Editor's note: Over the past few years, True Wealth editor Steve Sjuggerud has made some amazing calls... and his readers have made a ton of money.

This weekend, we're running two of Steve's classic issues that walk you through his thinking.

The companies discussed in this research might not be "buys" when you read this... and the specific advice these essays contain is dated... But there is great value in studying the unconventional thinking behind these successful ideas.

In today's edition of our weekend Masters Series – originally published in the August 2009 issue of True Wealth – Steve makes two incredible calls... buying real estate and buying Warren Buffett. Both have turned out to be huge winners.

The specific numbers Steve discusses below are from 2009... when stock and real estate investors were incredibly pessimistic.

It's Finally Time in Real Estate

By Steve Sjuggerud, editor, True Wealth

"I'm scared," a retired bank CEO told me last night.

I've never seen him scared before. With a half-century's experience in the financial markets, and having been the CEO of a few banks, he's hard to scare.

I see him a few times a year. And I love to hear what he's thinking. For example, early last year, as the banking crisis was getting going, his words were perfect...

|

If you swing easy, you can hit the ball well. Swing too hard, you can get into trouble. This retired banker was successful because he simply had the humility to swing easy in his career. But right now, things are different...

"Steve, right now, I feel like a turtle in his shell. But I don't know when to come out," he told me last night. After he retired from banking, he got into real estate development. Today, there are no buyers...

|

Now, he's scared. "I'm stuck in my shell," he says. "I don't want to sell. But I don't want to keep paying property taxes and mortgage interest indefinitely... I don't know how long I want to take this."

When even the "smart money," like this retired banker I respect, is getting scared... This is a sign we're near the bottom in real estate.

It's finally time in residential real estate... From charging the government 18% interest to buying distressed properties for huge discounts, opportunities are everywhere.

It'll take equal parts guts, patience, and money. But as I'll explain, Obama won't let you fail. And the payoff could be extraordinary – triple-digit profits are definitely possible within two years. And you could even make a once-in-a-lifetime, $500,000 TAX-FREE capital gain in two years. Let me explain...

The Hardest Thing in Investing:

Recognizing a Bottom and Acting on It

You and I would like to buy investments "at the bottom."

Rationally, we think we can. But it's much more difficult than anyone realizes... When you're in the moment, it's very hard to do.

Things feel so terrible at the bottom that you're afraid to pull the trigger and buy. At that moment, every fiber of your body says, "You're being ridiculous." For me, the nastier it feels at the starting point, the bigger the gains I end up pocketing. The key for me is separating my emotions from what's rationally going on... separating my heart from my head.

On the flip side, at the top of the real estate market in 2006, things were so good, Donald Trump was getting $1.5 million per speech to talk about getting rich in real estate. It felt like nothing could go wrong in real estate.

In San Francisco alone, 75,000 people showed up to hear Trump's "secrets." Now, just think about that for a moment... When 75,000 people in one town are competing for the same few properties, what do you think the result will be? They're doomed to lose money in the long run. And they did...

That summer of 2006 was the top. Since then, home prices in San Francisco have fallen nearly 50%. The cheapest third of the homes – the ones Trump's fans might have been able to afford – have fallen 61%.

Look... the biggest "secret" to making huge profits is buying something of value when nobody else wants it – buying it when it's "hated." To complete the deal, you must sell it when it's loved. A great sign an asset is loved is when Donald Trump is speaking in San Francisco to 75,000 people about it.

Right now, real estate is a hot potato... Nobody wants it. Everyone wants it off their hands. It's hated. That's great... That means we're nearing the bottom. What we need to do is figure out how to take advantage of it. In short, if you can buy "beachfront" property – basically prime property that can always be resold – at a few cents on the dollar today, you can hardly go wrong...

Particularly when there's a 100% chance the government will make sure home prices stop falling... and the potential is there for hundreds of thousands in tax-free capital gains...

Why Residential Real Estate Won't Crash from Here

I don't know about you, but I really don't like lighting my barbeque grill...

