New highs for one of Porter's top recommendations...

New highs for one of Porter's top recommendations... CVS purchases Omnicare... Doc's prediction is coming true... Another big win for True Wealth subscribers... Steve's No. 1 recommendation today...

![]() One of the top recommendations in the Stansberry Investment Advisory portfolio just hit yet another new high...

One of the top recommendations in the Stansberry Investment Advisory portfolio just hit yet another new high...

Pharmaceutical giant Bristol-Myers Squibb (BMY) hit a new 14-year high yesterday.

As we mentioned in the March 10 Digest, shares spiked higher after the company's revolutionary cancer drug, Opdivo, received new U.S. Food and Drug Administration (FDA) approval to treat lung cancer. Dave Lashmet, the analyst who led the research on Bristol-Myers, explained why this was so important...

Opdivo adds about 50% to the survival time of smokers with lung cancer... and it does so with limited side effects. It's such a profound survival advantage that the trial stopped early because it wasn't fair to the people on traditional chemotherapy. This trial covers about 25% of all lung-cancer patients. Another trial, including most other smokers, will finish later this year.

Lung cancer is the single-largest killer among cancer patients... so this is a big market. It's about 10 times larger than the advanced skin-cancer market, where Opdivo was first FDA-approved. The market was pleased, but we still think there are more approvals like this to come.

Because Opdivo treats your immune system – waking it up to a cancer that's hiding inside of you – it should work on any cancer with minimal side effects. Porter and I searched 16 years to find safe and effective cancer drugs like this as investments. In Bristol-Myers' Opdivo and Yervoy [the company's first blockbuster cancer drug], we found them.

Today, we checked in with Dave to get his latest thoughts on the company. Here's what he told us in a private e-mail this afternoon...

Next week is the American Society of Clinical Oncology (ASCO) Annual Meeting. It's the big conference for cancer doctors – 28,000 doctors will be there. For investors, this is the best time to see the data that drive cancer drug sales. Cancer drugs were a $100 billion market in 2014 and could be a $150 billion market by 2018. So over the next four years, Big Pharma could earn an additional $100 billion.

In the last quarter of 2014, Bristol sold $6 million of Opdivo. But by the first quarter of this year, Opdivo sales had already surpassed $140 million. We think this is just getting started.

Opdivo is already mentioned in an astounding 664 abstracts and speeches at ASCO. And the clinical results have been incredible. For example, in end-stage kidney cancer, Opdivo (combined with Yervoy) had a 40% response rate in 94 patients. Over a year into the trial, there's no median survival data... because fewer than 50% of the patients on these drugs have died. Folks aren't becoming "statistics."

Meanwhile, Dave notes, the historic five-year survival rate for end-stage kidney cancer is just 8%, according to the American Cancer Society. And that number can be inflated...

Kidney cancer patients tend to be older than other cancer patients. If they die of anything else – like a heart attack or stroke – then it wasn't cancer that killed them. So the true expected survival is worse than 8%.

You can do the math... Bristol-Myers' Opdivo isn't yet approved to treat kidney cancer. Neither is Yervoy. But both are showing positive results. Other investors can see these abstracts, too. And they know what this means for treating cancer. This is why Bristol-Myers' stock is moving higher. We think Bristol-Myers is in prime position with these two immunotherapy drugs.

Stansberry's Investment Advisory subscribers are now up more than 35% since early October... and Porter and his research team believe there's more upside ahead.

![]() Another of our favorite health care stocks was in the news today...

Another of our favorite health care stocks was in the news today...

CVS Health (CVS) is the biggest prescription drug retailer in the U.S. It has agreed to buy Omnicare, the country's biggest provider of pharmacy services to nursing homes, for about $12.7 billion.

CVS will pay $98 per share in cash and assume $2.3 billion in debt.

Pharmacy services – the business of managing prescription-drug plans for employers and health-insurance companies – is growing rapidly as companies look to control rising drug and health care costs.

CVS is already the country's second-biggest pharmacy-services manager. Its pharmacy-services business is already growing faster than its retail-prescription business, and this deal should strengthen it further.

Shares of CVS rose nearly 3% to almost $104 a share, while shares of Omnicare rose almost 2% to more than $96 a share.

![]() Retirement Millionaire editor Dr. David "Doc" Eifrig recommended shares of CVS in 2011 to profit from one of the biggest, most important trends in the world today. Here's what he said in the June 2011 issue...

Retirement Millionaire editor Dr. David "Doc" Eifrig recommended shares of CVS in 2011 to profit from one of the biggest, most important trends in the world today. Here's what he said in the June 2011 issue...

The fastest-growing segment in the U.S. is the Baby Boomer crowd, the generation born between 1945 and 1964... Take a look at the chart below, which shows how the growth rate of 65 year olds in the population will explode in the next 20 years.

As Doc explained, more Americans growing old will lead to more demand for health care and pharmaceuticals...

Older people use three to four times the amount of prescription drugs as folks under 50. And more than 30 million people will gain Medicare coverage by 2014. This means an increasing number of written prescriptions.

