In defense of SPACs; Stunning Confessions of a Short Seller; Wirecard: a record of deception, disarray, and mismanagement; Runaway house prices; We went to The Late Show With Stephen Colbert

1) Special purpose acquisition companies ("SPACs") have been getting hammered recently, but I don't think they're going away – nor should they.

Professor Steven Davidoff Solomon from the School of Law at the University of California, Berkeley agrees, as he writes in this New York Times column: In defense of SPACs. Excerpt:

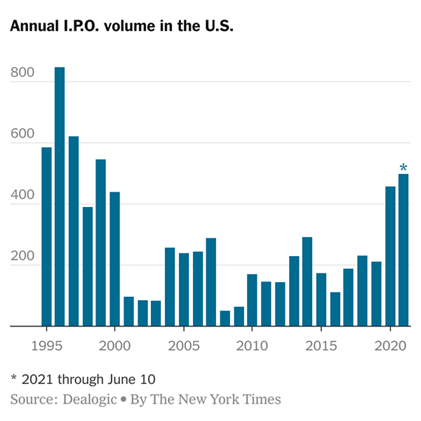

After the dot-com bubble burst and the Sarbanes-Oxley Act ushered in reforms to reduce broker conflicts, the small IPO all but disappeared, the subject of a study of mine. Since then, there has been a much slower pace of IPOs, almost all bigger companies.

Eventually, the notion that regulation had become too strict gained prominence, which led to the JOBS Act of 2012. This made it easier to go public, but the goal of giving public investors earlier access to innovative start-ups has proved elusive.

Enter SPACs, which are bringing many smaller companies to market. SPACs have found a way to raise ready capital via an IPO, long before approaching a company to acquire and transferring the funds. And there is also often additional investment from outside investors at the time of merger, which helps validate the deals...

More disclosure should be required about the compensation that SPAC sponsors receive. And some SPACs are too aggressive or make companies public too soon or with faulty (or even fraudulent) business plans. But the same can happen with traditional IPOs. That is not a reason to kill the only thing that has revived the market for IPOs of small and emerging growth companies in 20 years.

The sell-off in the SPAC sector is creating some great bargains such as Pershing Square Tontine Holdings (PSTH), which sold off earlier this month after it announced a complicated transaction that included purchasing 10% of Universal Music Group. My colleague Enrique Abeyta published an in-depth, extraordinarily insightful report analyzing it entitled, "The Type of Investor That Can Change Your Investing Life," which I covered in my June 7 e-mail.

If you're investing in the SPAC sector, it's critical to have an experienced guide like Enrique. Be sure to check out his Empire SPAC Investor newsletter – you can learn more about it right here.

2) This is the first time I've ever seen this. You gotta be extra careful on the short side! Stunning Confessions of a Short Seller. Excerpt:

The proliferation of short activist research in recent years has raised red flags about some of the originality, accuracy, and depth of these works – especially when combined with put options that are timed to coincide with the publication of reports that might send the stocks into a tailspin.

Now one of those activists, David Quinton Matthews, who wrote under the pseudonym Rota Fortunae, has admitted making false statements and profiting from short-dated put options ahead of his report's publication. David Quinton Matthews' admissions were made as part of a settlement of a defamation lawsuit that was billed as a "short and distort" case brought in federal court by the subject of the report – Farmland Partners, a Colorado real estate investment trust.

"I regret any harm the articles and its inaccuracies caused to Farmland Partners and any negative impact on Farmland Partners' stock price at the time," Matthews, a Dallas-based registered investment advisor, wrote in a carefully worded "press release" blogpost released on Seeking Alpha late Sunday night.

Fending off lawsuits is a cost of doing business for activist short sellers, who typically win those battles. But Matthews' stunning confession in this case sets it apart and sheds light on the relationship between anonymous short research firms and their hedge fund clients in an era when short selling has become less profitable and the costs of litigation are staggering.

3) Far more often, short sellers do excellent work exposing promotions and/or outright frauds like bankrupt German payment processor Wirecard. Here's the Financial Times with another follow-up story about it: Wirecard: a record of deception, disarray, and mismanagement. Excerpt:

The Financial Times has reviewed e-mails, internal chats, minutes of supervisory board meetings, and other documents, as well as hundreds of hours of witness hearings by Germany's parliamentary inquiry commission into the scandal.