I feel like my life is on the line. I turn the gas on, and I start punching the button. I keep punching... but it doesn't light. I know the big WOOSH is coming, and this time it might finally burn my eyebrows off.

Our government is trying to light up our economy the same way... President Obama and Fed Chairman Ben Bernanke have the gas on, and they keep punching the button. But nothing's happening – yet.

The thing is, Ben Bernanke is willing to sacrifice our eyebrows. The big WOOSH will undoubtedly come... Our government has a variety of powers (including the printing press) to make it happen.

Once the economy lights up, instead of hurrying to turn down the gas, Bernanke will keep the gas on high for a while, just to make sure it stays lit.

He'll even add some lighter fluid. (You can't be too sure!) He'll risk dramatic overheating. To the government, it's better than the alternative, which is just too gruesome for Obama and Bernanke to consider.

This is where we are today.

I'm absolutely certain President Obama and Ben Bernanke will do everything they can to prop up the U.S. housing market. You see, if housing prices keep falling, the U.S. economy will enter a death spiral...

Housing is the main source of collateral for just about everyone in America. It is the root of credit. When the value of the collateral goes down, people stop buying stuff. If the value of the collateral goes down far enough, people start going bust. The wheels of commerce stop. That is starting to happen.

Obama and Bernanke must stop this vicious cycle.

They're trying. The finger is on that button. They're printing money, propping up banks, giving all kinds of credits to home buyers, buying mortgages from banks to keep mortgage rates low... the list goes on.

Eventually, the button-pushing will work. They'll succeed. And they will overshoot... They will let things overheat just to be certain they accomplished their goals.

They want to ignite the housing market now. They'll figure out what to do with it once it's lit later.

This is what the government is giving us now.

In the last few months, our best investment ideas have come from taking what the government is giving us. We're up 53% on Hatteras (NYSE: HTS)... which is a boring business that happens to take advantage of the government right now. It simply borrows money at 2% and invests it with no credit risk at 5% in government-guaranteed mortgages. It wins on both sides of the trade... The Fed has cut rates low, so Hatteras can borrow cheaply. And the government guarantees the mortgages it buys. I love it.

We're up 12% in our first month on Washington REIT (NYSE: WRE). This is the company I called "Obama's Landlord." We bought this on the idea that one thing we can be certain of in a world of uncertainty is growth in Washington D.C.

And now, the government is giving us an opportunity in residential housing.

$500,000 Gains, Tax-Free, If You're Willing to Do This

Housing will recover. The government will prop it up, creating a floor for prices.

But to take advantage of this opportunity, we don't need housing to soar. We just need it to stop falling. Then, you have the potential for huge capital gains – tax-free. Here's the story...

More distressed selling is going on now in real estate than I've ever seen in my career – in any asset. Because of this, you can get once-in-a-lifetime bargains.

Banks are dumping real estate. For example, SunTrust Bank has pages and pages of bank-owned properties for sale. (It's "hiding" them online here.) A bank is not in the business of owning property... and it doesn't want to be. It wants to get rid of these properties. Another banker friend of mine told me SunTrust and banks like it will "accept just about anything."

So the basic trade we're making is this: Banks and other desperate sellers currently value cash in hand way more than the property. Whatever the story – whether the seller needs the money, or is fed up with taxes and mortgage interest, or is a bank that simply wants to get the property off its books – he isn't willing to sit on it any more.

But he has a problem. Like my retired banker friend said, there are no offers out there. This is the one time you have an advantage over big investors... Real estate is local. Big investors likely won't know about local deals near you.

Here's what I'm going to do... I'm going to find a home near me that was priced at $2 million two years ago that's on the market for $1 million today. Then I'm going to make a low offer: $500,000. If the seller bites, we'll move in and make it our primary residence for two years.

My wife has veto power, of course. But she's up for it. She sees the potential benefit: $500,000 tax-free. Here's how...

The best tax break in America is on your primary residence. For a married couple, if you own a home for two years and sell it, the first $500,000 of your capital gains is tax-free. So if the market is flat for two years, then we could sell it for $1 million. We'd have a $500,000 tax-free capital gain.

