Today's inflation report; The Fed sucked its thumb; 10 charts; Warren Buffett CNBC interview this morning; BNSF Railway; Fyre Festival II

1) The Labor Department reported this morning that inflation eased to 5% in March, the ninth consecutive month of decline and the lowest level in nearly two years.

This is in line with what I've written previously that inflation should fall into the 4% range by midyear.

It will be interesting to see how the Fed reacts to rapidly slowing inflation, accompanied by a slowing economy, near-paralysis in the housing market – with both buyers and sellers on strike – and the turmoil in the banking sector resulting in a sharp tightening of credit (more on this below).

The Fed's remaining interest rate decisions for 2023 are scheduled for May 3, June 14, July 26, September 20, November 1, and December 13.

I think the Fed is finished raising rates, so won't change them at its May, June, and July meetings. Then, amid signs of a recession, it will cut rates by 0.25% twice in its last three meetings of the year.

If I'm right, I think this is good news for stocks in general – and bank stocks in particular.

2) Speaking of which...

As I continue to dig into the banking sector, I'm finding plenty of investment opportunities that I'll be sharing with Empire Investment Report subscribers next week (if you aren't already a subscriber, click here to become one and put yourself on the list to receive the issue the moment it publishes)...

As I've said several times previously, the situation today is nothing like it was back in 2008.

Yes, housing prices soared in the aftermath of the pandemic, but this was due to strong fundamentals: low mortgage rates, a shortage of new homes being built over an extended period, and lifestyle changes like working from home. There was no rampant speculation, fraud, or use of exotic structures like "option ARMs" in the mortgage market.

Banks aren't over-levered and don't have opaque off-balance-sheet entities that (rightly) freaked out investors in 2008. Nor are they facing the prospect of large losses in their loan portfolios (though there will likely be some in their commercial real estate books).

So why is there so much turmoil in the sector?

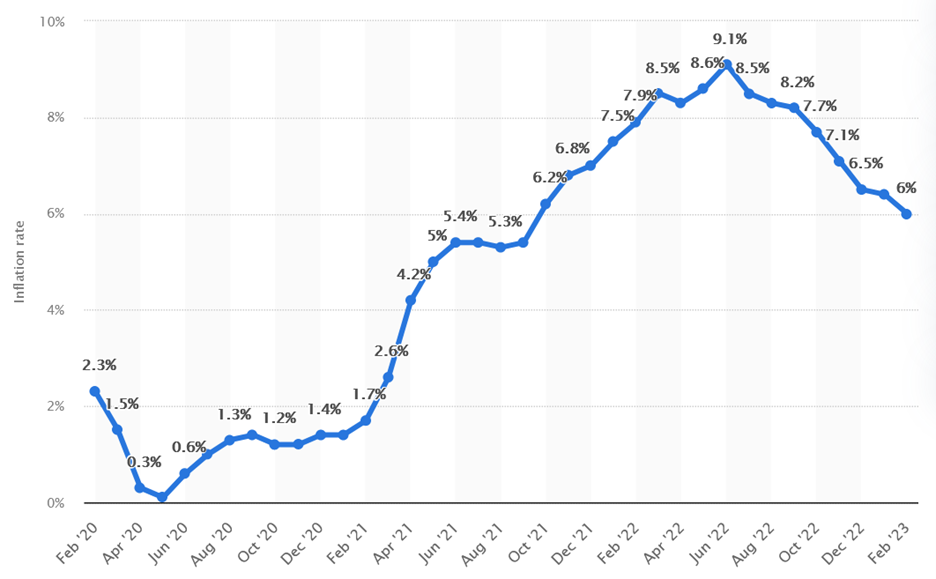

Well, the problems started when inflation started to rise as the economy recovered from the pandemic crash, going from a low of 0.1% in May 2020 to a peak of 9.1% in June 2022 (note that this chart doesn't show today's 5.0% print):

Looking at this chart, you might think that the Fed, with an inflation target of no more than 2%, would have started raising interest rates in early 2021 as inflation quickly spiked from 1.7% in February to 5.4% in June.

But instead, the Fed sucked its thumb for another nine months until March 2022, when inflation hit a 40-year high of 8.5%, before it started raising rates.

