Pros and cons of my investor pitch deck; Tesla should raise money now; Musk's short fuse; Wilbur Ross’ Pattern Of Grifting; John Oliver on trade; Hedge Fund Backed by Industry Leaders Closes Its Doors

1. As part of our seminar on How to Launch and Build an Investment Fund, we teach an in-depth module on how to create a first-class, compelling investor pitch deck, using multiple real-world examples (as we do with everything we teach). The first example is my own deck, which I think was at best a B – decent but a lot of room for improvement, as I discussed in our webinar earlier this month – here's the video of it: https://player.vimeo.com/video/285653427 (8 min).

If you find what we're teaching interesting, please join us for our three webinars or in-person seminars next month:

Don't delay – the super early bird rate expires on Thursday!

2. In light of the total mess at Tesla (the latest bombshell is this WSJ piece, just posted: Some Tesla Suppliers Fret About Getting Paid), I will repeat what I wrote on March 20 in my article entitled An Open Letter To Reed Hastings: Do An Equity Offering Now:

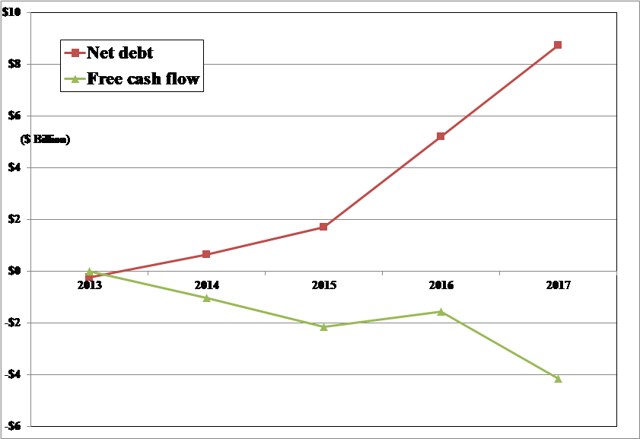

I would give the same advice, but even more emphatically, to Elon Musk right now. Like you, he is a bold visionary, investing heavily in the future, but piling up even more debt on Tesla's (TSLA) balance sheet to fund even deeper negative free cash flows, as this chart shows:

He too should be using his richly valued currency to avoid the risks outlined in this cover story in last week's Wall Street Journal, Tesla's Make-Or-Break Moment Is Fast Approaching.

3. Speaking of Musk, this article (in which I'm mentioned in passing) highlights how he is a case study in how NOT do handle short sellers: The private musings and short fuse of Elon Musk. Excerpt:

Short sellers have a way of rattling even the most confident business leaders. A classic of the genre is Overstock chief executive Patrick Byrne, whose crazed diatribes against investors betting on a stock-price drop include a public conference call during which he ranted about a shadowy "Sith Lord" out to destroy Overstock and his railing on a site called Deep Capture against unfair financial-media coverage. Overstock also sued his purported enemies.

On the other end of the spectrum is Netflix CEO Reed Hastings, who in 2010 wrote a polite-bordering-on-sweet open letter to short seller Whitney Tilson, calling him a "great investor and a wonderful human being" before laying out an even-toned and reasonable case that Tilson's evaluation was wrong.

As short pressure increases, CEOs have a tendency to inch rightward along the Hastings-Byrne Continuum, from polite objection to fevered denunciation. Tesla's Elon Musk isn't close to Byrne territory yet, but his recent Twitter stylings indicate that he is getting rattled by persistent investor skepticism about a money-burning, never-profitable enterprise with a market cap of about $60 billion.

PS – Note to my fellow short sellers: if you ever publish your short thesis (as I did here in Dec. 2010: Why We're Short Netflix) and the CEO responds with a thoughtful article that begins by calling you a "great investor and a wonderful human being", COVER YOUR SHORT!!! (Which we did and, after the stock fell ~80%, then went long VERY profitably – it's up more than 50x from the bottom!)

4. I thought Wilbur Ross was one of the good (or at least less dreadful) guys in this administration... until I read this devastating article: New Details About Wilbur Ross' Business Point To Pattern Of Grifting. Excerpt:

It is difficult to imagine the possibility that a man like Ross, who Forbes estimates is worth some $700 million, might steal a few million from one of his business partners. Unless you have heard enough stories about Ross. Two former WL Ross colleagues remember the commerce secretary taking handfuls of Sweet'N Low packets from a nearby restaurant, so he didn't have to go out and buy some for himself. One says workers at his house in the Hamptons used to call the office, claiming Ross had not paid them for their work. Another two people said Ross once pledged $1 million to a charity, then never paid. A commerce official called the tales "petty nonsense," and added that Ross does not put sweetener in his coffee.

There are bigger allegations. Over several months, in speaking with 21 people who know Ross, Forbes uncovered a pattern: Many of those who worked directly with him claim that Ross wrongly siphoned or outright stole a few million here and a few million there, huge amounts for most but not necessarily for the commerce secretary. At least if you consider them individually. But all told, these allegations—which sparked lawsuits, reimbursements and an SEC fine—come to more than $120 million. If even half of the accusations are legitimate, the current United States secretary of commerce could rank among the biggest grifters in American history.

5. One of the biggest risks to stocks is the possibility of a major trade war. I would feel more sanguine about this is there were anyone with an ounce of knowledge and/or common sense on this topic in this administration, as John Oliver highlights in this in-depth piece: https://youtu.be/etkd57lPfPU. Jared Kushner found Trump's primary trade advisor on AMAZON!?

6. Tough times in the hedge fund world! Hedge Fund Backed by Industry Leaders Closes Its Doors. Full article:

A hedge fund backed by some of the industry's biggest names, Cerrano Capital LLC, is closing less than a year after it got off the ground, the latest sign of the difficulties new funds are having raising money.

Michael Weinberger's $230 million hedge fund was launched last year, hoping to raise as much as $1 billion. The fund's early investors included York Capital Management founder James Dinan and chief investment officer Daniel Schwartz. Billionaire hedge-fund investor Dan Loeb of Third Point LLC was among the investors in Cerrano, according to people close to the matter.

Mr. Weinberger previously oversaw billions of capital as head of equities at York. Cerrano focuses on making both bullish and bearish bets on stocks.

Cerrano lost 1.4% through June of this year, after being up over 5% last year. In the 11 months the firm existed, the fund was up slightly. Mr. Weinberger became frustrated with the time he needed to devote to market the fund, the people say, and decided to return capital and manage his own money.

The decision underscores the difficulties many hedge funds are having making money and raising capital, as investors rethink the value of such funds.

Hedge funds have generally performed worse than broader stock market indexes for much of the past several years, making it hard for them to justify high fees. More recently, a widely followed hedge-fund index maintained by data research company HFR declined by 0.46% in June, pulling down the industry's gains for the first half of 2018. The index rose 0.81% in the first two quarters, which is lower than the 2.65% return on the S&P 500, including dividends, over the same period.