Right now, only 10% of Medicare dollars are spent on pharmaceuticals. If Washington starts looking for cost-effective ways to manage health, prescription drugs will be a quick and easy way to test its hypothesis. In many cases, the use of drugs can ward off diseases for many years. For example, doctors already know blood-pressure pills and diabetes medications prolong lives cheaply.

This demographic shift means big opportunities for companies delivering drugs. Pharmaceuticals could easily grow to 15%-16% of the Medicare pie this decade. And the over-the-counter (OTC) markets will grow along with it.

![]() Doc also noted why CVS, specifically, was one of his favorite ways to profit from this trend...

Doc also noted why CVS, specifically, was one of his favorite ways to profit from this trend...

One of the reasons I like CVS more than other pharmacy businesses is it's just starting to see cost savings and operating efficiencies from its multiple mergers: in 2006 (MinuteClinic), in 2007 (Caremark), and 2008 (Longs drugstores, which brought it to the California, Hawaii, and Arizona markets).

The benefits of these mergers should increase as CVS continues to integrate dozens of pre-acquisition platforms used to deliver and manage the prescriptions and goods. The streamlining promises to save $3 billion-$4 billion in inventory (nearly 6%-8% of market capitalization).

![]() So far, Doc has been exactly right... As he predicted...

So far, Doc has been exactly right... As he predicted...

Companies that provide quality health care goods and services at fair prices to this aging U.S. population should make a fortune, no matter what happens in Washington.

Retirement Millionaire subscribers are up 175% as of yesterday's close.

![]() We've spent a lot of time lately praising True Wealth editor Steve Sjuggerud for his incredible call on Chinese stocks. But another one of Steve's highest-conviction trades is breaking out...

We've spent a lot of time lately praising True Wealth editor Steve Sjuggerud for his incredible call on Chinese stocks. But another one of Steve's highest-conviction trades is breaking out...

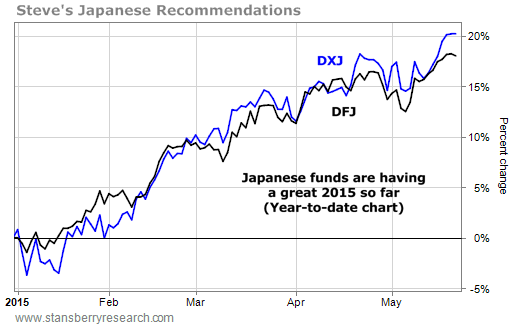

Yesterday, Japan's Nikkei 225 Index closed at a new 15-year high.

And as you'll notice at the end of today's Digest, Steve's two recommendations on Japan – the WisdomTree Japan Hedged Equity Fund (DXJ) and the WisdomTree Japan SmallCap Dividend Fund (DFJ) – just hit new 52-week highs, as well.

![]() Steve saw the bull market in Japan coming well in advance. In the January 2013 issue of True Wealth, he called Japanese stocks "The No. 1 Opportunity of 2013"...

Steve saw the bull market in Japan coming well in advance. In the January 2013 issue of True Wealth, he called Japanese stocks "The No. 1 Opportunity of 2013"...

[Japanese Prime Minister] Shinzo Abe is about to get his revenge... big time. And if you play your cards right, you could make A LOT of money from it...

In September 2007, the unpopular Abe resigned as Japan's leader. After his resignation, Japan's stock market (the Nikkei) fell by half. And the Japanese yen soared 40% versus the U.S. dollar. But now, Abe is back for his revenge...

This week, he swept Japan's elections – with a two-thirds majority! Abe won by promising to not repeat the same mistakes he made in 2006. In fact, he promises to do the exact opposite.

The promises he is making today, frankly, are a bit crazy. But that won't stop us from making a lot of money from them... As I will explain, I expect Abe's revenge will create a massive bubble in Japan's stock market, and trigger a potentially significant fall in Japan's currency.

Steve agreed to let us "unlock" the June 2013 issue of True Wealth. You can read it for free by clicking here.

![]() We've discussed how Abe's easing efforts have considerably weakened the Japanese yen. And in January, Steve noted that for the first time ever, five-year Japanese government bonds paid no interest. So investors could literally earn 0% giving their money to Japan's government for five years... or they could invest in Japanese stocks and exchange-traded funds (like DFJ and DXJ).

We've discussed how Abe's easing efforts have considerably weakened the Japanese yen. And in January, Steve noted that for the first time ever, five-year Japanese government bonds paid no interest. So investors could literally earn 0% giving their money to Japan's government for five years... or they could invest in Japanese stocks and exchange-traded funds (like DFJ and DXJ).

True Wealth subscribers are now up 82% on DXJ and 59% on DFJ. But Steve expects the rally to continue. In today's issue of our free DailyWealth e-letter, he explained why he's still bullish on Japanese stocks...

Surprisingly, Japanese stocks can (and should) continue higher...