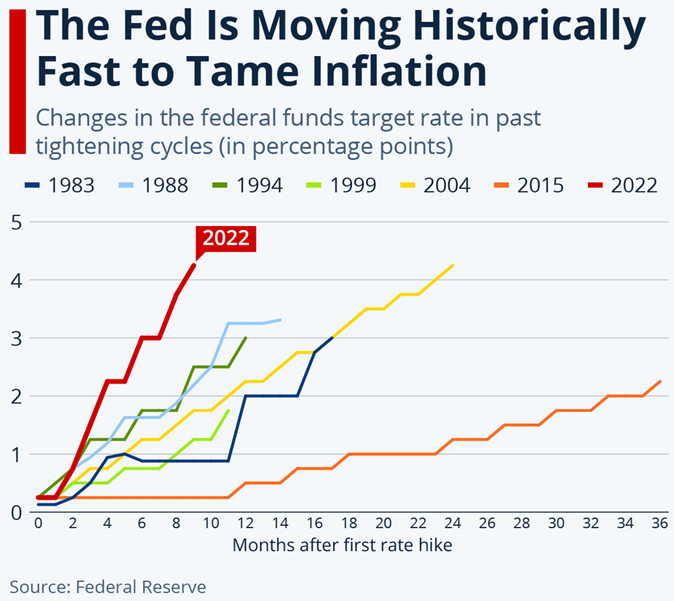

To make up for its initial inaction, the Fed has raised rates at an unprecedented clip (and this chart doesn't even capture the two additional 0.25% rate hikes this year!):

Such a rapid increase in interest rates has roiled the banking sector, for two main reasons...

First, banks take deposits and, very roughly speaking, make loans with 75% of them. Banks earn a spread between the interest rate they pay depositors and what they charge borrowers. A year ago, in an almost-zero interest rate environment in which banks were paying depositors nothing, they were happy to lend at, say, 4%.

Some of these loans had variable interest rates, which protect a bank when rates rise... but many didn't, which means that in today's environment, these loans are barely profitable – or even unprofitable.

Second, banks typically invest the remaining 25% of deposits in safe, liquid instruments like cash, bonds, and mortgage-backed securities. But a year ago, these were yielding almost nothing... so many banks invested in longer-dated securities – for example, a 10-year U.S. Treasury, which was yielding around 2% a year ago.

But with a 10-year Treasury now yielding nearly 3.5%, the value of one purchased a year ago at 2% has plunged – saddling the owner with a loss.

Fortunately for banks, accounting rules let them designate assets like this as "held to maturity," so they don't have to show a loss on their income statement or balance sheet, but investors – and, eventually, depositors – looked through the accounting to the underlying reality.

This triggered a run at a few banks like Silicon Valley Bank and Signature Bank, which both went under, and hit stocks across the sector – especially among small and mid-size banks, as depositors fled to the "big four" banks that are too big to fail: JPMorgan Chase (JPM), Citigroup (C), Bank of America (BAC), and Wells Fargo (WFC).

The chaos – some would call it a crisis – has created numerous mouth-watering investment opportunities which, again, I'll be sharing with Empire Investment Report subscribers next week – click here to become one.

3) CNBC's Carl Quintanilla tweeted 10 interesting charts from JPMorgan's Cembalest report, which show mixed signals about the health of the economy and our banks. Excerpt:

4) I'm a huge fan of Berkshire Hathaway (BRK-B) CEO Warren Buffett, so I watched with interest the extended interview he did this morning with CNBC. Here are various clips and articles CNBC has posted:

- Warren Buffett says we're not through with bank failures

- Buffett says U.S. bank deposits are safe and the government would backstop all of them if necessary

- Warren Buffett on U.S. economy: It's 'a tougher world' out there for many businesses

- Warren Buffett reacts to March inflation data: We don't profit from statistics and guessing

- Warren Buffett on raising stake in Japanese trading houses: I was 'confounded' by the opportunity

- Warren Buffett says Norfolk Southern handled train derailment 'terribly'

- Warren Buffett on ChatGPT and AI: This is extraordinary but not sure if it's beneficial yet

- Warren Buffett says he doesn't understand A.I. but he asked ChatGPT to write a song in Spanish

- Warren Buffett: I'd give up a year of my life to eat what I like

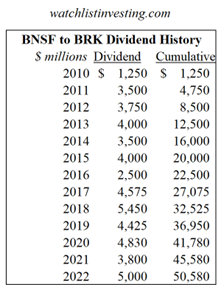

5) Speaking of Buffett, many critics said he overpaid for BNSF Railway when he acquired it in February 2010, shortly after the global financial crisis, in a $44 billion deal. As always, he has had the last laugh, as the railroad has paid Berkshire more than $50 billion and counting:

6) In 2019, I wrote a few times about con man Billy McFarland and his fraudulent Fyre Festival in the Bahamas, which led to two documentaries on Hulu (Fyre Fraud) and Netflix (FYRE: The Greatest Party That Never Happened).

McFarland pled guilty to two counts of wire fraud and was imprisoned from 2018 to 2022, but he's now out and – I hope you're sitting down – just tweeted this on Sunday:

I have three thoughts about this:

- You can not make this stuff up – this is the very definition of chutzpah!

- Anyone who pays McFarland anything deserves to lose their money.

- I think odds are close to zero that he'll be able to organize another Fyre Festival – but if he does, I know one place it won't be: the Bahamas, which considers him a "fugitive"!

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.