S&P 500 returns after a 5%-plus gain in Q1; Doug Kass' bearish views; Berkshire meeting two weeks from tomorrow; Yet Another Value Blog calls for immediate change at Berkshire

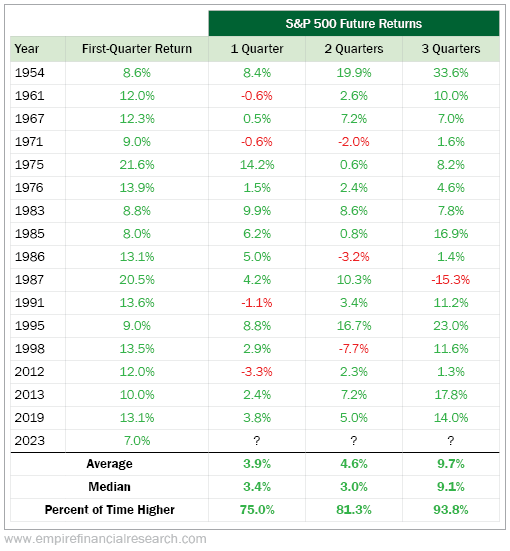

1) My colleague Enrique Abeyta included this table in the latest issue of Empire Elite Trader, which I found fascinating – I never would have guessed, and yet another reason to be bullish:

We had a good first quarter of performance in the market, with the S&P 500 Index up 7%.

In the table below, you can see how the market performed through the rest of the year after a first-quarter S&P 500 gain of at least 5%...

This is an amazing track record... In every year but one in more than seven decades, the market has ended up higher at year end. (The one exception is 1987 with the infamous Black Monday market crash.)

Thanks, Enrique!

To learn more about Empire Elite Trader – including how to gain access to Enrique's brand-new trade recommendation, which just published Wednesday – click here.

2) My friend Doug Kass of Seabreeze Partners doesn't share Enrique's bullishness for reasons he details in his quarterly letter (farther below, at the end of this e-mail). Excerpt:

We continue to view the outlook for equities unfavorably – both in absolute terms and relative to bonds. While precision of forecast is not intended, we are of the belief that the S&P Index (at 4,105) is now trading at the upper end of the expected 2023 trading range (3,700-4,100) – providing little upside reward but an abundance of downside risk.

In light of our continued ursine view, Seabreeze has consistently employed a lower risk strategy than most – by maintaining a high gross exposure but a low net exposure.

For all of 2022, for the month of March and for the first quarter of 2023, we achieved good investment returns without taking on much market risk in a regime of heighted volatility and growing uncertainties.

At the end of March, Seabreeze Capital Partners LP net exposure was under 5% net long. Since month-end we have moved into a net short of exposure.

We currently have 26 longs and 28 shorts.

While stocks staged a strong comeback this year, the advance has been narrow-led by Apple (AAPL) (29x price earnings multiple), Nvidia (NVDA) (160x), Microsoft (MSFT) (32x), Meta (META) (25x), Tesla (TSLA) (59x) Amazon (AMZN) (N.A.), Alphabet (GOOGL) (24x), Salesforce (CRM) (900x), and Advanced Micro Devices (AMD) (110x) accounting for over 90% of the year's gains. This means that the rest of the market foundered as one would expect with interest rates rising, banks falling and the economy slowing...

To us, current valuations are not consistent with a 5% percent benchmark interest rate. They may even be too high for the ZIRP/QE world that many investors still believe in but no longer exists:

* The equity market's capitalization as a percent of nominal GDP is at the 2000 bubble peak.

* On a price to sales basis we are also at that 2000 peak.

* The S&P earnings yield (the inverse of the price/earnings ratio) sits not far from the risk-free rate of return.

* At 18.5x, the S&P price earnings ratio is in the 90th percentile in the last four decades.

When properly navigated (by not losing money!), a bear market sows the seeds for making money in the eventual bull market. As Sir John Templeton once observed:

For those properly prepared, the bear market is not only a calamity but an opportunity.

