The heartbreak continues for Brazilian state-owned oil firm Petrobras (PBR)...

The heartbreak continues for Brazilian state-owned oil firm Petrobras (PBR)...

The company is in the middle of a giant corruption investigation. We're shocked – shocked! – that an oil company controlled by the Brazilian government would get caught up in this kind of funny business...

New York law firm Wolf Popper LLC filed a class-action suit against Petrobras on Monday. The firm is filing on behalf of investors who bought the American Depositary Receipts (ADRs) – shares of foreign companies trading on U.S. exchanges – of Petrobras between May 20, 2010 and November 21, 2014. Wolf Popper alleges violations of the anti-fraud provision of the Securities Exchange Act.

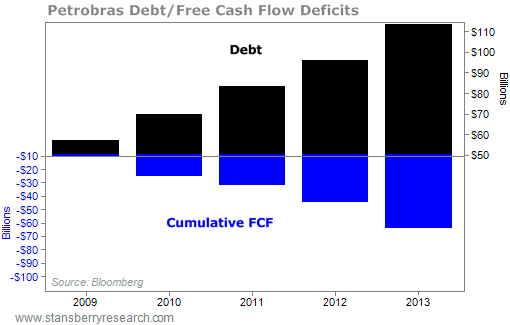

In addition to corruption, Petrobras is also horribly mismanaged (again, no surprise considering the Brazilian government's close involvement). Take a look at this chart Porter presented at our event in Nashville showing the company's mounting debts and shrinking cash flow...

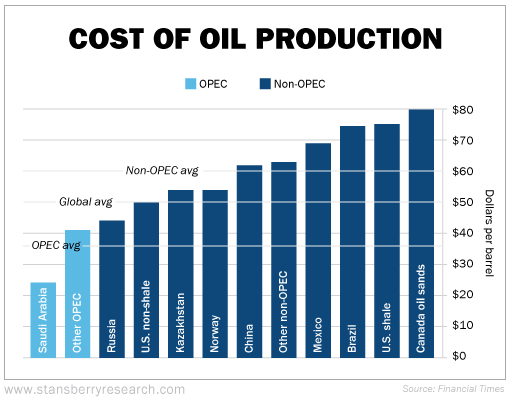

Finally, Petrobras is one of the highest-cost producers in the world. Its massive reserves are in super-deep water. And oil trading for less than $61 per barrel is squeezing the firm. Take a look at this infographic, which we've adapted from the Financial Times. As you can see, Brazil is one of the highest-cost producers in the world...

Finally, Petrobras is one of the highest-cost producers in the world. Its massive reserves are in super-deep water. And oil trading for less than $61 per barrel is squeezing the firm. Take a look at this infographic, which we've adapted from the Financial Times. As you can see, Brazil is one of the highest-cost producers in the world...

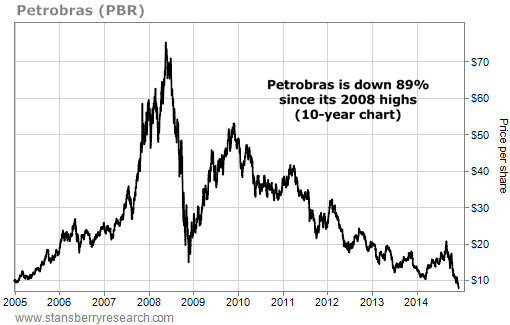

All of this adds up to Petrobras' struggling share price. Shares are down 64% since September nearly 90% from their mid-2008 peak...

All of this adds up to Petrobras' struggling share price. Shares are down 64% since September nearly 90% from their mid-2008 peak...

If you look back at the graphic showing global oil production costs, you'll see Brazil doesn't rank dead last... That title belongs to Canada's "oil mud" producers (or "oil sands"). Free-flowing U.S. shale oil basically rendered the Canadian oil sands useless. That's why Porter urged leading energy company Devon Energy to divest its oil sands assets and invest more time and capital into its shale assets.

If you look back at the graphic showing global oil production costs, you'll see Brazil doesn't rank dead last... That title belongs to Canada's "oil mud" producers (or "oil sands"). Free-flowing U.S. shale oil basically rendered the Canadian oil sands useless. That's why Porter urged leading energy company Devon Energy to divest its oil sands assets and invest more time and capital into its shale assets.