They are not expensive yet (particularly by Japanese standards), and nobody is talking about them – yet. Typically, stock markets peak when both of these things happen. We are not there yet.

As we noted above, Steve originally recommended two exchange-traded funds to profit from the rally in Japanese stocks. But now he's recommending just one...

DXJ is no longer the IDEAL way to play it. (It is still good, I just think there's a better way.)

You see, at this point, there's no need to buy a special exchange-traded fund (ETF) that hedges the currency risk, like DXJ. The U.S. dollar soared. And the yen fell dramatically. Both of these moves were fairly extreme. So I don't expect there's a big need to avoid Japan's currency anymore through DXJ.

Instead, Steve says shares of DFJ are thebest way to invest in Japan...

While DXJ went up 87%, shares of DFJ are only up 36% in the same amount of time. DFJ is the WisdomTree Japan SmallCap Dividend Fund...

DFJ underperformed – significantly – because of the currency. But that move is behind us. DFJ is looking GREAT at the moment...

It's dirt cheap (with its underlying holdings trading around book value), it is completely ignored, and it just broke out to new highs (which is a very bullish sign).

In short, Japan still has plenty of room to run... And the ideal way to play it going forward is through DFJ – an ETF focusing on smaller companies in Japan that pay dividends.

![]() While Steve is still bullish on Japan, it's not his No. 1 recommendation today... that's China. Despite the gain his subscribers have already made in Chinese stocks, he has found an incredible new opportunity to profit from China. If you're not already a True Wealth subscriber, you can find out more about Steve's top recommendation with a risk-free trial subscription. Learn more by clicking here.

While Steve is still bullish on Japan, it's not his No. 1 recommendation today... that's China. Despite the gain his subscribers have already made in Chinese stocks, he has found an incredible new opportunity to profit from China. If you're not already a True Wealth subscriber, you can find out more about Steve's top recommendation with a risk-free trial subscription. Learn more by clicking here.

![]() New 52-week highs (as of 5/20/2015): Activision Blizzard (ATVI), Bristol-Myers Squibb (BMY), WisdomTree Japan SmallCap Dividend Fund (DFJ), WisdomTree Japan Hedged Equity Fund (DXJ), KraneShares E Fund China Commercial Paper Fund (KCNY), and Alleghany (Y).

New 52-week highs (as of 5/20/2015): Activision Blizzard (ATVI), Bristol-Myers Squibb (BMY), WisdomTree Japan SmallCap Dividend Fund (DFJ), WisdomTree Japan Hedged Equity Fund (DXJ), KraneShares E Fund China Commercial Paper Fund (KCNY), and Alleghany (Y).

![]() In the mailbag, clarifying a reader's confusion on put selling. Send your questions to feedback@stansberryresearch.com.

In the mailbag, clarifying a reader's confusion on put selling. Send your questions to feedback@stansberryresearch.com.

![]() "I have a hard time following Jeff Clark's examples. [In the May 19 Growth Stock Wire] He says, 'By selling uncovered puts, you actually get paid just for agreeing to buy a stock at a specified price. If the stock never drops to that price, you never have to buy it... But you still get to keep the money you collected for making the agreement.'

"I have a hard time following Jeff Clark's examples. [In the May 19 Growth Stock Wire] He says, 'By selling uncovered puts, you actually get paid just for agreeing to buy a stock at a specified price. If the stock never drops to that price, you never have to buy it... But you still get to keep the money you collected for making the agreement.'

Then he adds, 'In other words, we didn't need CENX to go up in order to make money. We just needed it to not fall to less than $12.80 per share. CENX closed at $13.79 last Friday. Subscribers who sold the CENX May $14 uncovered puts for $1.20 could now buy them back for just $0.25. That's a gain of $0.95 per share – on a stock that fell in value.'

"Why did he need to buy them back? He already said that if the stock never drops to that price ($12.80), then you never have to buy it. So if the stock dropped to $13.79, (well above $12.80), why didn't he just keep his entire $1.20? Why did he need to spend $.25 to buy them back? He confuses me." – Paid-up subscriber Jeff Kelsey

Brill comment: Jeff recommended his subscribers sell the CENX May $14 puts. If you took his advice, you would have received $120 per contract (or $1.20 per share, since one contract covers 100 shares) for opening the trade.

If shares closed for more than $14 on option-expiration day, you would keep the $120 free and clear. If shares closed at less than $14 on option-expiration day, you would be assigned 100 shares per contract. And as Jeff noted, it closed at $13.79 per share last Friday.

Had you done nothing, you would have been assigned 100 shares per contract at $13.79. But because you collected the premium upfront, that helps to offset a drop in the share price.

So you would have made money as long as shares traded for more than $12.80 ($14 minus $1.20 in premium). But if you wanted to avoid being assigned shares, you would have needed to close the trade before option expiration, since they were trading for less than the $14 strike price on Friday. We hope that clears up some of your confusion.

Regards,

Justin Brill

Delray Beach, Florida

May 21, 2015