However, for now, our market concerns are multiplying as equity prices and Treasury bill yields rise.

3) The Berkshire Hathaway (BRK-B) annual meeting (aka, the Warren and Charlie Show), which I'll be attending for the 26th consecutive year, is taking place two weeks from tomorrow in Omaha, Nebraska. See my March 28 e-mail for more information about tickets, flights, lodging, car rentals.

I'll be hanging out at the bar on the main floor at the Hilton Omaha at 1001 Cass Street, directly across the street from the site of the meeting, the CHI Health Center, on Friday from 4 p.m. until at least 10 p.m. and on Saturday from 8 p.m. onward.

Warren and Charlie aren't getting any younger and it's not too late to make your plans to come. If you so, please stop by and say hi!

4) Speaking of Berkshire, Andrew Walker of Rangeley Capital wrote a hilarious and clever post on his blog (including the deliberate misspelling of "Buffet"): Yet Another Value Blog calls for immediate change at Berkshire. Excerpt:

It's time for a change.

That's all I could think about when reading Berkshire's most recent annual letter.

It's rare to see a corporate CEO admit to a single mistake in public. That's why I was so surprised to see Berkshire's Chairman / CEO (Warren Buffet) admit to the "many mistakes" he's made over the years. If he's willing to admit to "many mistakes" when most CEOs would not admit to a single one, imagine how many more mistakes Mr. Buffet must be hiding from us.

Perhaps making "many mistakes" would be acceptable if Mr. Buffet had founded Berkshire. We expect founder led companies like WeWork or Theranos to experience a stumble or two along the way... but those stumbles are part of the gig when it comes to founder led companies and their inevitable rise to greatness as they attack and inevitably dominant multi-trillion dollar TAMs.

In contrast, Mr. Buffet is not Berkshire's founder. He's just some pencil pusher who used his large bank account to take over the company years after it had been founded. Surely this corporate raider cannot take over a company and expect to lead it through stumbles and missteps that way a visionary founder could. We as shareholders expect... nay, demand, better from our managers, and when they continually stumble it's time for them to be replaced.

With that in mind, Yet Another Value Blog is not so humbly leading an activist campaign to replace Mr. Buffet.

We (and by we, as a one man blogging shop I do of course mean I) do not take this move lightly. However, given the litany of mistakes listed in the annual report and Mr. Buffet's refusal to engage with us, we have no choice but to make our demands public. Let's dive into the many mistakes Mr. Buffet has made, including both the ones he listed and the ones he omitted.

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.

My Market Outlook

Doug Kass, April 18, 2023

We continue to view the outlook for equities unfavorably – both in absolute terms and relative to bonds. While precision of forecast is not intended, we are of the belief that the S&P Index (at 4,105) is now trading at the upper end of the expected 2023 trading range (3,700-4,100) – providing little upside reward but an abundance of downside risk.

In light of our continued ursine view, Seabreeze has consistently employed a lower risk strategy than most – by maintaining a high gross exposure but a low net exposure.

For all of 2022, for the month of March and for the first quarter of 2023, we achieved good investment returns without taking on much market risk in a regime of heighted volatility and growing uncertainties.

At the end of March, Seabreeze Capital Partners LP net exposure was under 5% net long. Since month-end we have moved into a net short of exposure.

We currently have 26 longs and 28 shorts.

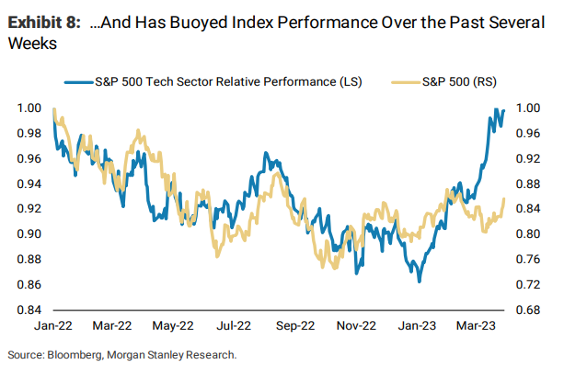

While stocks staged a strong comeback this year, the advance has been narrow-led by Apple (AAPL) (29x price earnings multiple), Nvidia (NVDA) (160x), Microsoft (MSFT) (32x), Meta (META) (25x), Tesla (TSLA) (59x) Amazon (AMZN) (N.A.), Alphabet (GOOGL) (24x), Salesforce (CRM) (900x), and Advanced Micro Devices (AMD) (110x) accounting for over 90% of the year's gains. This means that the rest of the market foundered as one would expect with interest rates rising, banks falling and the economy slowing.

