GameStink 'only' down 26% in the past week; The SPAC boom; Short Sellers Boost Bets Against SPACs; Opportunities in the SPAC sector; Cheers and Jeers: Ackman donates $1.3 billion to charity; Ticket resellers

1) In last Friday's e-mail, I predicted that GameStink's (GME) stock would "be down by 30% within a week, 50% within a month, and 80% within six months."

Well, my first prediction was close: As of earlier this morning, the stock is down 26%! I stand by my other two forecasts...

2) I last wrote about special purpose acquisition companies ("SPACs") in my February 17 e-mail. Excerpt:

SPACs set an all-time record last month... raising nearly $26 billion in January...

SPACs have come to dominate the initial public offering ("IPO") market over the past eight months (in fact, in the first six weeks of this year, SPACs have raised $38.3 billion... nearly double the $19.8 billion from traditional IPOs)...

The sector is definitely getting frothy... and there's no way that these 300-plus SPACs, as a group, will do well.

This article in the Financial Times has the latest data through March 16: SPAC boom eclipses 2020 fundraising record in single quarter. Excerpt:

Blank-cheque companies have already surpassed last year's fundraising record in the first quarter of 2021, reflecting the insatiable appetite for special purpose acquisition companies among both institutional and retail investors.

SPACs have raised $79.4bn globally since the start of the year, eclipsing the $79.3bn that flooded into vehicles in 2020, according to data provider Refinitiv, as of Tuesday night. So far in 2021, 264 new SPACs have been launched, overtaking last year's record 256.

As a result of so many IPOs, too much money is likely chasing too few deals, as this article in today's New York Times highlights: 'The Market Seems Crazy': Start-Ups Wrestle With Flood of Offers. Excerpt:

Dozens of SPACs began e-mailing Mr. Schaffer through their advisers, investors, bankers and other middlemen. Eventually, the interest became so overwhelming that, he said, he stopped responding to new inquiries. Even his accountant had a SPAC hookup.

"The market seems crazy," Mr. Schaffer said. "They want to go so fast."

Many start-ups are being similarly deluged as SPACs have kicked off an extraordinary dealmaking frenzy. In recent months, these investment vehicles – also known as "blank-check companies" – have pulled out all sorts of tactics to make deals with target companies. Their strategies include offering stratospheric values, dangling incentive bonuses and recruiting celebrities like Sammy Hagar and Shaquille O'Neal to their advisory boards to lend some star power.

And if all else fails? They badger the start-ups.

The activity has ramped up as SPACs have proliferated and chase a limited pool of potential targets. The financial vehicles, which are publicly traded shell companies with no operations, are structured to hunt for deals. They raise money from investors, take the shell company public and promise that they will find a private company to merge with. If that is successful, the target company then takes over the shell and becomes publicly traded. The sponsor gets a stake, typically 20 percent, of the shell company.

For years, these vehicles had a shady reputation. That changed last year as the market surged – and there may now be too many SPACs. So far this year, 264 of them have raised $76.7 billion in public offerings, topping the $75.5 billion that was raised in all of 2020, according to Renaissance Capital, which tracks listings. The blank check companies have outnumbered traditional initial public offerings – which are also booming – by nearly a four-to-one ratio.

Not having enough start-ups to merge with is a problem because SPACs face a ticking clock. If they do not complete a deal within two years, the special purpose vehicle dissolves and investors get their money back.

"There is intense pressure to find good targets," said Julie Copeland, a partner at StoneTurn, which advises companies and investors on regulatory and compliance issues. "Not a lot of firms want to say, 'Gee, we couldn't find a target.'"...

Andrew Dudum, chief executive of Hims & Hers, a telehealth company, said he was initially skeptical of SPACs but began taking meetings to learn about them last year – and was quickly overwhelmed by suitors.

"There's an endless number of teams out there with capital," he said. "Everyone and their grandma has a SPAC."

3) The sector has taken a bit of a breather in recent weeks, however, with the SPAC and New Issue Fund (SPCX) declining roughly 10% from its recent peak.

Short sellers are circling, as this Wall Street Journal article highlights: Short Sellers Boost Bets Against SPACs. Excerpt:

Short sellers are coming for SPACs.

