Stansberry & Associates Hall of Fame

(Top 10 all-time, highest-returning closed positions across all S&A portfolios)

| Investment | Sym | Holding Period | Gain | Publication | Editor |

| Seabridge Gold | SA | 4 years, 73 days | 995% | Sjug Conf. | Sjuggerud |

| Rite Aid 8.5% bond | 4 years, 356 days | 773% | True Income | Williams | |

| ATAC Resources | ATC | 313 days | 597% | Phase 1 | Badiali |

| JDS Uniphase | JDSU | 1 year, 266 days | 592% | SIA | Stansberry |

| Silver Wheaton | SLW | 1 year, 185 days | 345% | Resource Rpt | Badiali |

| Jinshan Gold Mines | JIN | 290 days | 339% | Resource Rpt | Badiali |

| Medis Tech | MDTL | 4 years, 110 days | 333% | Diligence | Ferris |

| ID Biomedical | IDBE | 5 years, 38 days | 331% | Diligence | Lashmet |

| Northern Dynasty | NAK | 1 year, 343 days | 322% | Resource Rpt | Badiali |

| Texas Instr. | TXN | 270 days | 301% | SIA | Stansberry |

A major way geniuses make their lives more difficult...

Bestselling author Robert Greene says certain character traits in some geniuses cause them problems. In today's Digest Premium, he explains how...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

Turning to gambling... Seth Klarman on gold... Sjuggerud: Gold has bottomed... Singer on Bitcoin and gold... Huge win for Phase 1... Google's $10 billion hiccup... Big earnings from Facebook and Blackstone... It's the last day to hear Jeff's prediction...

The Federal Reserve is forcing folks to gamble...

The Federal Reserve is forcing folks to gamble...

When inflation outpaces interest rates, savers are losing money by sitting in cash... We're forced to gamble by buying riskier assets like stocks and bonds.

There are few safe places to earn large yields today... Some blue-chip stocks yield between 3% and 5% (like software icon Microsoft, semiconductor giant Intel, and cigarette maker Philip Morris International, which we discussed yesterday). You can also buy certain municipal-bond funds for a discount to net asset value and earn a double-digit, tax-equivalent yield.

Regardless, we've become a nation of gambling speculators. Even the most conservative investors are forced to move out of their comfort zone to protect themselves.

Take Baupost Group hedge-fund manager Seth Klarman, for example. Klarman is notoriously secretive about his investing... And he's ultraconservative, buying only the cheapest assets.

In November, at the Grant's Interest Rate Observer Conference in New York, he told the crowd he was returning some money to investors for lack of opportunities. As of October 2013, Klarman had $14 billion of his $30 billion fund in cash. He told people at the conference...

|

Like us, Klarman believes the Fed's loose monetary policy will eventually lead to higher interest rates and a loss of faith in government paper.

Also in attendance at the Grant's conference was our own Dan Ferris. In a weekly update to his Extreme Value subscribers, Dan explained how Klarman is trading in gold...

|

There you have it. A conservative value investor is buying call options on gold.

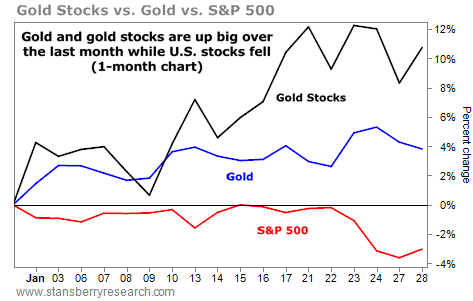

Meanwhile, Steve Sjuggerud says the bottom in gold is officially in. From today's DailyWealth:

|

Billionaire Paul Singer, who manages the Elliott Management hedge fund, also discussed gold and virtual currency Bitcoin in his quarterly letter to investors...

|

We agree with Singer: Gold is our alternative currency of choice.

Phase 1 Investor readers just enjoyed a major score...

In the November issue, editor Frank Curzio told readers about a tiny company named Vringo. In October 2012, Vringo took tech giant Google to court over two patents. These patents cover a process of directly tying advertisements to the things people search for on the Internet. Part of this process involves incorporating user feedback – like which ads you click on – into the system so it can tailor future listings that match your interests.