The outsized contribution of tech stocks to overall S&P Index performance is exhibited here:

As my dear friend Bob Farrell has written:

Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

To us, current valuations are not consistent with a 5% percent benchmark interest rate. They may even be too high for the ZIRP/QE world that many investors still believe in but no longer exists:

* The equity market's capitalization as a percent of nominal GDP is at the 2000 bubble peak.

* On a price to sales basis we are also at that 2000 peak.

* The S&P earnings yield (the inverse of the price/earnings ratio) sits not far from the risk-free rate of return.

* At 18.5x, the S&P price earnings ratio is in the 90th percentile in the last four decades.

When properly navigated (by not losing money!), a bear market sows the seeds for making money in the eventual bull market. As Sir John Templeton once observed:

For those properly prepared, the bear market is not only a calamity but an opportunity.

However, for now, our market concerns are multiplying as equity prices and Treasury bill yields rise.

*The Federal Reserve faces a trilemma – the challenge of simultaneously reducing inflation, minimizing the hit to economic growth and jobs, and maintaining the stability of the financial system.

*Short dated fixed income instruments provide an equity-like return that is risk free and less volatile than stocks.

Take a picture of the following Treasury yields (and save it) – a rare bird in sight:

U.S. Treasury Yields

- 3 month 5.09%

- 6 month 5.02%

- 12 month 4.84%

- 2 year 4.05%

- 5 year 3.55%

- 10 year 3.44%

- 30 year 3.63%

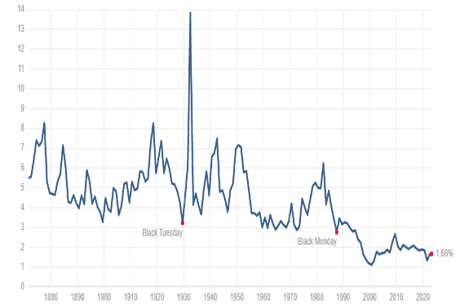

Recently, yields on both 3- and 6-month Treasury bills have climbed above 5% compared to the S&P dividend yield of only 1.65%:

S&P Dividend Yield

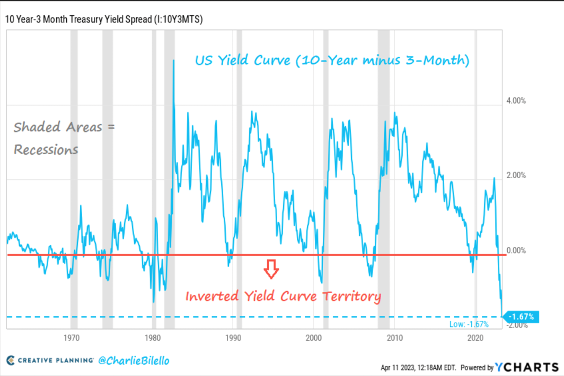

At 5.08%, the 3-month Treasury yield now 1.69% higher than the 10-Year Treasury yield (3.39%). This represents the most inverted yield curve in history – and is indicative that a recession likely lies ahead:

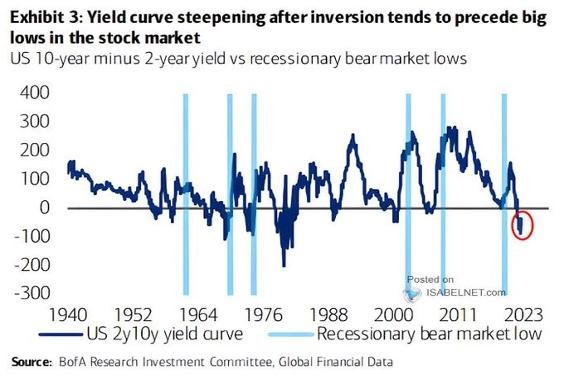

The same conclusion can be derived by observing the inversion of the 10-year Treasury note with the two-year Treasury note:

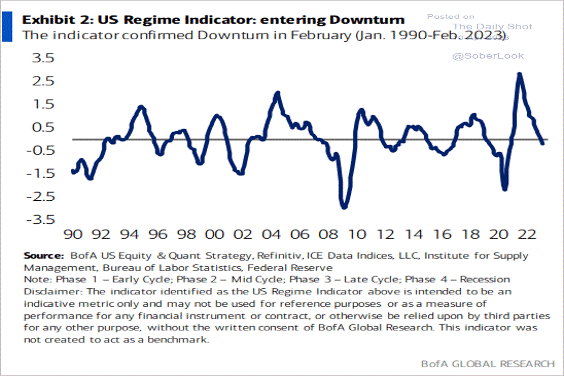

* Global economic, U.S. corporate profit, inflation and monetary/fiscal policy uncertainties abound. The domestic and global economies appear to be destined for recession as illustrated in the following charts:

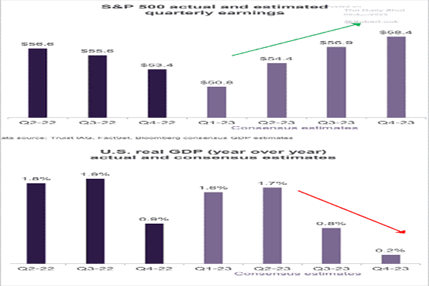

* The consensus somehow believes corporate profits will be healthy despite a significant economic slowdown. It's highly unusual for the economy to weaken but earnings accelerate:

* Inflation will likely remain sticky, representing a formidable challenge for the Federal Reserve. Though a drop in food and energy prices will contribute to a moderation in the CPI, wage inflation will remain elevated and Core Services Inflation (which excludes housing) will persist in the +4% to +5% range. This persistence of core services inflation argues strongly against any Federal Reserve rate cuts in 2023.

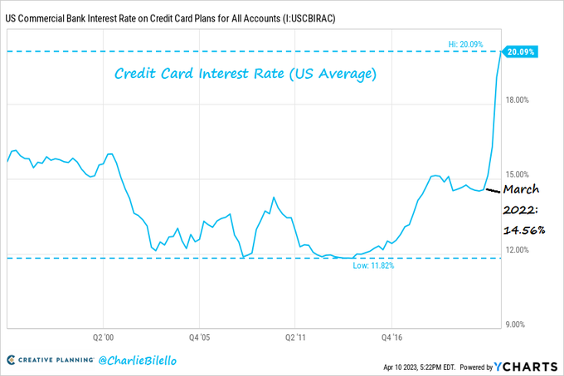

* The U.S. consumer appears particularly vulnerable to persistent inflation, elevated interest rates and reduced credit availability. The average interest rate on U.S. credit card balances has crossed above 20%. With data going back to 1994, that's the highest rate we've ever seen, and is 5.5% above the rate from just a year ago:

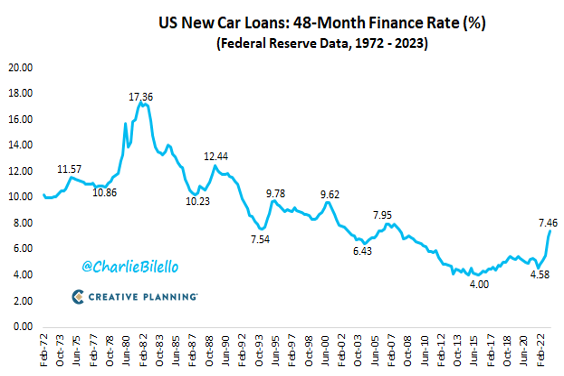

The average interest rate on 48-month new car loans has moved up to 7.46%. That's the highest we've seen since 2007. A year ago the rate was 4.87%:

The affordability of durables (automobiles and homes) has deteriorated. 16.8% of consumers who financed a new vehicle in Q1 2023 committed to a monthly payment of $1,000 or more – a new all-time high according to Edmunds – compared to 10.3% in Q1 2022 and 6.2% in Q1 2021:

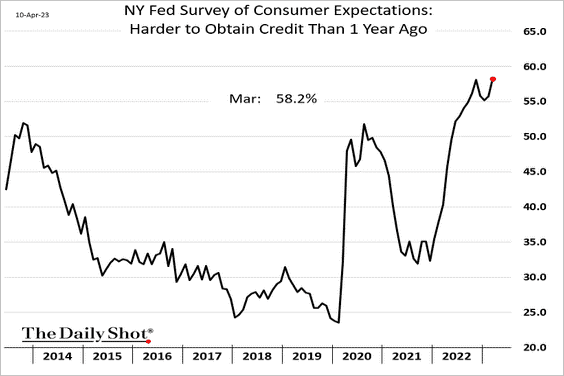

Finally, obtaining credit has become more difficult for U.S. consumers compared to a year ago:

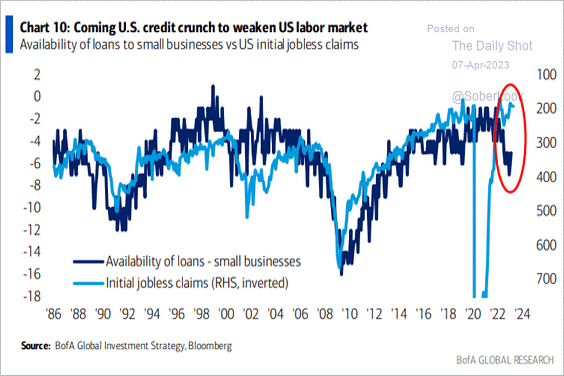

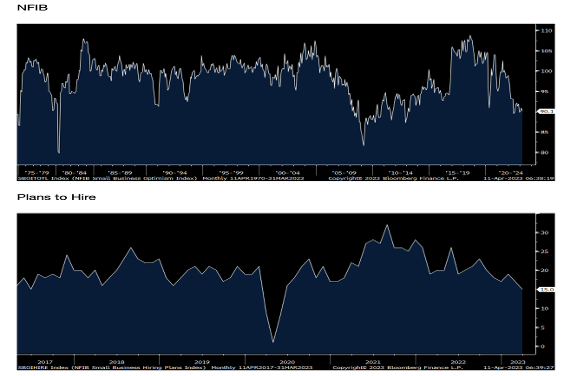

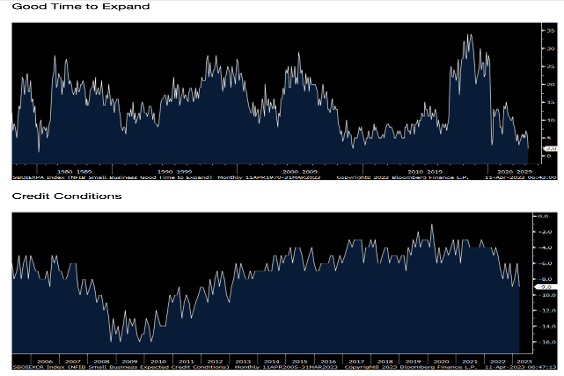

* We have always viewed the condition of small and medium sized businesses – who don't have the size or scale of larger corporations and rely on bank funding – as a leading economic indicator, often providing early warning signs of slowing domestic economic growth. Here a quote from today's NFIB release:

Small business owners are cynical about future economic conditions. Hiring plans fell to their lowest level since May 2020, but strong consumer spending has kept Main Street alive and supported strong labor demand.

Here are four confirming (NFIB) charts that support our business cycle concerns:

Source: Peter Boockvar