Considering tax rates are going up, in two years, you might have to make $1 million or more in taxable income to equal $500,000 tax-free in your pocket today.

Heck, you could buy a place like this close to your current house and keep your existing house if you can swing it. Maybe you could rent out your old home for two years. Just plan on leaving your old home for two years to live in the new place, then sell it, take the gain, and go back "home."

My hypothetical numbers here are simplified, of course. And I know this isn't going to fall in my lap. I have to work for it. I also can't be in a hurry to make this happen. There's a bit more pain before the bottom.

If you want to try a deal like this, remember: You can't know when the "yes" will come. But you have to make offers. And we are in a bit of uncharted territory economically, so you need to keep more of a reserve than you think you might need. That way, you can hang on to your fire-sale purchases through more pain, if it comes.

Borrowing money is difficult right now. This is one of those times where someone else may recognize an incredible deal but might not have access to the money to make it happen or they're too scared to pull the trigger. If you have access to money and you are bold enough to put it to use, you are ahead of 99.9% of the population.

For me, one issue is timing... One of my problems in investing is being a bit too early. I recognize an opportunity is great early on, and I can't resist. But you need others to recognize it too and capitalize on it for the price to rise.

I'm personally wrestling with "too early" versus "25 cents on the dollar." There's a potential tax-free 100% gain hiding there just for taking property off the bank's hands and being willing to live in it for two years.

What I'm Doing with My Own Money Right This Minute

The retired banker asked me last night what I've been buying lately. I told him I've been buying Florida tax-lien certificates, which basically pay 18% interest. He said, "Oh yeah, I forgot about those things. They're a great deal."

Here's the basic idea: Someone hasn't paid his taxes. The county is desperate for tax revenues. So you pay that guy's taxes for him and the county gives you a tax-lien certificate.

The county chases down that delinquent payer AND rewards you handsomely for paying the taxes on his behalf. Once the person pays the taxes or is foreclosed on, you get your money with 18% interest (that's the deal in Florida, anyway).

The investment is incredibly secure, particularly for the 18% reward. Your tax-lien certificate is a first-in-line secured lien on a property. In other words, you get paid even before the bank that holds the mortgage. So you have, say, $100,000 in security (the property) on a $2,000 lien, just to make up an example.

I've bought tax-lien certificates in the last few weeks. But I haven't bought any fire-sale real estate yet. I am looking... bank sales, auctions, foreclosures, you name it.

Look, here's the moment you're trying to get to: At the very bottom – at the absolute worst moment – some distressed sellers will accept those 25-cents-on-the-dollar offers. The bank will be desperate to dump. And your offer will be the only one on the table. (You don't know when that day is exactly, so you have to be making the offers and hold your price.)

Meanwhile, Obama and Bernanke are busy pushing the "ignite" button. They're pushing, pushing, pushing. It will light. It may end up creating a massive WOOSH of inflation down the road... which would only push the value of your new property up. But again, we don't need real estate to soar. If you can buy at 25 cents on the dollar and sell at 50, that's still a fantastic, 100% return.

If you're able to get the family on board for two years of sleeping in another house, you could pick up a few hundred thousand dollars in profit, tax-free.

I can't pick a stock for you this month to do this deal. The deal is yours to find. But a few hundred thousand dollars tax-free is worth trying to figure out.

Get your act together. Put some financing together if you can and start making some low offers. Don't worry if none are accepted. You don't need a hundred yeses – you just need one. And you're not in a hurry.

In the next 12 months, I guarantee that's what I'll be doing...

We've got to take what the government is giving us. It's giving us tax-lien certificates at 18% (here in Florida). It's giving us Hatteras and Washington REIT. And it's working hard to create a floor in housing prices. It's limiting our downside risk in housing.

Meanwhile, nobody has any money. And those who do are too scared to put it to use in real estate now. Be the only offer on the table. And once it finally comes through, heck, put a sign in the yard asking 100% more than you paid for it.