Investors who bet against stocks are targeting special-purpose acquisition companies, one of the hottest growth areas on Wall Street. The dollar value of bearish bets against shares of SPACs has more than tripled to about $2.7 billion from $724 million at the start of the year, according to data from S3 Partners.

Some of the stocks under attack belong to large SPACs that surged in recent months, in part because they were backed by high-profile financiers. A blank-check company created by venture capitalist Chamath Palihapitiya that plans to merge with lending startup Social Finance is a popular target, with 19% of its shares outstanding sold short, according to data from S&P Global Market Intelligence. The short interest in Churchill Capital IV (CCIV), a SPAC created by former investment banker Michael Klein that is merging with electric-vehicle startup Lucid, more than doubled in March to about 5%.

Others are wagering against companies after they combine with SPACs.

Here are two recent short reports on SPACs:

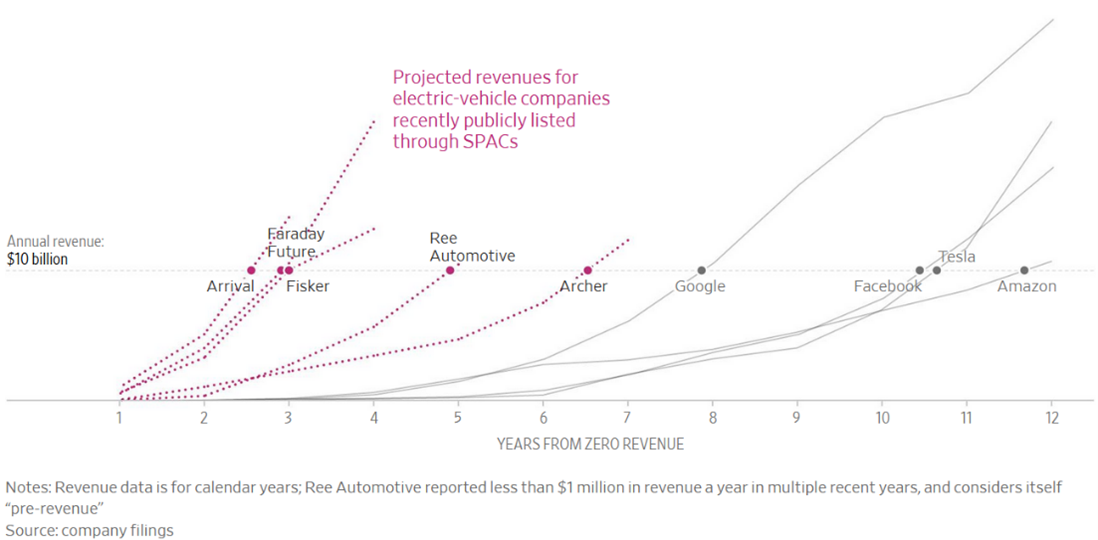

There's undoubtedly a lot of foolishness in the sector. Take a look at the absurd revenue projections of various electric-vehicle startups going public via SPACs, which the Wall Street Journal summarizes in this article: Electric-Vehicle Startups Promise Record-Setting Revenue Growth. Excerpt:

It took Google eight years to reach $10 billion in sales, the fastest ever for a U.S. startup. In the current SPAC frenzy, a spate of electric-vehicle companies planning listings are vowing to beat its record – in some cases by several years.

Among the most ambitious are luxury-car maker Faraday Future, U.K.-based electric-van and bus maker Arrival, and auto maker Fisker (FSR). Each has disclosed plans to surpass the $10 billion revenue mark within three years of launching sales and production...

The forecasts for record-setting growth illustrate the extent of the fervor for electric-vehicle startups, particularly for those going public by merging with SPACs, which are shell firms that list on a stock exchange with the sole purpose of acquiring a private company to take it public. More than 10 electric-vehicle or battery companies that struck deals with SPACs have been valued in the billions of dollars before producing any revenue, as amateur traders and many traditional investors have flocked to the buzzy sector.

4) While this is a risky sector to invest in, opportunities are presenting themselves amidst the pullback.

