One of the most flattering e-mails Porter has ever sent... Making 12.5% in 35 days... Big earnings from the country's top prescription provider... Siegel: The bull market isn't over... Sjuggerud: Higher interest rates mean higher stocks...

On Sunday, Porter sent us one of the most flattering e-mails we've ever received...

On Sunday, Porter sent us one of the most flattering e-mails we've ever received...

As we explained in the July 30 Digest, one of our employees recently invited a camera crew into his home to record him trading options with his personal money. It was his first time making this type of trade.

Regular Digest readers know we've espoused the benefits of selling put options for years... It's one of the safest and most consistent ways to generate income in the market. It's a skill every investor should have. Still, we know many of you have yet to sell a put option. So our quest to share this knowledge continues...

Most folks get scared when they hear the word "options." They think any trade involving options is risky or only for professional traders.

Even one of our company's directors hadn't sold puts yet... He has worked at S&A for years... And he has personally seen the rest of us make thousands of extra dollars a month using this strategy.

We knew if we could convince him that selling puts was a safe and profitable strategy, we could convince anyone.

So we brought a camera crew to his house... And we filmed him selling his first put option right from his kitchen counter.

Not only did we convince Jared to start selling puts... In the process, we also created a great primer for selling puts, which demonstrates just how easy and straightforward this strategy is. You'll see him make $320 in about five minutes.

In addition to receiving great feedback from our readers about this video, we also impressed Porter. He wrote...

|

We hope you'll take a moment to watch this video and see what all the fuss is about. And with many of the world's best companies down nearly double digits in the past couple months, now is the perfect time to learn how to sell puts.

The key is to identify high-quality companies whose shares you would like to own. By selling a put on that company, you name the price you're willing to pay for shares.

We'll walk you through an actual trade Dr. David "Doc" Eifrig recommended to his Retirement Trader subscribers earlier this year. It's no easy task choosing just one winning position from Doc... His track record is an amazing 178 winners out of 180 closed trading positions. In fact, for three years, Doc didn't close a single loser... He recommended 136 consecutive winning trading positions.

In March, we walked readers through a trade Doc recommended on drugstore chain CVS Caremark (CVS). CVS is highly profitable and is the country's No. 1 prescription provider. From that Digest...

|

Doc originally recommended shares of CVS in the June 2011 issue of Retirement Millionaire as a way to profit off the aging Baby Boomer generation and its growing dependence on medicine. From that issue...

|

CVS reported bullish earnings this morning, helping to confirm Doc's predictions. Net revenues and net income were both up 11% in the second quarter of 2014 compared with the same period in 2013. CVS generated $2.2 billion in free cash flow. Operating profits increased 12%, and adjusted earnings per share were up 17%. CVS is also one of the nation's largest pharmacy benefits managers (PBMs). Revenues from CVS' PBM segment were up 16% this quarter.

Altogether, it was a fantastic quarter for CVS shareholders. Including dividends, Retirement Millionaire subscribers are up nearly 120%.

Wharton professor Jeremy Siegel appeared on CNBC yesterday to reiterate his call for a bull market. We mentioned Siegel in the July 3 Digest when he said the Dow "could go to 20,000."

Siegel noted it has been a long time since we've had a correction, "but the bull market is definitely not over," he said.

Bull markets can go on for another nine months to two years after the Federal Reserve starts raising interest rates, he explained.

While he doesn't think we're currently in a correction, an actual correction would "be a great buying opportunity for investors."

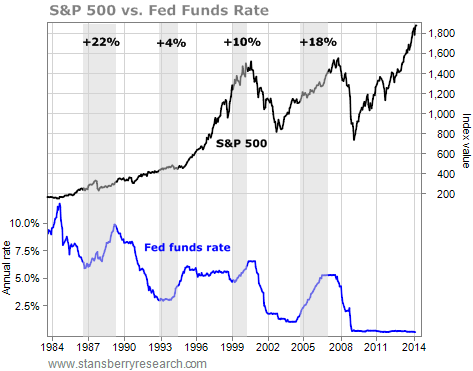

True Wealth editor Steve Sjuggerud has echoed Siegel's thoughts.

