Why Amazon could fall 80% from here...

Online retail giant Amazon recently announced it may significantly raise its subscription fees for its Prime service.

In today's Digest Premium, Paul Mampilly – a former securities analyst for a world-class hedge fund – explains why this could spell disaster for the stock...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

The second-worst February in history... Gold stocks are holding up... Home prices are up for 22nd straight month... Biotech is booming... Update on the best business in the world... J.C. Penney is getting slammed... Ackman minded his stops...

The S&P 500 and Dow Jones got hammered yesterday, both down more than 2%...

The S&P 500 and Dow Jones got hammered yesterday, both down more than 2%...

It was the worst February start for the S&P 500 since 1933. And that's on top of a horrid January.

We've enjoyed exceptional stock market gains since 2009... And whether or not more gains are to come, the trend is down today.

We've had occasional hiccups as the market has risen 150%-plus from the March 2009 bottom: the European credit crisis, the debt-ceiling debacle, and today, the rout in emerging markets...

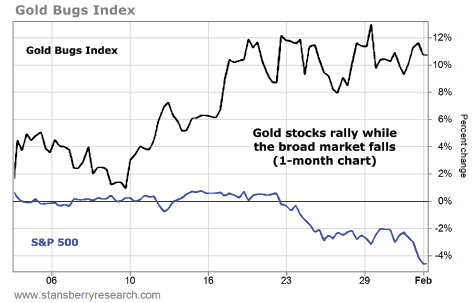

Despite the overall market's poor performance, some sectors have held up well during the selloff...

First, we have gold stocks, which S&A Editor in Chief Brian Hunt highlighted in today's DailyWealth Market Notes...

|

The spot price of gold fell slightly today. Meanwhile, the Market Vectors Gold Miners Fund (GDX) – which holds a basket of gold stocks – was up slightly.

S&A Short Report editor Jeff Clark noted the solid performance today in his real-time Direct Line blog. He said the "consolidation period is constructive" for gold and it "should help fuel another boost higher."

U.S. home prices are also on the rise... According to the latest data from financial-information service CoreLogic, home prices in December 2013 were up 11% from December 2012. That's the 22nd consecutive monthly increase. According to a press release from CoreLogic chief economist Dr. Mark Fleming...

|

Biotech stocks, which True Wealth editor Steve Sjuggerud recommended in January 2012, are blowing the market away.

Last year, the benchmark Nasdaq Biotech Index was up 66% – more than double the S&P 500's 32% gain. True Wealth readers are up 110% on the iShares Nasdaq Biotechnology Fund (IBB).

In his latest True Wealth, Steve said the sector could move even higher...

|

So far, in 2014, Steve has been correct. Shares of IBB are up 7%... Meanwhile, the S&P 500 is down 5%.

Steve summed up the lesson for readers who were hesitant to buy these outperforming sectors due to their large rises last year:

|

Insurance stocks are struggling this year. Still, it's one of Porter's favorite sectors in the market. He even calls insurance "the greatest business in the world." The reason is simple. Berkshire Hathaway founder and investment legend Warren Buffett summed it up in his 2011 shareholder letter...

|

In other words, insurance companies enjoy a positive cost of capital. (While most companies have to pay for capital, a well-run insurance company is paid to accept it.)

Despite their business advantage, insurance companies haven't been immune to the broad market selloff, falling 11% this year.

We asked Bryan Beach, a lead analyst for Stansberry's Investment Advisory, for an update on the sector...

|

Bryan will share more of his thoughts (and top names in the sector) in next week's Stansberry Data, a supplementary publication to Stansberry's Investment Advisory. The only way to gain access to Stansberry Data is to be a lifetime subscriber to Stansberry's Investment Advisory (or join the S&A Alliance). To learn more about this offer – and gain access to Bryan's list of top insurance companies – click here. (You won't have to sit through a long promotional video.)

We'll end today's Digest with an update on one of our favorite short-sale candidates of all time, department-store chain J.C. Penney.

The J.C. Penney saga is a long one. We've written volumes on the topic. To sum things up...

Hedge-fund manager Bill Ackman took a large stake in J.C. Penney in October 2010 and hired former head of Apple retail Ron Johnson to help turn the company around. The company was bleeding cash and losing customers. The stock got crushed. We recognized a failing business for what it was... But Ackman held on.

Johnson left the company in April 2013. Ackman sold his stake last summer for a $500 million loss. But it could have been much, much worse...

Today, J.C. Penney shares tumbled 12% to around $5 a share – a new all-time low – despite reporting an increase in sales during the holidays. If Ackman still owned shares today, his initial $1 billion position would be worth less than $200 million.

New 52-week highs (as of 2/3/14): Aware (AWRE) and Virginia Mines (VGQ.TO).

Nothing of note in today's mailing. Come on... haven't we done anything lately to make you angry? Send your e-mails to feedback@stansberryresearch.com.

Regards,

Sean Goldsmith

Miami Beach, Florida

February 4, 2014

Why Amazon could fall 80% from here...

Editor's note: Today's Digest Premium is adapted from a conversation with our friend Paul Mampilly, a former securities analyst for a world-class hedge fund...