In a couple years, the biggest gains in residential real estate – the gains from when things go from bad to less bad – will be behind us. It'll be time to move on... time to put that money to work in place with more upside potential.

For now, though, the government is limiting your downside. If you buy right – if you buy a quality property at a great price – your upside is unlimited.

This is a moment – an opportunity – you may never see again in your lifetime. Get started now and take advantage of it within the next 12 to 18 months.

Sell Trump, Buy Buffett

Donald Trump is the poster boy for the excesses of three years ago. Meanwhile, Warren Buffett, the world's second-richest man, still lives in the house in Omaha he bought more than 40 years ago and drives a pickup truck.

Americans are in the midst of a change in how they live... Conspicuous consumption is out. Thrift is in. Trump's out, Buffett's in. And it may take a while for conspicuous consumption to return.

Trump and Buffett have handled the crisis as you might expect. Trump is getting swallowed by the crisis because of debt. And Buffett is reveling in it.

For example, Donald Trump won't pay a $40 million personal guarantee he owes on a Chicago condo project that isn't selling. His excuse? The financial crisis was an "Act of God." I'm not kidding.

And just this week, his lawsuit against a writer was dismissed... Trump sued the author of the 2005 book Trump Nation, who said Trump was worth more like $200 million back then, not the billions Trump claimed. Who actually sues someone for that?

Around the same time, Trump was avoiding his personal guarantee, Buffett did exactly what a great investor does... He had cash when nobody else did and he put it to work. (That's what we want to do with real estate in the next 18 months.)

At the height of the crisis last year, Buffett spent billions propping up Goldman Sachs, and he got an absolutely ridiculous deal. (Part of the deal was stock warrants giving him the ability to buy $5 billion worth of Goldman stock at $115 a share. Today's price is $157 a share... That gives Buffett – or more correctly, his investment vehicle, Berkshire Hathaway – a paper profit of more than $1.7 billion.)

I don't want to waste your time singing Buffett's praises. You already know he may be the greatest investor who ever lived. He has made a career of making distressed loans to big businesses for a high interest rate, plus an arm and a leg.

You know the basic story. I simply suggest buying shares of his company today...

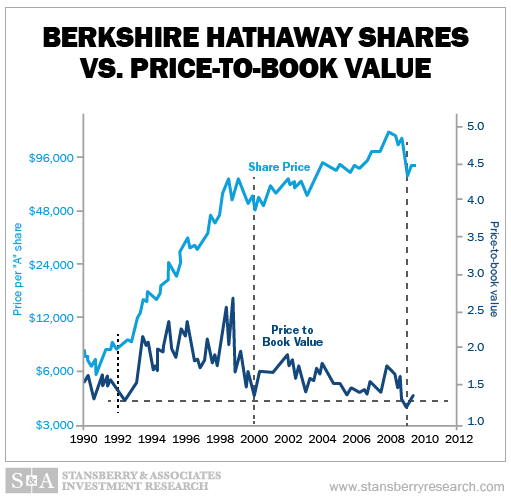

I have just one "exhibit" for you that should explain why now is a great time to buy: the price-to-book ratio of shares of his company.

"Book value" is a very rough measure of the liquidation value of a company. Whenever the shares of the greatest money manager in the world trade near the liquidation value of his company, they're a buy.

They traded nearly this low in 1992, and it was good for a near-100% gain in just a year. It happened in 2000 and was good for a 50% gain in just a year.

We're here again... and the shares are even cheaper this time around. Buy shares of Berkshire Hathaway (NYSE: BRK-A or BRK-B) today. Use a 25% trailing stop. Otherwise, plan on holding forever.

Editor's note: Steve says you can still make a lot of money in real estate. But he has discovered one investment that's even safer in the long run: The secret behind several of the world's richest families. It has nothing to do with stocks, mutual funds, or options. But he says it could make you 500% gains… with little risk. Steve believes this could be one of the best investments in the world in terms of risk, safety, and potential reward. Learn more about this opportunity here.