Jehoshaphat Research Comes Out of the Shadows; Kerrisdale short report on Tilray; A blast from the past with voxeljet

1) I continue to believe that activist short sellers – those who are willing to go public with their research and conclusions – are healthy for our markets.

Even if you only invest on the long side (which is what I recommend for 99% of people), you should read short sellers' reports on any stocks you own or are thinking of buying, as they might save you from big losses...

Some activist short sellers choose to remain anonymous, which makes sense for a lot of reasons. However, it's even better for our markets when they're willing to go on the record... so it's great news that one of the short sellers with the best track records over the past decade has unveiled himself in this article: Jehoshaphat Research Comes Out of the Shadows. Excerpt:

So just who is this enigmatic character using a biblical pseudonym? At first glance, it would appear that Jehoshaphat is something of a newbie in the world of short-selling. Jehoshaphat has published short activist research only since 2021, with an average track record of 15.8% gains for the stocks of 12 different companies, according to Breakout Point, which tracks activist short-sellers. (The stocks fell by that amount since the reports were published, while the broader market gained about 14%.)

But the person behind Jehoshaphat is no newcomer. A graduate of the Wharton School at the University of Pennsylvania, he has a 15-year record of short-selling at several firms, including hedge funds Diamondback Capital, Lawton Park Capital Management, and Carlson Capital, and then AllianceBernstein. He left AllianceBernstein's New York City offices during the early days of the Covid pandemic to work remotely from his hometown of Tampa, Florida. In 2021, he departed from the firm to form his own hedge fund, Carrollwood Capital Management, named after the neighborhood where he grew up.

His name is Victor Bonilla.

Bonilla, 40, reached out to Institutional Investor recently, saying he was ready to shed his anonymity. (Jehoshaphat, the name of an Israeli king in the Old Testament, was something of a joke between him and his wife; it's what they called their son before he was born in early 2020.) Bonilla now wants people to know that he is not "some really pissed off guy in a basement or some guy on Twitter who's just really mad and wants to take revenge on companies."

The move is a big change for a person who came from the hedge fund world, where, he says, "you don't go out and talk."

For many years, Bonilla had posted his short research on a site called SumZero. Over seven years, he says, he published 12 short ideas there, and all but one of the stocks significantly underperformed the market. The average alpha per idea was more than 30%, leading Bonilla to be ranked the site's No. 1 all-time short-seller in May 2016.

2) My friend Sahm Adrangi of Kerrisdale Capital, another one of the top activist short sellers, released a short report on Canadian cannabis company Tilray Brands (TLRY) last week. Excerpt:

We are short shares of Tilray Brands, a $2.4bn failing Canadian cannabis player running a familiar playbook for unsuccessful businesses trading in the public markets: given structurally unprofitable operations, the company has resorted to ongoing, shameless, and massive dilution to stay alive, even as management compensates itself generously while operating metrics further deteriorate.

Tilray touts itself as being different from other Canadian cannabis companies which lack positive EBITDA and free cash flow. But the truth is that Tilray is just obscuring losses by issuing shares, instead of recording cash expenses, to one of its largest suppliers. Furthermore, the company's "cannabis adjacent" diversification strategy essentially entails incinerating shareholder capital by overpaying for doomed businesses that will ultimately only deepen the company's losses.

Valuation made little sense even before retail investors raced to chase recent buzzy headlines on potential marijuana rescheduling, which may be a boon for U.S. weed companies but does next to nothing for Tilray. Now shares are even more poorly positioned ahead of seemingly endless dilution required to fund operations and refinance convertible debt due to mature in a few weeks.

Tilray is caught in a nonstop dilution cycle. It doesn't generate cash internally, and what cash it has on the balance sheet is largely thanks to dilutive equity offerings. To fund operations and maintain a currency for acquisitions, Tilray must keep its share price from joining the penny stock ranks of many of its cannabis peers.

Consequently, in late 2021, as Canadian cannabis industry fundamentals continued to implode, rather than pay amounts owed to a key cannabis operating partner in cash Tilray opted to directly issue the supplier increasing amounts of stock. What began as $24m paid in cash in 2021 morphed into $100m in stock paid over the last two years, even as Tilray's stock price fell to new lows. We believe these payments are poorly disclosed and allow Tilray to materially inflate reported EBITDA and free cash flow. We believe shareholders are being intentionally misled; without these convoluted stock payments, last year Tilray's EBITDA would have been zero and its free cash flow would have been deeply negative (again).

This brings back memories...

