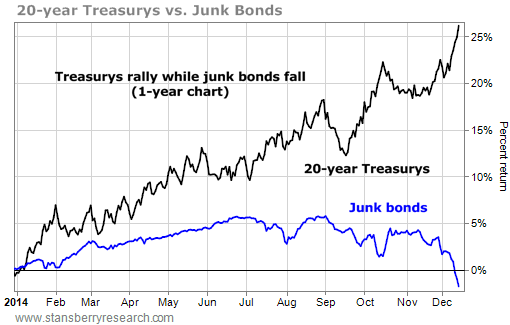

During the market's lows in the financial crisis in 2009, junk bonds were yielding about 22% more than Treasurys with similar durations – the so-called "risk spread." Earlier this year, that spread was at its lowest level in history. We shifted from extreme fear to extreme greed. You've probably heard the old Warren Buffett saying about fear and greed...

No, Citi may not have seen the selloff in oil coming... But it should have at least been aware of the effect it could have on its beloved junk bonds.

Today, oil fell straight through the $60-per-barrel level...

On fear of slowing demand, the International Energy Agency (IEA) lowered its global demand forecast for the fourth time in five months, helping oil prices fall 3% today.

Energy producers increasingly relied on the high-yield debt markets for financing...

According to investment bank Barclays, energy companies' share of the high-yield bond market have increased from 4.3% in 2004 to 15.2% this year.

In other words, in addition to the many other factors that could pop the high-yield bubble... falling energy prices was another major concern.

And we're seeing the selloff in oil spook high-yield investors...

In the past week, investors pulled $1.9 billion from high-yield bonds – the largest single-week outflow since the $2.3 billion outflow the week ended October 1 (which followed an $859 million outflow the week before that), according to fund tracker Lipper.

The money fleeing from high yield is going into safety assets – namely U.S. Treasurys.

In April, Martin Fridson – nicknamed the "Dean of High Yield" – warned attendees at the Grant's Interest Rate Observer conference that this scenario could happen. DailyWealth Trader editor Amber Lee Mason discussed it...

|

Here's what that melt-up has looked like over the last year...

As you can see in the list of today's 52-week highs (below), the ProShares Ultra 20+ Year Treasury Fund – which Amber recommended in DailyWealth Trader – just hit a new high.

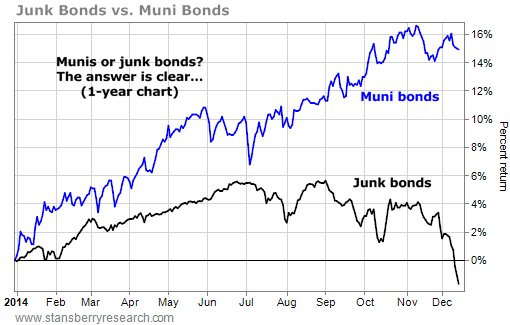

Our favorite bond sector – municipal bonds – is also outperforming the market...

Muni bonds are debt issued by state and local governments. This is one of the safest areas of the bond market. Munis have a minuscule default rate... and pay a tax-free yield.

Retirement Millionaire subscribers are up nearly 100% on municipal bonds since 2008. And they're still collecting double-digit (tax-equivalent) yields on their invested capital.

Given the fear and uncertainty in the world today, we doubt yields are heading higher any time soon. And municipal-bond funds are still a great place for capital. You can still buy certain funds for double-digit discounts to their net asset value that pay close to double-digit yields on a tax-equivalent basis.

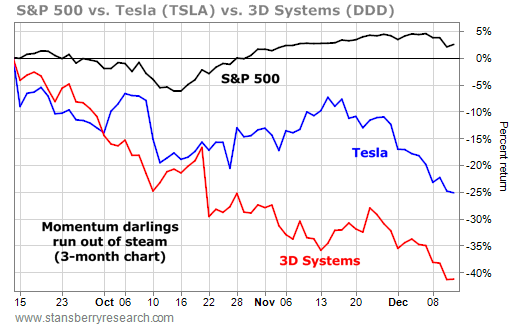

Investors today are dumping risk across the board. And that includes shares of some of the market's momentum darlings – like 3D Systems and Tesla Motors... Stocks we've warned against given their absurd valuations. When stocks are priced for perfection – a state we rarely see in the world – bad outcomes usually follow...

We told you about 3D Systems' absurd valuation in the January 13 Digest...

|

This year turned out to be a year of production delays and missed expectations. 3D Systems shares are down nearly 70% since the start of 2014.

And of course, there's one of our favorite whipping boys, electric-car maker Tesla...

Tesla makes about 35,000 cars a year and produces $2 billion in revenue. But it's valued at half the price of BMW – one of the world's premier auto manufacturers, which makes around 2 million cars a year and produces $100 billion in annual revenue.

The list of Tesla's issues continues to grow... It trades at an outrageous valuation, it loses money every quarter, its cars catch on fire, and it's building a $5 billion "gigafactory."

Plus, as Porter explained in the July 9 Digest Premium, he questions the validity of its accounting...

|

Of course, we've recently had success with one of Stansberry Venture editor Dave Lashmet's biotech recommendations...

As we wrote in Monday's Digest, pharmaceutical giant Merck purchased biotech company Cubist for $9.5 billion... Readers are up more than 40% since September.

That's the beauty of investing in medical companies that work to produce the next wonder drug or technology. It doesn't matter what's happening with the price of oil... or which country is in the middle of riots...

If a company discovers the cure for cancer, its share price will soar.

On the topic, Retirement Millionaire editor Dr. David "Doc" Eifrig just left San Francisco, where the annual American Society of Hematology meeting is in full swing. While there, he dined with one of the world's leading researchers in blood disorders... and just as he predicted months ago, the latest data from the search to cure cancer is spectacular.

Even the Wall Street Journal and USA Today have published stories on the miracle cures that are coming out of the research being presented for the first time to the world. The big news is the powerful paradigm shift using a cancer treatment called "immunotherapy."

As Doc told us, researchers presented on a breakthrough using immunotherapy to treat Hodgkin's lymphoma and even acute myeloid leukemia (AML), which is normally deadly, with the standard treatments almost as bad.

Doc's subscribers are already familiar with immunotherapy. In his latest report, titled "The Living Cure," he discussed why immunotherapy is revolutionizing how doctors treat cancer patients, how to get access to this treatment, and the questions you absolutely must ask your doctor if you discover that you or a loved one has cancer.

Doc even shared the name of a company that's going all-in on this kind of new cancer treatment (and, in many cases, potential cures). You can access Doc's special report with a four-month, risk-free trial subscription to Retirement Millionaire for 60% off the retail price. You can learn more here.

New 52-week highs (as of 12/11/14): Cempra (CEMP), ProShares Ultra 20+ Year Treasury Fund (UBT), and UIL Holdings (UIL).

Nothing going on in the mailbag... Have we done anything to anger you lately? Let us know at feedback@stansberryresearch.com.

Regards,

Sean Goldsmith

Baltimore, Maryland

December 12, 2014