The picture they paint is striking. In the aftermath of Wirecard's collapse, it quickly became clear that the company's top echelon had spent years deceiving investors, regulators, auditors and large parts of its own staff. But what the internal communications also show is that the confused and disorderly scenes of its last few weeks were anything but an isolated incident.

The documents and testimony reveal a company shaped by persistent mismanagement. Wirecard had presented itself as one of Germany's rare technological success stories; but on the inside, it was a chaotic, byzantine, and often ineffective organization.

In one of the most striking examples of the weakness of Wirecard's business, many of the operations that actually existed had been lossmaking for years, and some were heavily cash-burning.

Even Alexander von Knoop, the company's chief financial officer, was not fully aware of the extent of the losses. In one instance, he was outraged when he learnt in July 2019 – some 18 months after his appointment – that Wirecard's relationship with Aldi, the supermarket chain it had boasted about being one of its clients, had generated close to €5m in losses over the previous three years.

"With all due respect for flagship clients, what is the plan to become profitable with Aldi in future?" he asked his underlings by e-mail. He never received a convincing answer.

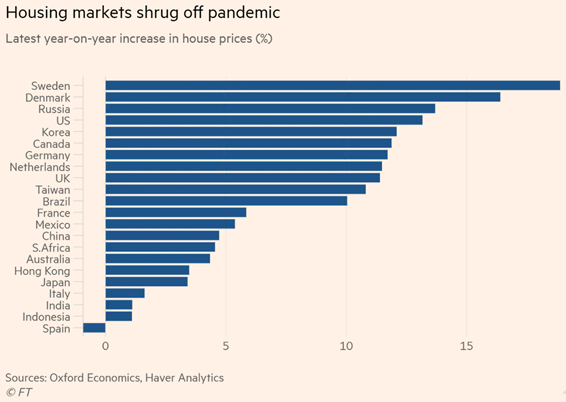

4) Here's the FT with another interesting article: Runaway house prices: the 'winners and losers' from the pandemic. This phenomenon, which is exacerbating income inequality, is happening not just in the U.S., but also around the world. Excerpt:

In Akron, Ohio, house prices have risen by 10.1% over the past year. In Albany, New York, the increase has been 11.7%. Albuquerque, New Mexico, has seen a similar surge of 11.6%.

And that is just the American cities beginning with an A.

"You could throw a dart at a map and it wouldn't matter where it landed because the housing market there is probably hot," says Ali Wolf, chief economist at Zonda, a housing market research company in California.

When the coronavirus pandemic first hit last year, the initial assumption of many politicians was that the economic pain would be shared. This epic event was to be a great leveler. But as governments across the developed world stepped in to protect incomes in ways that have most helped people with steady jobs, the hardship has fallen disproportionately on flexible, low income workers and young people. Suddenly unable to eat out or travel, richer households have used the last year to build up their savings.

Oslofjord, Norway, where the central bank said last week that Oslo had seen a net outflow of residents for the first time in 20 years in 2020.

Aggregate global wealth accumulated by households rose by about $28.7tn in 2020, according to a report published this week by Credit Suisse, which highlighted the extraordinary disconnect between this growth and the fortunes of the wider economy.

Wealthier households have channeled windfall savings into equities and cryptocurrencies, Louis Vuitton handbags, and Dutch masters. But most of all, they have poured money into buying bigger and better houses.

"People didn't expect this to play out how it did. No one clocked until a few months in that there are clear winners and losers," says James Pomeroy, an economist at HSBC. Now, the sharp rise in house prices represents "a huge challenge – a problem in terms of financial stability but a huge socio-economic problem too."

The phenomenon is global. Some of the sharpest rises have been in the U.S., where data released this week showed the median price for all housing types was up 23.6% year on year in May. Most U.S. homes now sell above asking price, with an offer accepted in a fraction of the time from listing than it took before the pandemic, according to Daryl Fairweather, chief economist at Redfin (RDFN), an online property brokerage.

But even in Japan and Italy, where ageing populations limit demand, price growth has accelerated. With ultra loose monetary policy holding down borrowing costs, house price inflation now stands in double digits in many developed economies, from Sweden to South Korea, Canada to the Netherlands and New Zealand – with the biggest increases seen not in capitals, but in suburbs, smaller cities, and rural areas.

5) Susan and I won the lottery for free tickets to be in the live studio audience for yesterday's taping of The Late Show With Stephen Colbert (you can enter the lottery for a future show here). It was great fun! Here are two pictures (they didn't allow anyone to take out their cellphones in the theater, so I had to sneak the second one):

Best regards,

Whitney