In particular, a number of SPACs that have announced deals are trading near $10 per share. Since investors can take $10 in cash any time before the deal closes, this presents an attractive risk/reward setup. As we explained in the latest issue of Empire Investment Report:

That means one of two things will happen...

- If investors as a whole decide that the SPAC's announced deal isn't worthy of the cash raised, the deal will fail the shareholder vote. The cash will remain in trust and the SPAC will either have to find a better deal or return the money to shareholders.

- If shareholders approve the vote, the deal will go through. The stock will soon represent shares in the target company. But this also means by definition that the majority of investors think the stock is worth more than $10.

Once the deal is complete, it's no longer a SPAC... It's a company with its own future. Some will succeed and some will fail. But we know that at least if a deal has been approved, the shareholders believe that even with the future uncertain, the stock is worth more than $10 in cash.

Another way to take advantage of this opportunity is to buy the warrants of certain SPACs whose shares are trading around $10... and my colleague Enrique Abeyta recently identified six of these in the latest issue of his Empire SPAC Investor newsletter.

In summary, if you're going to invest in this sector, you need a savvy guide who knows it backward and forward... and there's nobody better than Enrique. Since launching Empire SPAC Investor in October, he has recommended seven SPACs (excluding his most recent issue) – including one that has already doubled!

Click here to sign up for Empire SPAC Investor. If you're not satisfied for any reason, just call our customer service team within 30 days and we'll give you a full credit, which you can apply to any other Empire Financial Research product.

5) Moving on to my latest cheers and jeers...

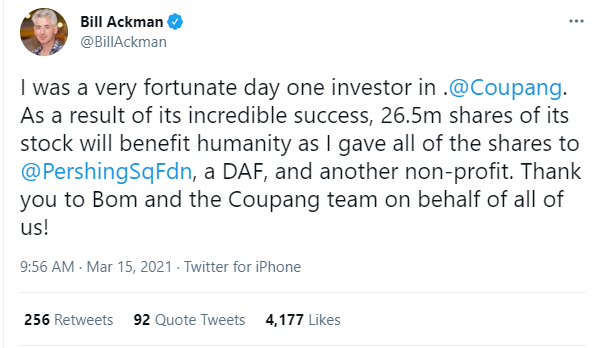

Cheers to my friend Bill Ackman, who was a day-one (personal) investor in the Amazon (AMZN) of South Korea, Coupang (CPNG), which just went public on the New York Stock Exchange at a roughly $80 billion market cap. In this tweet, Bill announced that he's donating all of his 26.5 million shares, worth $1.2 billion, to three charities:

I'm on the board of the primary beneficiary, the Pershing Square Foundation, and look forward to helping Bill put his incredible gift to work!

6) And jeers to ticket resellers like StubHub. This article will make your blood boil: How Is This Legal? Excerpt:

Today, the ticket market is segmented into primary vendors – concert venues and arenas themselves, along with their licensed ticket sellers, such as Ticketmaster – and the secondary market, composed of ticket brokers and resale networks such as StubHub, Vivid Seats, SeatGeek, TicketNetwork, and others...

Today, that dynamic has been supercharged online, with a multimillion-dollar industry ballooning to a market worth roughly $15 billion. Ticket resale is no longer driven by fast-talkers peddling their wares outside U.S. arenas. Now it's effectively dominated by software companies.

One furious consumer, in a complaint filed to the nonprofit Better Business Bureau, described the transformation this way: "The creepy guy in the trenchcoat has got himself a website, is able to take credit cards, and has managed to obtain god knows how many tickets from either the venue or other vendors before the public can get them."

Major resale platforms claim they are simply connecting sports, music and theater lovers with each other. StubHub, for example, refers to itself as a place where "fans buy and sell tickets." Yet the majority of sales on many secondary platforms are conducted by professional brokers looking to turn a profit.

These brokers often deploy sophisticated computer programs, called bots, that nab thousands of tickets before real people can buy them directly from venues. Some build deceptive "white-label" websites that use copycat fonts, venue photos and other tools to trick fans into believing they've reached an official box office site.

Others sell so-called speculative tickets, which the brokers do not actually yet possess. Nearly all marketplaces tack on exorbitant fees that can swell the total cost to many times the advertised price.

Best regards,

Whitney