Help prevent wrinkles by eating McDonald's... What happens if we have a crisis?... Yellen's warning: time to panic?... The classic investor's dilemma: bonds or stocks...

Editor's note: The Stansberry Digest editors are in Sea Island, Georgia this week for our annual Spring Editors Conference. So we're doing something a little different for today's Digest. We're featuring some bonus commentary from Dr. David "Doc" Eifrig's Retirement Millionaire research team. We hope you enjoy. We'll return to our normal fare later this week...

We wrote it, did you buy it?

Doc Eifrig recommended shares of McDonald's (MCD) to his Retirement Millionaire subscribers back in August 2010. And in the March issue, he predicted that we'd see the fast-food giant rolling out fresh, healthy ingredients in a few years...

|

McDonald's needs to adapt and figure out how to appeal to new consumer tastes. Once it does, it can push that newfound success out to 36,000 restaurants. In the meantime, it still earns $4.2 billion in free cash flow every year. That's enough to keep the dividend and share buybacks growing.

Plenty of writers and fortune-tellers have declared McDonald's a dying giant... Their gleeful predictions have made the stock cheaper and more attractive. Just watch... "Mickie D's" will soon announce it's getting rid of preservatives and high sodium levels. Its ads will feature fresh-looking vegetables. I bet I'll be able to buy an arugula salad at the drive-through in a few years.

|

|

Sure enough, McDonald's announced last Thursday that it was adding kale to its menus. From the

Associated Press...

|

Kale is included in a turkey sausage and egg white bowl, which also has spinach and bruschetta. The other option is a chorizo and egg bowl, which includes a hash brown, cheddar jack cheese, and pico de gallo.

On Wednesday, Janney analyst Mark Kalinowski had also noted on that McDonald's was introducing three salads in Canada that have kale as an ingredient.

|

|

Doc's longtime readers know that kale is one of his favorite "superfoods." Back in 2011, he told his Retirement Millionaire subscribers about its benefits...

|

Kale is packed with vitamins A and K. Vitamin A is essential for your skin tissue to repair itself. Studies show vitamin A controls acne, reduces wrinkles, and corrects flaky skin. Vitamin K helps maintain skin's elasticity, which keeps your skin from sagging and developing wrinkles.

Kale is an easy food to add to your diet. This dark green, leafy vegetable looks similar to lettuce, but the taste is slightly bitter. Do what I do and add a little bit to your salad to get the amazing skin benefits.

|

|

If you don't already own shares of McDonald's, it's one of the stocks that Doc and Porter agree on. Porter went so far as to call it the one stock

everyone should own. From the

April 10 Digest...

|

My prediction is that over the next decade, McDonald's shareholders will receive returns of capital worth at least $100 billion – more than the entire business is worth today. If you're a shareholder, do you have to worry about what the stock price will do tomorrow or next week? Nope. You're going to get paid no matter what happens. And even after you've been paid back more than 100% of what you put up to buy the business, you'll still own a piece of the company, which by then will surely be worth a lot more.

|

|

Porter went on to note that investors who bought McDonald's shares back in 2006 – which meant they held through the worst financial collapse in decades – have already made around 200% on their money...

|

I'm confident that based on McDonald's current share price, similar (or even superior) returns are currently available to any investor wise enough and patient enough to buy McDonald's stock today.

There's essentially no risk to this investment at this price given McDonald's brand, locations, price point, margins, and capital efficiency. So... if you're looking to protect your wealth during a financial crisis (you should be), look no further than the oldest recommendations still sitting in our Top 10 list. These types of companies are a great way to get rich, no matter what happens to the economy or to the stock market.

|

|

Doc's subscribers are up nearly 55% as of yesterday's close.

Earlier this year, a subscriber to Doc's options service

Retirement Trader wrote in asking what would happen to Doc's recommended trades if we head into another financial crisis. As Doc explained...

|

I come at investing, finance, and life from a conservative and pragmatic point of view. When I hear predictions about our economic future – good and bad – I look for opportunities... ways to trade, hedge, and make money. If times do turn crazy, we'll be investing in the craziness and be protected along the way.

I'm well aware of the risks of bubbles and a possible meltdown again. But for now, the U.S. dollar remains the world's reserve currency. In many places, it's the preferred payment for commerce – even in countries like Turkey, where you'd think the euro would be the heavy favorite.

And if there is another meltdown, we'll be ready like the anaconda to pounce on the opportunities.

|

|

We realize that closely following interest rates can be like watching paint dry. But they're an important factor in deciding what to invest in (like certificates of deposit, a savings account, stocks, bonds, or real estate, for example).

As Doc recently explained in the April edition of his subscriber-only podcast, Uncut...

|

We're at a place where interest rates are really low and there are risks of them starting to rise. But the question is, what would make them rise?

