Implications for the war and markets of the Russian coup attempt; Inflation expectations declining; Who's to Blame for All Those Hidden Fees? We Are

1) I spent much of the weekend following the aborted coup in Russia and thinking about the implications for the war in Ukraine and on markets.

It's clear that Russian President Vladimir Putin has been severely weakened. That said, I think it's likely that he'll be able to hold on to power for a while. (The betting markets agree: For example, SMarkets says he's 72% likely to be the winner of the presidential election scheduled for next March.)

As for the war, this weekend's events are unquestionably great news for Ukraine, for two reasons.

First, given that Putin's first priority is personal survival and that there's a direct line between his failed invasion and this weekend's events that threatened him, it's possible that he'll look for an exit – perhaps by blaming his generals for the debacle and accepting a deal like the one I've outlined in previous e-mails in which Russia withdraws from Ukraine, but certain areas like Crimea are demilitarized, with UN peacekeepers.

Sadly, however, I think this is unlikely.

Instead, Putin will figure that, even more than ever now, he can't afford to look weak, so the situation a few days ago is still the situation today: The only way peace will come to Ukraine is when Ukrainian forces drive every last Russian off their soil, which is going to be very costly and difficult.

That said, this task has gotten somewhat easier thanks to the coup attempt for a variety of reasons...

- Lower morale among Russian forces (I'm reminded of John Kerry's searing question in 1971: "How do you ask a man to be the last man to die for a mistake?")

- Their most effective fighting unit, Wagner, has been weakened

- Eight aircraft were destroyed, and

- There were significant disruptions to supply chains

For these reasons, I think the odds that the war ends this year – which would give the markets a huge boost – have risen from 50% to 65% (note that this a very out-of-consensus view).

If you're interested in more commentary, here are links to the best articles I read over the weekend:

- Putin's War on Ukraine Backfires, Leading to Wagner Uprising (WSJ)

- Why Wagner Chief Prigozhin Turned Against Putin (WSJ)

- After Chaos in Russia, Questions Remain Over Wagner's Fate (WSJ)

- Putin's humiliation means new dangers for Russia – and the world (WaPo)

- Revolt Raises Searing Question: Could Putin Lose Power? (NYT)

- 'A huge humiliation': failed putsch exposes deep flaws in Putin's regime (FT)

- Will the Wagner insurrection affect the Ukraine war? (FT)

- The Putin system is crumbling (FT)

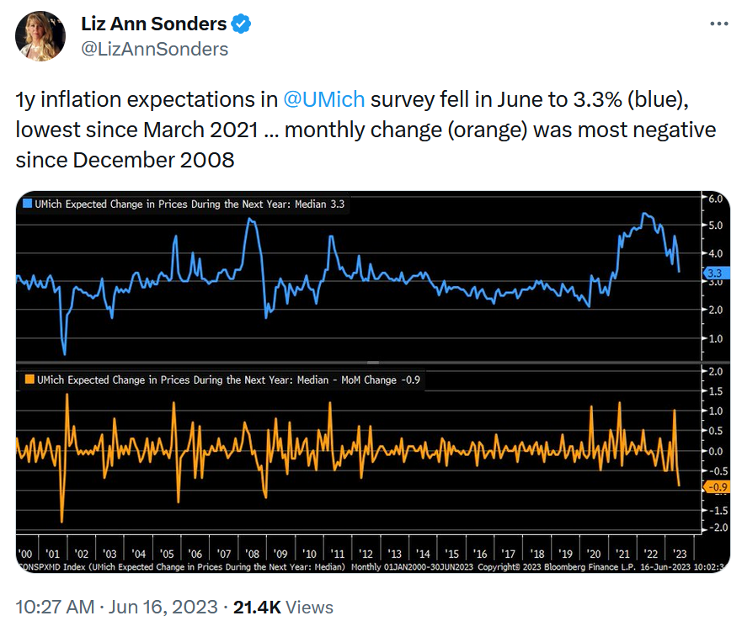

2) Another reason I'm bullish: Not only is inflation falling fast, but inflation expectations are as well, as this tweet by Liz Ann Sonders, the Chief Investment Strategist at Charles Schwab (SCHW), shows:

3) Sonders also tweeted out another interesting chart showing that the current market is not following the trajectory of the bear market from 2000 to 2002:

4) Andy Serwer with a bullish column in Barron's this weekend: There Won't Be a Recession This Year. You Can Take That to the Bank. Excerpt:

Years or maybe just months from now, dismal scientists and their ilk will probably be coming up with "un-reasons" to explain the great "un-recession" of 2023.

