The latest signs of a top...

The latest signs of a top... M&A is breaking records... Buybacks are soaring... All-time records in art... A $500 million palace... Markel: What do you think?...

We start today's Digest with the latest signs of a top...

We start today's Digest with the latest signs of a top...

Longtime readers know we are cautious on the market. We believe we're in the final innings of the Bernanke Asset Bubble, the huge bull market in U.S. asset prices fueled by the Federal Reserve's easy-money policies. And while we're not calling a top today, we are seeing more and more signs of the absurd behavior that often precedes a major peak in the market...

In recent months, we've discussed the sky-high valuations given to popular stocks like Tesla, GoPro, and Shake Shack... We've warned of "froth" in the global bond markets, particularly in high-yield – or "junk" – bonds... And we've noted the massive public interest in tech "startups" and venture capital investing, just to name a few.

Today, we're seeing more...

Last summer, we noted mergers and acquisitions (M&A) through the first half of 2014 hit seven-year highs. On Friday, news service Reuters reported M&A activity is set to break all-time records this year...

|

M&A activity is so hot, there's now a website dedicated entirely to speculating on the next big corporate takeovers. As CNBC journalist Herb Greenberg noted last week...

|

Companies are also continuing to buy back record amounts of their own stock...

According to a report in the Financial Times, analysts forecast U.S. companies will spend more than $1 trillion on share buybacks and dividends this year. From the FT...

|

Returning $1 trillion to shareholders sounds like great news for investors. But as Extreme Value editor Dan Ferris pointed out in the April 13 Digest, there's more to consider...

|

As Dan explained, that's much easier said than done...

|

We're also seeing signs of "froth" outside the stock market. Last month, two all-time sales records were broken in the art world...

According to the Washington Post, a 1955 painting by Pablo Picasso, titled "Women of Algiers (Version O)," sold for a record $179.4 million at London auction house Christie's. The sale set the record for the most expensive work of art ever sold at auction by more than $30 million. The previous record was set in 2013, when a painting by Francis Bacon sold for $142.4 million.

On the same night, a 1947 sculpture by Alberto Giacometti sold for $141.3 million, setting the record for most expensive sculpture in history, as well. From the article...

|

We could soon see an outrageous new record in the real estate market as well. Film producer and real estate developer Nile Niami is hoping to build the most expensive "spec" house in history...

When completed, the 100,000-plus square foot "palace" in the Los Angeles neighborhood of Bel Air will be one of the largest homes in U.S. history. And at the planned asking price, it would more than double the previous record for most expensive home in the world. Says Niami, "The house will have almost every amenity available in the world. The asking price will be $500 million..."

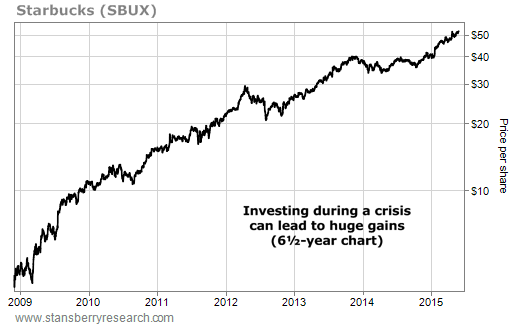

Again, we're not calling for a top today. The market can and likely will go higher. But we've seen enough to be cautious. As we've advised before, consider selling your riskiest stocks, watch your stop losses closely, and don't buy ridiculously overvalued assets. Speaking of records, shares of coffee chain Starbucks (SBUX) hit a new all-time high on Friday. Starbucks is undoubtedly one of the most popular stocks in the market... but unlike some of those we mentioned earlier, it's also a great business. As Editor in Chief Brian Hunt wrote in the Market Notes section of the March 18 DailyWealth...

|

Like many stocks, Starbucks isn't a bargain at today's levels. It's trading for more than 30 times earnings and 20 times its enterprise value to EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio.

But it is a good reminder of the power of buying great businesses at great prices. These opportunities don't come along every day, but they're incredibly profitable. In particular, Brian noted the fantastic opportunity Starbucks investors had during the financial crisis. As Brian explained...

|

As you can see from the chart below, buying shares of Starbucks in November 2008 – when nobody else wanted to – would have quickly generated impressive returns. Seven months later, shares doubled... three years after buying, you would be up 500%... and today, you would be up nearly 1,500%.

New 52-week highs (as of 5/29/15): eBay (EBAY). We received nearly 500 e-mails from subscribers offering their thoughts on whether insurance firm Markel (MKL) is cheap or expensive. Stay tuned for Porter's answer in tomorrow's Digest. In the meantime, if you haven't already, please send your answer to feedback@stansberryresearch.com. "I am going with cheap. EV/EBITDA of around 10 seems to be a good deal. Large operating cash flow and large revenues to EV as well. Price to book also not overly expensive. Great exercise!" – Paid-up subscriber AG "These are guesses because I really don't know, but it seems cheap. It's priced at 1.36 times book value, has enough cash to pay off all its debt, and costs a little more than two times revenue. I was trying to figure out profit per share, because I think you don't want to pay more than 10x that number, but I wasn't sure if I got it right. 1470M profit / 14M outstanding shares is 105 times profit, which I believe would be expensive, but that doesn't seem like the correct calculation.

New 52-week highs (as of 5/29/15): eBay (EBAY). We received nearly 500 e-mails from subscribers offering their thoughts on whether insurance firm Markel (MKL) is cheap or expensive. Stay tuned for Porter's answer in tomorrow's Digest. In the meantime, if you haven't already, please send your answer to feedback@stansberryresearch.com. "I am going with cheap. EV/EBITDA of around 10 seems to be a good deal. Large operating cash flow and large revenues to EV as well. Price to book also not overly expensive. Great exercise!" – Paid-up subscriber AG "These are guesses because I really don't know, but it seems cheap. It's priced at 1.36 times book value, has enough cash to pay off all its debt, and costs a little more than two times revenue. I was trying to figure out profit per share, because I think you don't want to pay more than 10x that number, but I wasn't sure if I got it right. 1470M profit / 14M outstanding shares is 105 times profit, which I believe would be expensive, but that doesn't seem like the correct calculation.

"Maybe market cap (which is value of all outstanding shares if I'm not mistaken) is the correct metric. 10.78B MC / 1.47B profit is only 7.3x profit, which would be cheap. For enterprise value (MC minus debt I believe) is 9.29B / 1.47B is still 6.3x, so still seems cheap. This email is just a brain dump as I look through the numbers. Curious if I'm even close." – Paid-up subscriber SA

"Markel is an insurance business so the first thing I would look at to estimate its value is the ratio of its market value to float + book value. Market value/(float+book value) = 0.60. So at a share price of $773 you are buying Markel at a 40% discount or $0.60 for a dollar. This looks good, just slightly above the $0.50 to the dollar that Buffett would consider cheap enough to buy and about the average discount you would expect for an insurance business. So at first look I would say that MKL is fairly priced at $773." – Paid-up subscriber DA "Looking at Markel over the previous three years reveals a stock that has risen from about $430 per share to about $770. Earnings per share have risen from $17 to $26.33 yet it pays no dividend. Its P/E of 29 is about twice the average of its peers. So it is expensive. Fair market value would be in the $500 per share range." – Paid-up subscriber HW

Regards,

Justin Brill

Baltimore, Maryland

June 1, 2015