My 1999 thesis on Amazon; Doug Kass' spot-on forecast; Money flows from active to passive; Pandemic Is a Great Incubator for Financial Fraud

1) I have a long history with Amazon (AMZN), dating back to when I bought the stock at $48 per share in my hedge fund in 1999.

With AMZN shares recently breaking $3,000, I went back through my archives to see what my thinking was back then and found this e-mail that I sent to my friend, journalist Herb Greenberg, on October 5 of that year. In response to his skepticism (which was well-founded, as the stock fell below $6 per share two years later), I wrote:

I heard Joe Galli's presentation at the BofA Securities conference in SF last week (he's the new President and COO of Amazon, formerly at Black & Decker). I was really impressed. Here are the highlights:

1) From a year ago, AMZN has moved from being solely a book seller to a) selling toys, music, videos, electronics, etc.; b) having auctions, including an investment in/partnership with Sotheby's; c) expanding to the U.K. and Germany; and d) taking stakes in many categories (Drugstore.com, pets.com, gear.com, homegrocer.com, and della & james). In short, in only one year, AMZN has made tremendous strides toward becoming a broad-based e-commerce company and positioning itself to go after the $5 trillion global retail market.

2) AMZN added 2.3 million new customers last quarter and 7 million in the past year to reach 11 million, by far the largest in e-commerce. eToys has had 500,000 total customers. AMZN's annual sales are 3.5x that of its main competitors as a group (B&N, Reel.com, eToys, and CDNow), and 8x that of its single largest competitor.

3) 70% of its revenues in Q2 came from existing customers.

4) AMZN is the 16th most trusted brand in America according to a survey, and the company is only four years old.

5) AMZN has made huge progress in building a world-class management team. In addition to Galli, it hired Warren Jenson from Delta as CFO and Jeff Wilke from Allied Signal to head operations.

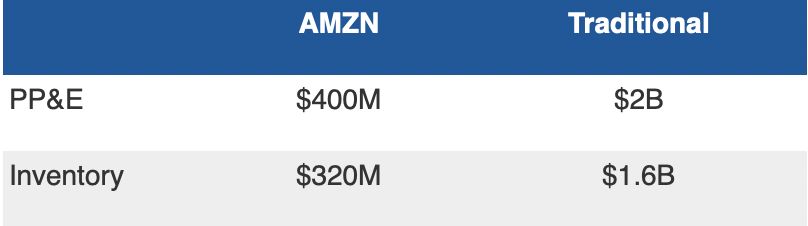

6) Galli rebutted the critics of AMZN's new warehouses by pointing out that a) AMZN has always controlled its own logistics, to ensure top-notch customer service; it's just adding to its two warehouses that were at capacity last Christmas (Nevada and Kansas are now operational and three more are on the way); and b) the warehouses don't change AMZN's superior economic model relative to bricks-and-mortar retailers. He gave the following statistics for AMZN vs. a typical bricks-and-mortar retailer doing $8 billion in sales:

By consuming a much lower amount of capital to support each dollar of sales, AMZN offers the potential (key word) for much higher returns on capital.

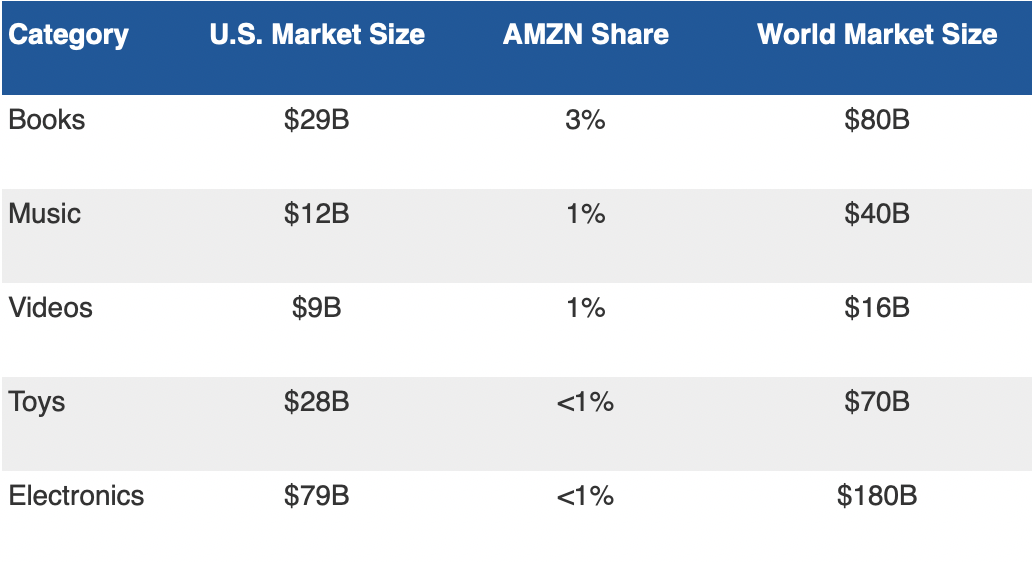

7) In the five categories where AMZN is active (and AMZN is quickly moving into new categories), there is room for huge growth in the U.S. and world markets:

Finally, here are my own thoughts on zShops: I've always felt that the greatest potential for Amazon is less as a retailer and more as a brand. The greatest businesses in the world (Coke, McDonald's, etc.) involve licensing a brand, whereby others put up the money and do all the work, and the licensor simply rakes in the money. I view zShops as the first of what I believe will be many steps by AMZN to leverage its brand and customer base far beyond simple retailing.

Regardless, this is going to be an entertaining ride, which I plan to stick out for the long run.

That's a pretty darn good analysis if I do say so myself – how I wish I'd listened to myself and held it for the long run!

2) Though I'm regretful about not holding Amazon over the past two decades, at least I didn't fall into the "I missed it" trap when I launched my first newsletter, Empire Investment Report, in April 2019...

At the time, I recommended a 7% to 8% Amazon position, which is up 67% since then (versus only 9% for the S&P 500 Index).

I've been regularly pounding the table on the stock ever since, as has my friend Doug Kass of Seabreeze Partners. In my January 31 e-mail, I shared his thesis behind his forecast that the stock would hit "$3,000 by 2021 and surpass $5,000 by 2025." Here's a summary of what he wrote then:

- Amazon, the "Supreme Disruptor," has established an insurmountable first-mover advantage and a deepening competitive moat

- Amazon's profit runway is lengthy and (as witnessed by last night's report) underestimated

- I previously saw the company about one year away from "hockey stock" earnings per share ("EPS") growth that I believed would far exceed consensus expectations

- Amazon is 12 months ahead of my schedule

- I continue to expect that AMZN, in the fullness of time, will become the first $2.5 trillion company

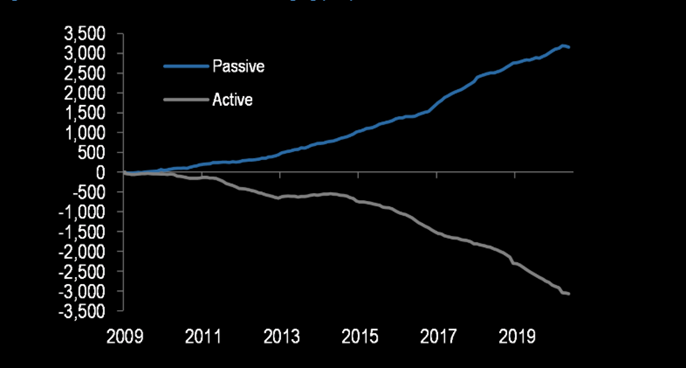

3) Following up on yesterday's e-mail about the difficulties long-short hedge-fund managers are having, this chart from The Market Ear shows that all active managers have been losing money, as assets flow to passive (index) funds:

4) Here's Bloomberg's Joe Nocera with some wise, cautionary words: Pandemic Is a Great Incubator for Financial Fraud. Excerpt:

"The pandemic is the perfect storm for fraud," one of the panelists said, and who can doubt it? The federal government hastily pushed hundreds of billions of dollars out the door in the largest bailout in U.S. history with only the most vague requirements for recipients; bankers working from home doled out those billions to small businesses; regulators loosened rules to help institutions get through the crisis. As my colleagues Timothy L. O'Brien and Nir Kaissar noted recently, "the White House has made it easier for government insiders to obtain bailout loans from the Small Business Administration, creating a raft of conflicts of interest."

That certainly sounds like a recipe for financial fraud...

As for the banks, the SBA has put them in a terrible spot, giving them the responsibility of hastily vetting the hundreds of thousands of businesses seeking PPP funds. Even with the best of intentions, it is inevitable that scam artists found ways to bilk the banks out of PPP loans. Indeed, prosecutors have already arrested a handful of executives for doing so.

The larger issue is that, just like in 2008, regulators aren't focused on preventing misconduct. Instead, their focus is on making sure banks have the ability to lend – even if it means loosening rules that were designed to make banks safer. In late March, for instance, the Federal Reserve relaxed several lending rules, including one that measured counterparty credit risk. And in early April it loosened capital requirements...

If significant bank misconduct is uncovered during a Covid-19 post-mortem, said Stephen Scott, the founder of Starling Trust Sciences, a risk-management company, "there will be pitchforks."

The country is much more polarized than it was in 2008, and much angrier, too. If it turns out that the billions of dollars intended to help out-of-work Americans was diverted by fraud, it will make the aftermath of the financial crisis look like a picnic.

Best regards,

Whitney