Steve believes the Federal Reserve will raise interest rates in April 2015... But he thinks the bull market can go on well past then.

History shows when the Fed raises rates, the market usually goes up. One reason for this is that the Fed will only increase interest rates (especially today) when it knows the economy is improving.

Steve showed the numbers in the March 10 DailyWealth...

|

Don't let the past few down days scare you out of the market. Instead, have a buy list ready... When your favorite stocks get cheap enough, scoop up shares. The trend is still up...

Don't let the past few down days scare you out of the market. Instead, have a buy list ready... When your favorite stocks get cheap enough, scoop up shares. The trend is still up...

New 52-week highs (as of 8/4/14): Berkshire Hathaway (BRK).

In today's mailbag, one Digest reader took advantage of the recent selloff to time a purchase of one of Porter's favorite companies... And another subscriber questions the quality of the products that the World Dominating Dividend Growers put out. Send your musings to feedback@stansberryresearch.com.

"I've been waiting for an opportunity to pick up some shares of Hershey (HSY) on the cheap. When I got Monday morning's DailyWealth Premium and saw that they had registered a new low last week, I quickly got into my trading account and checked it out. Their shares were down under $89 after being up over $100 a month ago! Looks like their announcement (and Mars') about price increases due to rising costs for ingredients, fuel, etc. put a funk in Mr. Market's outlook on their business.

New 52-week highs (as of 8/4/14): Berkshire Hathaway (BRK).

In today's mailbag, one Digest reader took advantage of the recent selloff to time a purchase of one of Porter's favorite companies... And another subscriber questions the quality of the products that the World Dominating Dividend Growers put out. Send your musings to feedback@stansberryresearch.com.

"I've been waiting for an opportunity to pick up some shares of Hershey (HSY) on the cheap. When I got Monday morning's DailyWealth Premium and saw that they had registered a new low last week, I quickly got into my trading account and checked it out. Their shares were down under $89 after being up over $100 a month ago! Looks like their announcement (and Mars') about price increases due to rising costs for ingredients, fuel, etc. put a funk in Mr. Market's outlook on their business.

"I quickly put in a bid and grabbed some shares at $88.94. I see that they are starting out today at $89.42, so I'm already ahead on that purchase. Thanks for providing the notice of that opportunity via your 'NEW LOWS OF NOTE LAST WEEK' section – not something you likely get much praise for! Just like Buffett said: 'Down days always make me feel good.' Now to go get some chocolate to enjoy... before the price goes up!" – Paid-up subscriber David G.

"S&A constantly touts McDonald's, Hershey's, and Coca-Cola as excellent companies to own, because they 'gush cash.' Fair enough. The majority who pay to read your material surely are interested primarily in profits, and rightly so. But I would like to point out that both McDonald's and Hershey's are leaders in putting out products that AT BEST could be described as mediocre, and these products get more so as we go along. In my opinion, Coca-Cola makes the best cola drink in existence, but the cola drink, in and of itself, is a mundane product. So, is that the secret to a company's success, to make and market a mediocre, commodity-grade product so efficiently as possible? Can this prism be applied when viewing other prospective acquisitions?" – Paid-up subscriber P.M.

Goldsmith comment: You don't pay us for our restaurant reviews. (Although we would argue McDonald's fries are better than "mediocre.") You pay us for our investment research. And the three companies you listed make products that are consistent all over the world and have made their consumers extremely loyal.

Can you get a better burger at a Manhattan steakhouse? Sure. We wouldn't argue that the Big Mac is the best burger in the world. But McDonald's serves millions of people around the world every day... and at low prices.

