Two pitches for EPAM Systems; Investors spend $200mn on 'worthless' Bed Bath & Beyond shares; The Richcession Keeps Rolling; Pictures from Italy

1) We wrapped up the 19th annual Value Investing Seminar in Italy with a second day of eight outstanding presentations!

In my e-mails today and next week I'll share the best of them (including the rest of my presentation, which I started to cover in yesterday's e-mail).

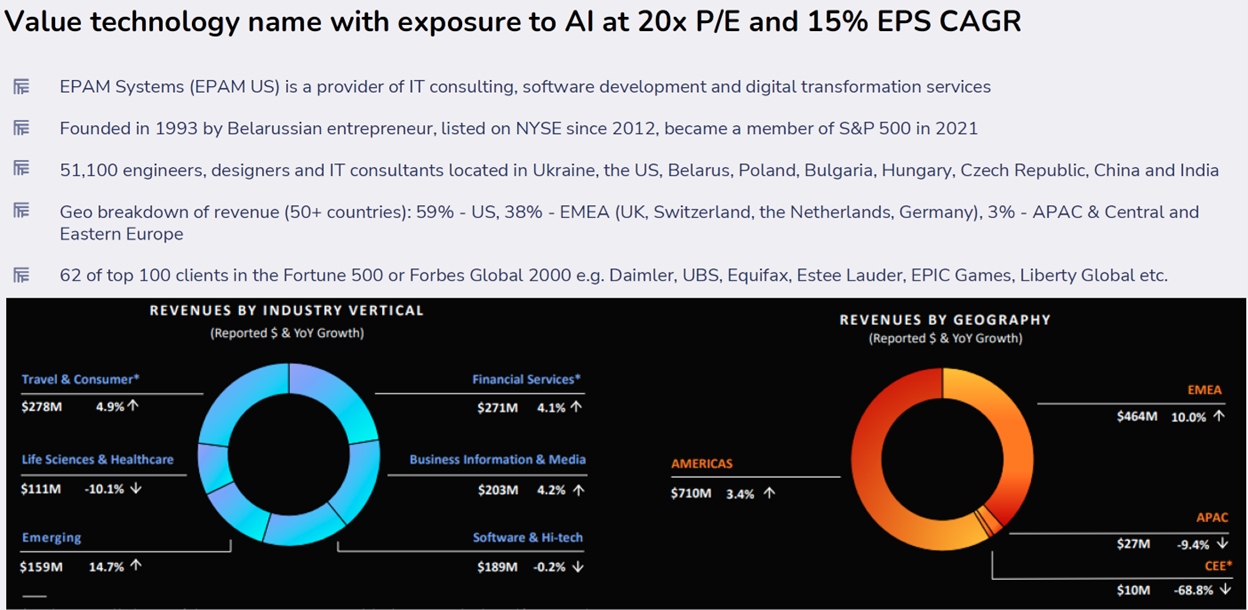

One of my favorites was a pitch for EPAM Systems (EPAM) by Anatoly Fedorov, the portfolio manager of the Signet Equity Fund, which is part of London's Signet Capital Management. He gave me permission to share his presentation, which you can download right here. Here are three slides from it:

2) EPAM was also pitched on ValueInvestorsClub on June 12, which members can access here (nonmembers will be able to access it after a 45-day delay, which will be July 27). Here's the introduction:

EPAM Systems is a high-quality IT service provider that had been a compounder stock. We believe that EPAM is an AI beneficiary.

