My out-of-consensus view on an early end to the Ukraine war; Energy producers have finally developed some common sense around capital allocation; Why a Secretive Short Seller Is Challenging Reports Made by Peers; The R.T.O. Whisperers Have a Plan; Biased maps

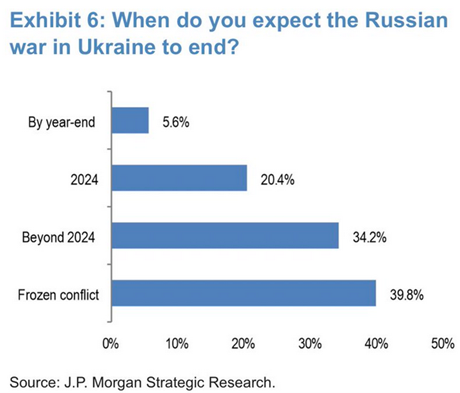

1) CNBC's Carl Quintanilla posted some interesting charts from JPMorgan Chase's (JPM) latest investor survey on the following questions:

- Where do you see the S&P 500 at year end?

- Where will 10-year U.S. Treasury yields end the year?

- When does the next U.S. recession start?

- What would induce you to add to risky assets?

- What is the probability of a China-Taiwan war in the next five years?

My answers to these questions were roughly in line with the consensus, with the exception of this one:

My view, based on extensive reading and visiting Ukraine twice in the past two months (at one point going within six miles of the front lines) is in the 5.6% minority.

I think that Ukraine has been getting stronger and Russia has been getting weaker every day for the past six months.

All winter, Ukrainian forces have cleverly tied up Russian ones in Bakhmut, a small, strategically insignificant city – decimating Russian forces with their "B" team (Territorial Defense Forces), while resting, training, and equipping their best troops for the counter-offensive that I believe will commence in the next two to four weeks. Watch this short video the Ukrainian government posted to see the forces it has been massing.

This isn't to say that expelling Russian forces from their territory will be easy... I expect at least a month of brutal, bloody fighting, with only small territorial gains, which will reinforce the views of those who believe this will be a long, drawn-out conflict, possibly ending in a stalemate.

But I believe that Ukrainian forces will not stop, no matter how high their losses, because the idea of having Russian forces on their soil another year is intolerable. As such, their continued attacks on depleted and demoralized Russian forces will result in a breakthrough and a chaotic Russian retreat to the border.

By mid-to-late summer, having expelled Russian forces from eastern Ukraine, Ukrainian forces will likely be on the border of Crimea.

At that point, I expect them to pause and there will be a peace deal that ends the war, with two bones being tossed to Russia...

- While Russia will withdraw its forces from Crimea and it will be returned to Ukraine, Ukrainian forces won't enter the territory. Instead, it will become some sort of UN protectorate.

- Ukraine won't officially become part of NATO, but it will instead receive security guarantees that are the equivalent.

If I'm right, I think the unexpected early end to the war will result in lower energy and food prices and provide a tailwind to the markets into the end of the year.

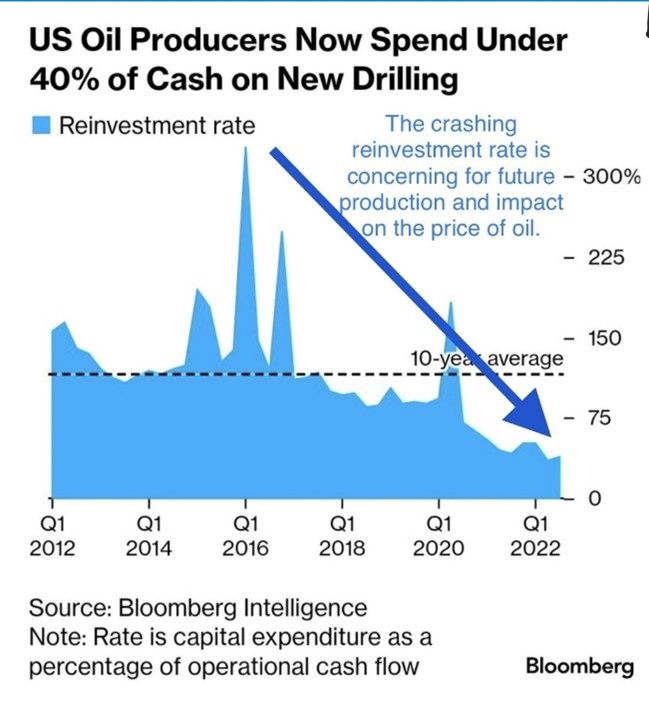

2) That said, we're still bullish on energy over the long term in large part because energy producers have finally developed some common sense around capital allocation.