In late 2012, the court ruled that Google's "AdWords," the ad displays you see with every Google search, infringed upon Vringo's patents. Frank believed the courts could force Google to pay Vringo hundreds of millions of dollars in royalties for continuing to use the technology (a huge amount for a small-cap tech company worth less than $300 million).

Even after the initial victory, Vringo argued Google's AdWords was still the same, and Google was still "willfully" infringing on the company's patents. Yesterday, Frank sent subscribers a special update...

|

Vringo rocketed 30% on the news. And Phase 1 readers sold half their position for an 85% gain in less than three months.

A little more Google schadenfreude...

No tech company's rise to dominance is complete without a few horrid acquisitions and subsequent 11-figure writeoffs.

Yesterday, the search-engine giant announced it sold its Motorola Mobility handsets division to Lenovo for $2.9 billion.

Google purchased the division in May 2012 for $12.5 billion. In the first nine months of last year, the division lost $645 million.

It's a move straight from Microsoft's playbook... The software giant has burned around $22 billion on bad acquisitions since 2007. And most recently, it purchased Nokia's Devices & Services business for $5.1 billion and a 10-year license on its patents for $2.2 billion.

Given its history of bad acquisitions and inability to successfully produce hardware, Dan Ferris was skeptical. As he told Extreme Value readers in an October update...

|

Still, it's hard to overlook the company's consistently high returns on equity... consistent profit margins... gushing free cash flow... financial fortress balance sheet... and shareholder friendliness via share repurchases and growing dividends. That's why Microsoft has been a stalwart in the Extreme Value portfolio since 2006.

Two quick earnings updates...

Shares of social-networking behemoth Facebook jumped more than 15% to a record high on strong earnings.

Facebook earned $523 million for the quarter, up from $64 million a year ago. Mobile users grew 39% to 945 million. And the company's mobile ad revenue was 53% of total revenue for the fourth quarter – the first time it comprised more than half the total ad revenue.

Private-equity giant Blackstone Group announced record fourth-quarter earnings. Shares rallied nearly 5% to a new high.

Blackstone earned $621 million in the quarter, up from $106 million a year earlier. The company profited from cashing in on several deals – including deals involving hotel group Hilton Worldwide, theme park Sea World, packaged-foods company Pinnacle Foods, and global-information company Nielsen Holdings (best known for its TV ratings). Blackstone made around a $10 billion profit on Hilton alone, which it sold to the public last year.

Blackstone's assets under management increased 7.1% from the third quarter, to $265.8 billion. It brought in $17 billion in the fourth quarter.

On the company's earnings call, Blackstone President Tony James expressed his bullishness about 2014... James said the U.S. economy is strengthening. And he expects Blackstone to take seven to eight companies public this year.

"There are definitely more tailwinds than headwinds. I personally believe that the IPO window will stay open for another year," he said. And "real estate continues to rock."

True Wealth readers are up 138% on the recommendation since November 2012.

Today is your last chance to hear Jeff Clark's big prediction...

Federal Reserve Chairman Ben Bernanke is leaving his post tomorrow. Bernanke has inflated the Fed's balance sheet to $4 trillion – the highest in history. And while he tapered the Fed's purchases of bonds from $85 billion a month to $65 billion, the damage has already been done.

Jeff believes certain factors tied to Bernanke's exit could lead us to another 2008-type market collapse. But here's the bright side... 2008 was the best year in Jeff's 30-year career. He made 10 different recommendations that more than doubled readers' money.

You can listen to Jeff's prediction – and get a special offer to receive a free year of the S&A Short Report – until midnight tonight. After that, we're taking it down. Click here to learn more.

New 52-week highs (as of 1/29/14): Aware (AWRE), National Fuel Gas (NFG), Virginia Mines (VGQ.TO), and Vringo (VRNG).

Quiet mailbag today... Send your notes to feedback@stansberryresearch.com.

"I disagree with Porter's grade of F for S&A Short Report. The grade is purely based on 'official' recommendations, but that should not be the only gauge on this newsletter. Different from other Stansberry newsletters, we received real-time insight into the market from Jeff Clark, many although not official, were very beneficial for subscribers." – Paid-up subscriber SL

Regards,

A major way geniuses make their lives more difficult...