From the July issue of Stansberry's Investment Advisory...

|

Even worse is that commodity prices cannot be hedged over decades. As Porter explained, Devon was putting itself in harm's way...

|

Porter argued that Devon invested billions of dollars in the Canadian oil sands because it believed in Peak Oil... and feared it wouldn't be able to replace its oil reserves. At the time, the Canadian oil sands were one of the last-known large deposits of hydrocarbons.

Then, Devon discovered huge reserves in U.S. shales... Yet the company continues to invest $2 billion a year into its Canadian operations.

Canadian heavy crude recently hit $40 a barrel. It trades at a discount to WTI crude because of higher production costs and a shortage of pipelines (again thanks to U.S. shale). And low prices are crushing producers in the area. As Dinara Millington, Vice President of Research at the Canadian Energy Research Institute, told Bloomberg...

|

Like with the domestic shale plays, Canadian producers are also scaling back. Drilling giant Baker Hughes reported last week that Canadian drillers cut the number of rigs to its lowest level for this time of year since 2009.

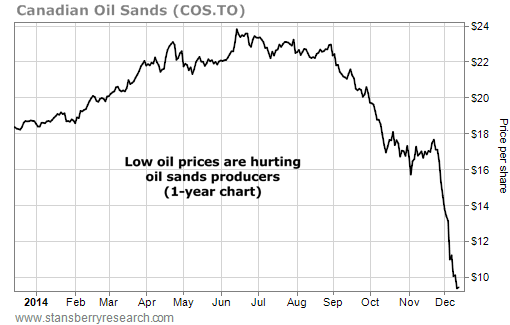

Canadian Oil Sands is one of the largest pure plays on the area. As you probably suspect, its shares are suffering...

Since the plunge in oil prices began, we've been writing about the deflationary forces at work in the world today...

Growth across the globe is slowing. We've written about the problems in China as well as Europe and Japan. All three are taking steps to spark inflation. Japan – under the direction of Prime Minister Shinzo Abe – is printing reams of cash. Today, China – whose economy is centrally controlled – told its banks to start lending more to boost economic activity.

Even Norway – the largest oil exporter in Western Europe – is feeling the brunt of it.

Statistics Norway, the country's official statistics agency, said oil companies will cut investment on oil projects 14% this year. That is expected to drag Norway's growth this year from 2.6% to 1%. As a result, 10% of Norwegian oil-sector employees – approximately 10,000 people – were laid off.

Because of the slowdown, Norway's central bank cut its main interest rate to 1.25% and suggested it may lower interest rates again next year.

China is the world's largest consumer of commodities. And when China slows down, commodity markets stutter...

Commodities across the board – not just oil – have suffered. Since July, coal is down 17%, platinum is down 17%, and iron ore (a key ingredient in steel) is down 17%.

As such, shares of the companies that move these commodities – shippers – are experiencing a slowdown.

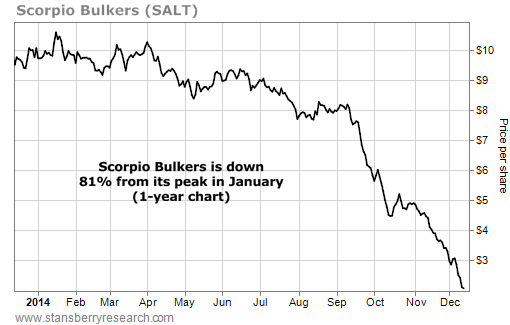

Take a look at this chart of Scorpio Bulkers... The company ships coal, iron ore, agricultural commodities, and other dry bulk goods. If you're looking for a sign of slowing global growth, this is it...

As you can see, Scorpio shares have gotten clobbered. But keep your eyes on shippers... Like commodities, shipping is a boom and bust industry. And we're getting close to a bottom.

New 52-week highs (as of 12/10/14): CME Group (CME) and ProShares Ultra 20+ Year Treasury Fund (UBT).

In the mailbag... one more satisfied Cubist shareholder. Send your questions and concerns to feedback@stansberryresearch.com.

"Thank you for this recommendation. It worked out beautifully for me as I went long as and when recommended. It would have been even better if I had also gone long some calls – but I am mindful that while bulls and bears may profit, pigs rarely do. I greatly appreciate the rest of Stansberry's Investment Advisory, thank you. Have a great holiday season." – Paid-up subscriber Goetz Oertel

Regards,

Sean Goldsmith

Baltimore, Maryland

December 11, 2014