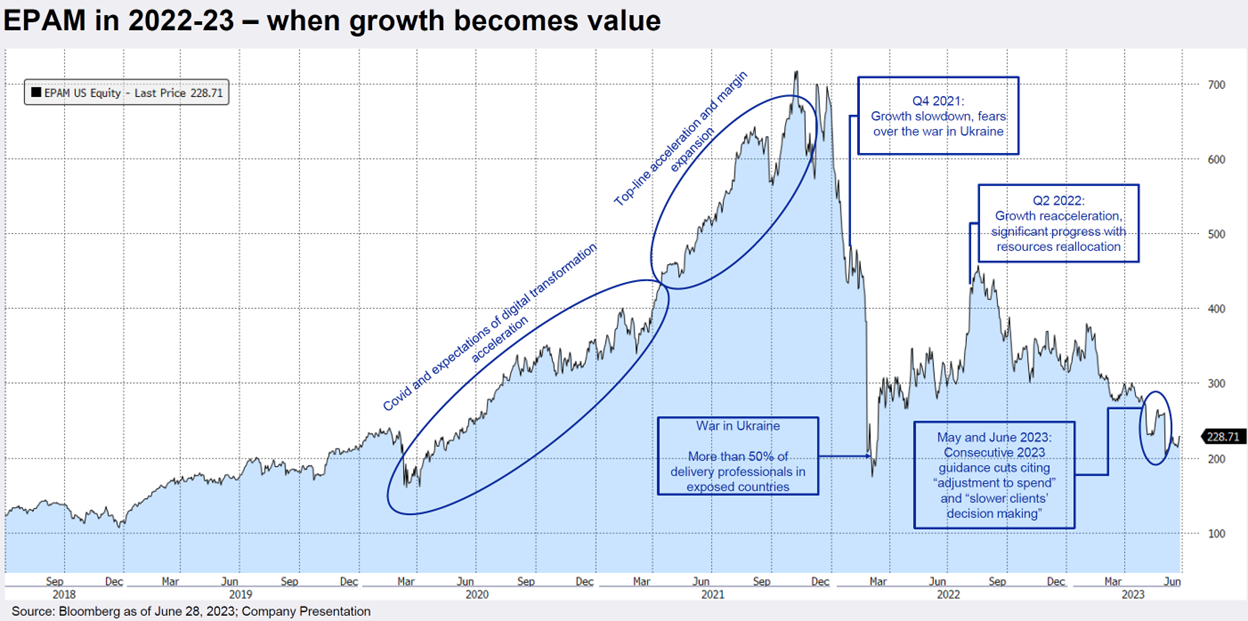

EPAM's winning streak came to an end in 2022.

With Russia's invasion of Ukraine the stock fell from $550 per share to $180 per share as the market was worried about EPAM's workforce/delivery centers in Ukraine, Belarus, and Russia.

The management at EPAM did a wonderful job derisking the company from this exposure. They exited Russia by not only leaving their clients there but also by closing their delivery centers in the country. By the end of 2022, EPAM's exposure to these volatile countries had reduced from 60% of overall workforce to 30% of overall workforce. EPAM moved some of the affected employees to neighboring countries and ramped up their hiring efforts in India and Latam. Due to this, the stock moved up to $450 per share a few months later in August 2022.

However, very recently, EPAM reduced their guidance for 2023. They first reduced their guidance during their earnings but then followed this up with a further reduction in guidance a few weeks later. The management is now expecting negative growth in 2023.

We first got involved with EPAM after it sold off in March 2022 but have recently added to the position. EPAM is not a "cheap" stock in the VIC sense of cheap but it is very cheap given the quality of the business and the tailwinds we see due to AI.

EPAM is currently available for 21x depressed 2023 earnings per share. It is a $12 bn market capitalization company with $1.7 bn in net cash and a $500 mn share repurchase authorization. An investor purchasing shares at these valuations can expect to compound with earnings growth with the added call option of multiple expansion if EPAM is once again seen as a durable growth franchise. We believe that is the most likely outcome.

And here's the conclusion:

EPAM remains a high-quality founder-led business that has hit a rough patch. We believe that this is a small bump and EPAM will get back to growth in a few quarters.

Overall, the company can be had for 21x depressed 2023 guided earnings. This is on a non-GAAP basis. Before 2022, analysts had estimates going to $16 per share in earnings for EPAM by 2025. While this is no longer possible, we model $14 per share in 2025 and $16+ per share in 2026. In addition to the reduction in growth, EPAM is also not optimized when it comes to margins. We believe it can move on to high teens margins in a more normalized environment.