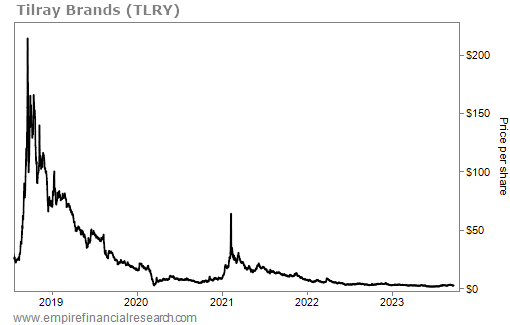

In perhaps my single best-timed call ever, I went on Yahoo Finance TV (you can watch the video here) on September 19, 2018 and, the very hour that Tilray peaked at $300 per share that day during intraday trading (it closed at $214.06 per share), I:

- Heaped scorn on this obvious bubble stock, saying it was overvalued by at least 10 times, maybe even 100 times (it was)

- Compared it to cryptocurrency, 3D printing, and alternative power stocks at their peaks

- Noted that short sellers can't correct this inefficiency because the cost of borrow and put options are so expensive

- Said it's a great cautionary tale for short sellers, as it appeared to be a great short at $50 a few weeks earlier – the lesson is to avoid hot stocks in hot sectors, with limited floats and a big short interest

- Predicted that, from its high that day of $300 per share, it would be below $100 per share within a month (it was) and would crash at least 90% within a year, probably sooner (it did)

- Lamented how many greedy, naïve, inexperienced individual investors were going to get incinerated

- Said the SEC should halt trading for a week so it could investigate possible market manipulation (it didn't)

A few months later in January 2019, with the stock still trading at nearly $100 per share, I had the chance to see management present at the ICR Conference in Orlando. During the Q&A after their presentation, I raised my hand and said:

Even though your stock is down a lot from its high, it's still wildly overvalued, so I recommend that you issue as much stock as possible to raise cash.

The CEO smiled and said, "That's exactly what we're doing." (And they were: the company sold $157 million of stock in the fiscal year ending in May 2018 and another $191 million the following year.)

It was a smart move for Tilray, but a disaster for investors foolish enough to have bought the stock, as it currently trades for less than $3 per share:

3) I gave similar advice years earlier to German 3D printing company voxeljet (VJET), which hit my radar screen today on this announcement: voxeljet AG Announces Review of Strategic Alternatives.

Some background: when I was at my first Consumer Electronics Show in January 2014, 3D printing companies were all the rage. To learn more about this emerging technology that had investors so excited, I visited the booths of dozens of companies and saw many Chinese competitors selling knock-off printers at a fraction of the price of the market leaders like 3D Systems (DDD) and Stratasys (SSYS), whose stocks had gone parabolic, up nearly 10-fold in the previous two years.

It was such an obvious bubble that I shorted all five publicly traded stocks in the sector and went very public with my thesis, which paid off spectacularly, as every stock dropped roughly 90% in less than two years (and have never recovered). Here are two articles that Julia La Roche wrote at the time about my thesis: Whitney Tilson Says 3D Printing Stock Is Going To Plunge 90% and Here's The Hilarious And Brutal Chart That Whitney Tilson Sent Out To Explain The Crash In A Big 3D Printing Company.

The smallest of the five stocks was voxeljet, which had gone public in late 2013 and had soared to a $3 billion market cap, despite barely detectable revenues of $16 million that year. This always happens in silly bubbles: insiders take second- and third-tier companies public in the hopes that they can cash out before the bubble inevitably bursts – good recent examples would be all the dodgy electric vehicle companies like Nikola (NKLA), Mullen Automotive (MULN), and Canoo (GOEV) that went public in 2020 and 2021 and have completely imploded.

The reason voxeljet sticks out in my mind is that it's the only company in which I met management. They were meeting with investors in New York, so I tagged along with a friend and listened to the presentation by three very formal German engineers about their high-end industrial 3D printers, which sold for $1 million each. After hearing them out, this is what I told them:

I came in here thinking your company was a total fraud. But I was wrong: you are impressive engineers and it's a credit to you for building an impressive machine.

But you need to recognize that your entire industry is in a massive bubble, which means your stock is inflated to at least 10 times what it's worth.

So I have two pieces of advice for you: first, as a company, sell as much stock as you can to raise cash... and, personally, you should do the same. If you are locked up and can't sell your shares, then hedge yourself by shorting the stocks of all of your competitors.

They nodded politely and I never thought of voxeljet again until today, so I was curious to look back and see what happened...

After raising $65 million in the IPO in 2013, the company took my (obvious) advice and issued more stock in 2014, raising another $37 million.

Nearly a decade later, revenues have doubled to $32 million, so there has been a little bit of a growth story.

But voxeljet has lost money every year since then ($17 million in the last 12 months) and the stock has gone from more than $300 per share to around $1 per share...

The lessons here are timeless: don't get sucked into bubbles, growth doesn't equal profits, and valuation matters.

4) Had you asked me before watching this video, Run ONE Lap At Kipchoge Pace And WIN £50 | WR Marathon Speed Challenge, whether I could run 400 meters – one lap of a track – at the pace Eliud Kipchoge maintained for his entire unofficial-record-setting 1:59:40 marathon (here's an article about it: The incredible science behind Eliud Kipchoge's 1:59 marathon), I would have said "sure!"

I have seen Kipchoge run by my apartment on Fifth Avenue during the NYC Marathon and he didn't seem to be running very fast (23 miles into the race).

And then I looked at my personal-best times...

Kipchoge ran a marathon, equal to 105 400s back-to-back, at a pace of 1:08 (68 seconds) each – and my personal best at that distance is 1:16 – not even close!

Well, how about the 200? On Friday, my workout with my Whitney-and-the-ladies running group ended with a downhill 200m all-out sprint. My time was 34 seconds – exactly Kipchoge's pace for an entire marathon. This blows my mind!

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.