Indulge my descent into ungrammatical double-negativism. What I'm doing, of course, is ridiculing the most widely predicted economic event in modern history – which seems pretty certain not to happen.

In fact, I'm just going to say it: There won't be a recession this year. Not with all the help-wanted signs plastered on storefronts, and friends telling me they can't find people to hire for their businesses. Not with some 2.5 million airline passengers a day filing through TSA checkpoints. Not with hotel room rates up over 10% from prepandemic levels for most major U.S. cities. Not with the market up 14% year to date.

Look out, Ma! Here comes a white swan! White, of course, being the color of most swans, which speaks to the fact that the economy most often grows, that stocks most often go up, and that ol' Warren Buffett is still right: Never bet against America. Optimism, it seems, is in such short supply these days that market commentator Zachary Karabell has produced a podcast about it called What Could Go Right? Sounds like an ideal summer tonic for the nattering nabob crowd...

The University of Michigan consumer sentiment survey is up 8% in June, "reaching its highest level in four months, reflecting greater optimism as inflation eased," according to the latest update.

Older people are spending briskly after getting the biggest boost in Social Security since 1981. Granted, overall spending by consumers is selective – restaurants, food, and travel, yes; cars and jewelry, not so much – but that suggests a prudent, Goldilocks mind-set, rather than bubble bingeing, which is a positive. (As for rich folks loading up at dollar stores, how do you think they got that way?)

But the most positive fact, certainly over the longer term, is the underrecognized $2 trillion of spending from Washington in three bills: the Infrastructure Investment and Jobs Act, the Creating Helpful Incentives to Produce Semiconductors and Science Act, and the Inflation Reduction Act.

Although Kevin Pollari, lead of Deloitte's Infrastructure & Capital Projects program for state and local governments, cautions that some of that money is incremental, he nevertheless is most sanguine about the spend. "The money is huge in its impact on industry and the momentum it has created," Pollari says. "It has catalyzed so much activity that it's really kind of mind-boggling. As I go around meeting with metropolitan planning organizations, the amount of projects is really, really stunning."

5) I hate these junk fees with a passion, so it's discouraging to learn that there's a reason they're proliferating: they work!

That's why the government needs to step in and mandate transparent pricing because otherwise no company can afford to do it alone – they'll lose too much business. Who's to Blame for All Those Hidden Fees? We Are. Excerpt:

In 2013, the website StubHub, which resells event tickets, attempted to do away with hidden fees, citing research about how hated they are. Its new "all-in pricing" prominently displayed the total ticket cost from the beginning of searches. The strategy failed to boost business or attract more customers.

In 2015, shortly before abandoning all-in prices, StubHub did an experiment – described several years later by economists who obtained the data – where half of shoppers saw all-in pricing, and half saw the lower base price with taxes and fees only added at the end. The latter strategy boosted revenue 20%.

Shoppers didn't just buy more tickets. When they saw lower prices initially, they opted for better seats. By the end of the checkout process, they were committed.

"When people get to the end of the process, there's a variety of psychological reasons they're locked in," said Morwitz. "They overestimate the cost of starting over, they underestimate the benefits." Maybe they're just excited about the purchase, or reluctant to admit they could have made a mistake, she said.

On Thursday, two of the biggest U.S. ticket sellers, Ticketmaster and SeatGeek announced a switch to more transparent pricing. Some companies in the ticketing industry have said they would support all-in prices if they were mandated for everyone. The StubHub example shows why it's hard for one company to buck an industrywide practice.

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.