The sector has historically been characterized by booms and busts because any time energy prices rose, producers plowed more than 100% of their profits into new production – causing oversupply and falling prices and profits.

But this time finally is different, as you can see from this chart from Bloomberg:

3) I think activist short sellers are, overall, healthy for our markets... but sometimes they get it wrong.

This is why in January and again in March I covered three reports by a new entity, Fiat Lux Partners, that rebutted reports by activist short sellers.

The folks behind Fiat Lux have chosen to remain anonymous, so kudos to Institutional Investor's Michelle Celarier for contacting them and writing this revealing article: Why a Secretive Short Seller Is Challenging Reports Made by Peers. Excerpt:

Cohodes is one of many short sellers who've complained – some of them privately – that the large number of often anonymous short activist reports has created an information overload that risks commoditizing the research and has also raised red flags about its originality, accuracy, and depth. Such activist short sellers "give someone like me a bad name. Their work is so shoddy and their work is so fly by night," Cohodes said.

As it turns out, Fiat Lux feels pretty much the same way, even though it has no connection to Cohodes. II has confirmed that Fiat Lux, which has now published three reports, is run by an employee of a well-regarded activist short selling fund whose founder supports its mission. The person behind Fiat Lux declined to say whether he had other financial backers.

In an interview with II, he said that there is "an extremely crowded space of short sellers" and while many are smart and thoughtful, "there are some who are consciously being exceptionally careless."

"They are very fast and loose in their research and frankly publishing reports which are of exceptionally low quality," he said. "We see a lot of poor short sellers free riding on this massive credibility that high quality short sellers have built." He made a point of saying that he isn't targeting the individual short sellers, some of whom are occasionally "publishing bad material."

As Fiat Lux's founder pointed out, activist short selling is a "model to have people highly incentivized to sniff out bad actors." He has simply taken that model and turned it on its head, sniffing out what he considers bad reports.

4) I have sent this New York Times article to many of my friends – ranging from managing partners at big law firms to owners of small hedge funds – who are grappling with employees' resistance to returning to the office: The R.T.O. Whisperers Have a Plan. Excerpt:

But then there were employees, like Alefiya Hussain, a computer-science researcher, who realized how much time they gained from remote work. Hussain estimates that at one point, before the pandemic, she spent 400 minutes a week commuting from Palos Verdes to I.S.I. Once she started working from home, she could have longer meals with her children, exercise on Zoom with her sister and write more papers for the institute. "It lets me control and define my time," she says.

As Knoblock was wrestling with the fate of his office, a colleague sent him a video of a talk by Gleb Tsipursky, a behavioral scientist who promised to help chief executives in Knoblock's precise situation. Tsipursky, the 42-year-old head of the boutique consultancy Disaster Avoidance Experts, appeared in the video wearing a black headset and rimless rectangular glasses, his every blond hair in order. In his talk, Tsipursky acknowledged the tough spot that employers like I.S.I. were in, citing a statistic that 40% of workers say they would quit their jobs if forced to come in full time.

He told the cautionary tale of Apple, which he said had recently mishandled its return-to-office process and was now facing an employee uprising and several high-profile departures. But Tsipursky claimed that, with his guidance, it was possible to avoid Apple's predicament.

Knoblock reached out to Tsipursky and described to him what was happening at I.S.I. "You can't just snap your fingers and get people to change their behaviors," Tsipursky said. He told Knoblock that most business leaders were thinking about the problem of hybrid work all wrong. Tsipursky's philosophy is that hybrid work isn't a logistical dilemma; it's psychological.

Tsipursky's doctoral research was on the Soviet Union's policing of music in the 1940s and 1950s. The Kremlin didn't want Russian teenagers to be influenced by American artists like Miles Davis and Dizzy Gillespie. But the government found that the more heavy-handed its messaging on radio stations and at youth-group meetings, the more the youth flocked to forbidden artists. If you tell people what to do, they'll rebel, Tsipursky told I.S.I. Give them reasons to act a certain way, and they'll be more inclined to do so.

In other words, you shouldn't forcibly change people's schedules – but sometimes you can change their minds.

5) These 20 maps are really fascinating... I didn't realize how biased standard maps are. Here's an example:

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.