In all this, AI remains a big variable and we think the surprise is likely to be on the upside.

This is a $320 to $400 stock in three years if they can do $16 in earnings per share in 3 years and get valued at 20-25x earnings. It is more likely than not that the multiple will be much higher if they do return to 20% plus growth.

Importantly, EPAM has a strong balance sheet with $1.7 bn in net cash and can buy back more shares or do tuck in M&A to further enhance shareholder value. EPAM has a $500 mn buyback authorization in place which should help with dilution and earnings accretion.

Economic cycle is a big risk. IT service providers are dependent on IT budgets which are then dependent on revenues. If there is a downturn in the economy and revenues come down – that will affect IT budgets.

3) This is so sad...

Despite my numerous warnings, retail investors got massacred as Bed Bath & Beyond spiraled into bankruptcy – and, as this Financial Times article notes, they have continued to suffer losses afterward: Investors spend $200mn on 'worthless' Bed Bath & Beyond shares. Excerpt:

Investors have spent almost $200mn trading theoretically worthless shares in Bed Bath & Beyond since the homewares retailer went bankrupt at the start of May, in the latest manifestation of the meme stock craze...

...an average of 18mn of the company's shares have changed hands each day on over-the-counter markets since then, according to Bloomberg data. Users of the Reddit website have been sharing highly speculative theories about possible turnround plans for the retailer...

"It's an extension, almost a mutation, of the meme stock phenomenon," said Anthony Chukumba, an analyst at Loop Capital Markets who previously covered Bed Bath & Beyond.

"We can have real debates about the value of Tesla, or GameStop for that matter, because it's still a viable company," he said, referring to other stocks favoured by retail investors. "We can't have a debate about the value of Bed Bath & Beyond because we know what that value is."

4) After nearly a half century of widening income inequality, driven by stagnating wages for working-class folks and huge gains for highly educated professionals and entrepreneurs, this article in the Wall Street Journal stunned me...

I had no idea that such a significant reversal has taken place: The Richcession Keeps Rolling. Excerpt:

Yet while the better-off are, by definition, better off than the poor, they have been hit harder by layoffs, have been less able to secure wage increases that keep up with rising prices and have been more affected by the slump in profits that began to take hold last year.

In other words, it is still looking like a richcession, where amid economic uncertainty, the rich feel more of the sting. And this, in turn, is beginning to have knock-on effects, with richer Americans reining in their spending relative to others.

Layoffs are still making headlines, and they are still disproportionately affecting higher-earning workers. By the count of outplacement company Challenger, Gray and Christmas, about one-third of layoffs announced by companies this year have come from tech firms such as Facebook parent Meta Platforms, where the median employee made $296,320 in 2022.

Job cuts elsewhere have been aimed at higher-paid workers, such as at Ford Motor, where planned layoffs are concentrated in the engineering ranks. Meanwhile, overall layoffs have remained low. Labor Department figures showing that even though the number of people in the workforce is higher than before the pandemic, fewer people are receiving unemployment benefits...

A tight labor market and in-demand skills mean that many well-off workers who lose their jobs can probably find new jobs fairly quickly – but maybe not at the same level of pay. Meanwhile, labor demand from industries that employ lower-paid workers remains elevated, and that is helping drive wage gains.

A wage tracker developed by the Federal Reserve Bank of Atlanta shows that the 12-month moving average of annualized monthly wage growth for workers in the bottom quartile by income was 6.8% as of May, compared with 5.6% for workers in the top quartile.

Economists David Autor, Arindrajit Dube, and Annie McGrew estimate low-wage workers' ability to switch into higher-paying jobs has unwound one-quarter of the wage inequality between top and bottom earners that built up in the four decades before the pandemic.

5) Here are some pictures from Italy of me with Ciccio, my friend's 10-month-old daughter (I LOVE little babies and have told my daughters to hurry up and give me grandkids!), all of the speakers, and Ciccio's family:

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.