And I think the answer for us, at least, is that rates are eventually going to rise, from both the Federal Reserve raising short-term rates and from the economy starting to pick up and there being more and more of a demand for money. That would raise the price of interest rates.

|

|

Regular

Digest readers know that the Federal Reserve raising rates is getting more attention in the mainstream headlines. That's mostly because of Fed Chair Janet Yellen's latest comments. As she explained last week...

|

I would highlight that equity valuations at this point generally are quite high. They're not so high when you compare the returns on equities to the returns on safe assets like bonds, which are also very low, but there are potential dangers there.

When the Fed decides it's time to begin raising rates, these term premiums could move up and we could see a sharp jump in long-term rates. So we're trying to... communicate as clearly about our monetary policy so we don't take markets by surprise.

|

|

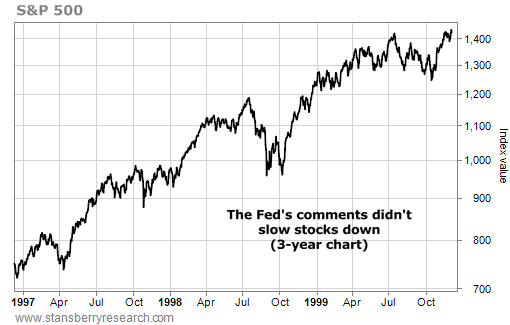

This is worth keeping an eye on... but it's not worth panicking. After all, back in 1996, former Fed Chairman Alan Greenspan used the phrase "irrational exuberance" to describe the stock market. The benchmark S&P 500 index rose more than 90% over the next three years...

Interest rates also serve another important purpose of helping income-focused investors decide between buying stocks or bonds. As Doc told

Retirement Trader subscribers last month...

|

One classic way to determine if stocks or bonds are the better investment at any one time is to look at the spread between the interest paid on the 10-year U.S. Treasury and dividend yield of the Standard & Poor's 500 Stock Index. When the spread is wide, you want to buy bonds because they yield much more than what you'd expect to get from stocks. But as you can see... today, the relationship is as tight as I can imagine.

That means bond prices have gone too far up or stock prices are too low (or some combination of the two). Today, we can buy blue-chip companies with dividends greater than the 10-year U.S. Treasury notes. Why own bonds if you can own dividend-paying stocks?

|

|

It's clear that stocks – especially ones that produce income – are the better value today. And in the April issue of

Income Intelligence, Doc recommended a stock yielding a safe 4%-plus.

This investment is in the health care industry. And as longtime Stansberry Research subscribers know, Doc believes health care will continue to boom for years to come. As he wrote in that issue...

|

One trend will march forward into the next decade without slowing, regardless of what the economy does... Americans are getting older.

Right now, nearly 45 million Americans are older than 65. By 2020, that number will grow to 53 million. By 2040, 77 million Americans will be older than 65. And the proportion of those older than 85 years of age will quadruple as the Baby Boom generation grows older and life spans increase. With age comes big health care bills. The average American racks up $300,000 in medical bills in a lifetime, and $188,658 of that comes after age 65.

And I haven't even mentioned the 16.4 million people added to insurance rolls under Obamacare. Now, nearly 90% of Americans have health insurance. And they are going to use it. Simply put, this health care boom represents the key trend for our generation of investors.

|

|

Out of respect to Doc's

Income Intelligence subscribers, we can't give you the name of this company. But right now, you can get a full year of

Income Intelligence for just $49. We believe it's one of the world's best values. For more details on how to sign up,

click here. (You won't have to sit through a long video presentation.)

New 52-week highs (as of 5/11/15): AXIS Capital (AXS), Blackstone Group (BX), CDK Global (CDK), and Energy Transfer Equity (ETE).

Have you profited from Doc's research? The subscriber in today's mailbag has. Send us your experience with Doc's advisories to

feedback@stansberryresearch.com.

"I am a subscriber to

Retirement Millionaire and I must say it is the best financial newsletter I have ever had the pleasure of reading. Now I can make that claim because I have been reading various finance newsletters for the past 35 years. I must tell you that your observations about the financial world and social commentary are spot on, and I value and look forward to every issue and commentary by Porter. Keep up the good work. I have learned so much form your insights and knowledge and I am most grateful. Many thanks." – Paid-up subscriber Brian Tennyson

Stansberry Research comment: Thanks for the kind words, Brian. We think

Retirement Millionaire is one of the greatest bargains in our industry. And we'd urge any Stansberry Research readers who are on the fence to give Doc a try. You can get a full year of

Retirement Millionaire for just $49 a year. And you can even take four full months to decide if it's right for you.

Click here to get started.

Regards,

Stansberry Research

Baltimore, Maryland

May 12, 2015