![]()

On January 30, shares of online retail giant Amazon fell 11% after a disappointing earnings announcement.

I (Paul Mampilly) was bearish on the stock going into the announcement. (The company's margins are razor-thin, and it was trading for 100 times earnings.) And even after the fall, I continue to be bearish today...

After reviewing Amazon's earnings conference call, I can see Amazon stock falling 80% from its peak of $408. I know that seems far-fetched, but stick with me...

Amazon wants to raise prices on its popular Prime membership program, which has generated huge sales growth for the company.

An Amazon Prime membership is great for anyone who likes to shop online. You pay $79 a year and you get free two-day shipping on anything you order from Amazon (shipped from Amazon's warehouses). Prime also gives you free access to streaming movies and TV programs.

Amazon doesn't reveal how many Prime members it has. But analysts estimate it's around 25 million people, or around $2 billion a year.

But Amazon Prime is too good of an offer... There's no way it can last. Once people started ordering loads of goods from Amazon, the $79 annual membership was never going to be enough to cover shipping costs. That's what happened last Christmas, when Amazon added 1 million Prime members.

On top of that, the cost of getting licenses to stream movies and TV programs is also going up – thanks to mounting competition from Netflix and other streaming services.

Amazon has no choice but to wring its golden goose. The company announced it wants to raise Prime membership fees to $119 – a 51% increase.

You may think the extra $40 a year is chicken feed. But the story reminds me of when Internet video-streaming company Netflix tried to spin off its DVD rental business in 2011 as "Qwikster"... Which caused investors to flee from the stock, sending shares down more than 75%.

A 51% increase in Amazon Prime subscription costs could cause a similar exodus.

– Paul Mampilly

Why Amazon could fall 80% from here...

Online retail giant Amazon recently announced it may significantly raise its subscription fees for its Prime service.

In today's Digest Premium, Paul Mampilly – a former securities analyst for a world-class hedge fund – explains why this could spell disaster for the stock...

To continue reading, scroll down or click here.

Stansberry & Associates Top 10 Open Recommendations

(Top 10 highest-returning open positions across all S&A portfolios)

As of 02/03/2014

| Stock | Symbol | Buy Date | Return | Publication | Editor |

| Prestige Brands | PBH | 05/13/09 | 373.0% | Extreme Value | Ferris |

| Enterprise | EPD | 10/15/08 | 257.6% | The 12% Letter | Dyson |

| Constellation Brands | STZ | 06/02/11 | 255.7% | Extreme Value | Ferris |

| Ultra Health Care | RXL | 03/17/11 | 200.6% | True Wealth | Sjuggerud |

| Fluidigm | FLDM | 08/04/11 | 197.8% | Phase 1 | Curzio |

| Ultra Nasdaq Biotech | BIB | 12/05/12 | 181.2% | True Wealth Sys | Sjuggerud |

| Altria | MO | 11/19/08 | 163.8% | The 12% Letter | Dyson |

| McDonald's | MCD | 11/28/06 | 163.2% | The 12% Letter | Dyson |

| Ultra Health Care | RXL | 01/04/12 | 162.5% | True Wealth Sys | Sjuggerud |

| Hershey | HSY | 12/06/07 | 162.3% | SIA | Stansberry |

Please note: Securities appearing in the Top 10 are not necessarily recommended buys at current prices. The list reflects the best-performing positions currently in the model portfolio of any S&A publication. The buy date reflects when the editor recommended the investment in the listed publication, and the return shows its performance since that date. To learn if a security is still a recommended buy today, you must be a subscriber to that publication and refer to the most recent portfolio.

| Top 10 Totals |

| 2 | Extreme Value | Ferris |

| 3 | The 12% Letter | Dyson |

| 1 | True Wealth | Sjuggerud |

| 1 | Phase 1 | Curzio |

| 2 | True Wealth Sys | Sjuggerud |

| 1 | SIA | Stansberry |

Stansberry & Associates Hall of Fame

(Top 10 all-time, highest-returning closed positions across all S&A portfolios)

| Investment | Sym | Holding Period | Gain | Publication | Editor |

| Seabridge Gold | SA | 4 years, 73 days | 995% | Sjug Conf. | Sjuggerud |

| Rite Aid 8.5% bond | 4 years, 356 days | 773% | True Income | Williams | |

| ATAC Resources | ATC | 313 days | 597% | Phase 1 | Badiali |

| JDS Uniphase | JDSU | 1 year, 266 days | 592% | SIA | Stansberry |

| Silver Wheaton | SLW | 1 year, 185 days | 345% | Resource Rpt | Badiali |

| Jinshan Gold Mines | JIN | 290 days | 339% | Resource Rpt | Badiali |

| Medis Tech | MDTL | 4 years, 110 days | 333% | Diligence | Ferris |

| ID Biomedical | IDBE | 5 years, 38 days | 331% | Diligence | Lashmet |

| Northern Dynasty | NAK | 1 year, 343 days | 322% | Resource Rpt | Badiali |

| Texas Instr. | TXN | 270 days | 301% | SIA | Stansberry |