Because these companies have such strong brands and simple, straightforward business models, they're able to produce huge returns on assets without having to invest much back into the business (a concept Porter calls "capital efficiency"). So they're able to return more of that money to shareholders every year through share buybacks and growing dividends. From a financial perspective, that's all that matters. These are exceptional businesses to invest in when they go on sale.

Regards,

Sean Goldsmith

August 5, 2014

Why Goldman Sachs is wrong about Wal-Mart...

A research analyst at investment bank Goldman Sachs recently downgraded retail behemoth Wal-Mart from "buy" to "neutral." The analyst argues that Wal-Mart and other big-box retailers are losing market share to the Internet and "smaller, more conveniently located stores."

In today's Digest Premium, Dan Ferris – who holds shares of Wal-Mart in his Extreme Value newsletter – explains why Wal-Mart is not in serious danger from any competition...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

Why Goldman Sachs is wrong about Wal-Mart...

Editor's note: A research analyst at investment bank Goldman Sachs recently downgraded retail behemoth Wal-Mart from "buy" to "neutral." The analyst argues that Wal-Mart and other big-box retailers are losing market share to the Internet and "smaller, more conveniently located stores."

In today's Digest Premium, Dan Ferris – who holds shares of Wal-Mart in his Extreme Value newsletter – explains why Wal-Mart is not in serious danger from any competition...

Walk into your local dollar store. You won't see steaks, fresh vegetables, or just about anything else being sold at lower prices than at the biggest retailer in the world. If you can undercut Wal-Mart's prices and not lose money, you deserve to dethrone Wal-Mart. But that's hard... really hard.

For Costco to beat Wal-Mart on price, it has to move pallets per day of a single item. You can do that with 4,000 items in a warehouse store... but you can't do it with 150,000 items in a Wal-Mart superstore.

Now imagine buying fresh meat, fish, and vegetables online. You might be able to do that with your local grocery store. But it's going to be more expensive than Wal-Mart, and it doesn't appeal to millions of customers.

Are you going to buy an engagement ring at the dollar store? People do at Wal-Mart. It's the biggest jeweler in the country.

I don't believe for one second Wal-Mart can or will be replaced by Amazon or any dollar store.

On sheer scale, Dollar Tree and others are nowhere near displacing Wal-Mart in any meaningful way. Dollar Tree, Dollar General, and Family Dollar combine for less than $40 billion in annual sales.

Comparing Wal-Mart's online sales to Amazon's is a little silly. Wal-Mart does nearly $500 billion in sales. Amazon doesn't even do $100 billion. It's ridiculous. You can do a lot of things with $500 billion in sales that you just can't do with a few billion or even a few tens of billions.

I'll believe Goldman Sachs is right when Wal-Mart stops gushing free cash flow, can no longer cover its interest payments with ease, stops generating consistent profit margins, ceases to raise its dividend, stops buying back shares, and struggles to generate consistent returns on equity. Don't look for that to happen anytime soon.

– Dan Ferris

Editor's note: Wal-Mart is currently a "hold" in Dan's Extreme Value portfolio. But he recently told his subscribers about an opportunity he calls "the best resource opportunity of my career." This company sits on some of the most lucrative assets in North America... but has fewer than 20 full-time employees.

Dan believes this company could easily double from today's levels. And people who invest today could be sitting on a double-digit dividend yield within the next couple years. To learn more about Extreme Value – and this lucrative investment opportunity – click here.

Why Goldman Sachs is wrong about Wal-Mart...

A research analyst at investment bank Goldman Sachs recently downgraded retail behemoth Wal-Mart from "buy" to "neutral." The analyst argues that Wal-Mart and other big-box retailers are losing market share to the Internet and "smaller, more conveniently located stores."

In today's Digest Premium, Dan Ferris – who holds shares of Wal-Mart in his Extreme Value newsletter – explains why Wal-Mart is not in serious danger from any competition...

To continue reading, scroll down or click here.