Editor's note: Today's Digest Premium is adapted from James Altucher's conversation with bestselling author Robert Greene from episode 116 of Stansberry Radio...

![]()

The laws of human nature go back thousands of years.

It's sort of like looking at humans as if we are animals that behave according to particular patterns of behavior. And I'm going to give you a codebook so that you can understand the weird behavior of the people that you deal with, that's the general idea.

Social intelligence is more like 20%-25% of the game. So let's say that you are really brilliant. You are like an Einstein. You are a tech genius or a business genius, but you have really bad people skills. You are kind of pushy. You don't listen.

You are negating all that talent. Going to Princeton and getting your degree and all that hard work is completely neutralized by your horrific people skills. People who have real skill, who have mastered a craft of any kind, are going to run the world in the future. And it's not just about being a great nerd... we are social animals. Everything you do involves other people. You are continually having to sell your ideas. If you are terrible at it, you are going to be miserable.

In my newest book, there's this doctor. He could have been greater than famed chemist Louis Pasteur, but he offended everybody he came in contact with. So it's not everything. It's not all about being political and being a BS artist and knowing how to charm people. That has its limitations, too, but depending on what field you are in, you have to have some degree of awareness of people and how they are thinking.

Say you just entered a new environment and suddenly somebody is super friendly to you. It takes you off-guard and you are charmed. What's happening is that he or she envies you to a degree. They are setting you up for some kind of negative action, because people generally are a little wary when they first meet each other. Somebody who is super overly friendly on the first encounter is a sign of something wrong.

– Robert Greene

![]()

Editor's note: The newest member of the S&A Radio stable – The James Altucher Show – is currently the top-ranked business podcast on iTunes. To sign up to receive episodes of The James Altucher Show for free, click here and subscribe on iTunes. And to receive a free gift, e-mail him at james@stansberryradio.com with the subject line "Podcast Subscriber."

A major way geniuses make their lives more difficult...

Bestselling author Robert Greene says certain character traits in some geniuses cause them problems. In today's Digest Premium, he explains how...

To continue reading, scroll down or click here.

Stansberry & Associates Top 10 Open Recommendations

(Top 10 highest-returning open positions across all S&A portfolios)

As of 01/29/2014

| Stock | Symbol | Buy Date | Return | Publication | Editor |

| Prestige Brands | PBH | 05/13/09 | 378.0% | Extreme Value | Ferris |

| Constellation Brands | STZ | 06/02/11 | 266.4% | Extreme Value | Ferris |

| Enterprise | EPD | 10/15/08 | 252.0% | The 12% Letter | Dyson |

| Ultra Health Care | RXL | 03/17/11 | 207.0% | True Wealth | Sjuggerud |

| Ultra Nasdaq Biotech | BIB | 12/05/12 | 192.7% | True Wealth Sys | Sjuggerud |

| Altria | MO | 11/19/08 | 177.9% | The 12% Letter | Dyson |

| Fluidigm | FLDM | 08/04/11 | 173.0% | Phase 1 | Curzio |

| Ultra Health Care | RXL | 01/04/12 | 168.1% | True Wealth Sys | Sjuggerud |

| GenMark Diagnostics | GNMK | 08/04/11 | 163.8% | Phase 1 | Curzio |

| McDonald's | MCD | 11/28/06 | 163.5% | The 12% Letter | Dyson |

Please note: Securities appearing in the Top 10 are not necessarily recommended buys at current prices. The list reflects the best-performing positions currently in the model portfolio of any S&A publication. The buy date reflects when the editor recommended the investment in the listed publication, and the return shows its performance since that date. To learn if a security is still a recommended buy today, you must be a subscriber to that publication and refer to the most recent portfolio.

| Top 10 Totals |

| 2 | Extreme Value | Ferris |

| 3 | The 12% Letter | Dyson |

| 1 | True Wealth | Sjuggerud |

| 2 | True Wealth Sys | Sjuggerud |

| 2 | Phase 1 | Curzio |