Protect Your Portfolio With These Simple Rules

Editor's note: There's more to investing than choosing great businesses...

When building a portfolio, many people tend to focus on putting as much money as possible into strong companies. But Keith Kaplan, CEO of our corporate affiliate TradeSmith, says finding the best stocks is only the start. To truly grow your wealth, you can't rely on your "gut instinct" – you have to make a plan...

According to Keith, investors can use a number of factors to reduce their risk in the markets. And if you're overlooking these concepts, it could cost you a lot of money...

That's why this weekend, Keith is sharing his three "key rules" for being a successful investor. In today's Masters Series – a combination of the February 5 and May 21 issues of his Money Talks e-letter – Keith reveals the first two rules... and explains how you can easily implement them in your portfolio today...

Protect Your Portfolio With These Simple Rules

You are an emotional being...

It has gotten you this far in life... and that's probably a good thing. But it's almost certainly costing you money.

You see, I believe most people who are buying and selling stocks are actually pretty great at picking them. But they are terrible investors.

Don't feel bad. In the past, I definitely would've said that about myself, too. (And I had the terrible track record to prove it!)

Just think about this for a minute...

When you buy a great stock, how do you decide when you'll sell it? If you're like most folks, you probably don't give it much thought. But that's a mistake.

This isn't the type of decision you want to leave up to your "gut." Save that for dinner, movies, relationships, and so forth.

You see, here at TradeSmith, we believe you must know three key rules to be a successful investor. And the first rule is this...

- You should have a clearly defined exit strategy for every position you own.

That's why we love trailing stops.

A trailing stop is simply a "stop" (or sell) price set at a specific percentage below the current price of an investment.

As the price of that investment rises, the stop price "trails" or follows it higher. But if the price falls, the stop price stays the same. It never moves lower.

If or when the price of that investment closes below the trailing stop price, you simply sell that investment and wait for signs of a new uptrend before getting back in.

This means not only can trailing stops protect you from big losses in your worst-performing investments, but they can also help you "lock in" gains and realize even bigger returns from your winners.

And best of all, they do so while taking all the emotion out of investing, so you can sleep well at night.

That should be your biggest goal!

In other words, trailing stops are about as close to the "perfect" exit strategy as you're likely to find. And I personally use and recommend them for just about every public-market investment out there, including individual stocks, exchange-traded funds ("ETFs"), most stock and bond mutual funds, and even options.

(Unfortunately, trailing stops are difficult to use in privately traded or less "liquid" assets like real estate, individual bonds, collectibles, and so on.)

Next, I'm going to explain the basics of fixed-percentage trailing stops...

As you can probably tell by the name, these are stops that are placed at a fixed percentage – like 15%, 20%, or 25% – below the purchase price of an investment.

For the following examples, we'll use a 25% trailing stop, but the idea is the same regardless of the percentage used.

Suppose we believe shares of Company ABC are likely to rise, so we decide to make an investment at $10 per share. Because we've decided to use a 25% trailing stop, our initial stop price would be set 25% below our purchase price, or $7.50.

At this point, one of two things could happen: The stock price could move up as we expected, or it could fall. So let's take a look at what would happen to our trailing stop in each of those scenarios...

If the stock immediately moved lower, our stop price would not move lower with it. (Remember, trailing stops can only move higher, not lower.) It would remain at $7.50. If the stock were to keep falling and close below $7.50, we would sell our position the next day.

Because we chose a 25% trailing stop, we can rest assured we won't lose much more than 25%... even in the worst-case scenario.

Now, let's take a look at what could happen if we were right and the stock moved higher right out of the gate.

If the stock moved 10% higher to $11, our trailing-stop price would move higher along with it to $8.25. Notice this is not only 10% higher than it was before (just like the current stock price), but also still exactly 25% below the current stock price.

No matter how high the stock price rises, this will always be the case.

If the stock moved higher to $13.34, our trailing-stop price would move to $10, equal to our entry price. At this price, our trailing stop would allow us to exit around "breakeven," even if the stock suddenly turned lower.

If the stock really took off and hit $20, our trailing stop price would move to $15. In this case, we would be all but guaranteed to lock in a great profit no matter what happened next.

At TradeSmith, we've done hundreds of studies on different investor portfolios. We've looked at the portfolios of individual "mom and pop" investors... the most successful analysts in the newsletter world... even the "best of the best" billionaire investors like Warren Buffett and David Einhorn.

And in almost all scenarios, putting a simple 25% trailing stop in place allowed those portfolios to perform much better.

I would say that the only exception to this rule involves higher-risk, more speculative stocks. These typically include companies with tiny market caps, low trading volumes, and those in highly cyclical and volatile businesses like resource mining, among others.

These kinds of riskier stocks aren't necessarily right for everyone. But if you're going to own them, our research shows using a wider trailing stop of 40% on these stocks can produce better overall returns. Just be sure to keep your position sizes much smaller in these stocks to account for the wider-than-usual trailing stop.

Tracking your fixed-percentage trailing stops isn't difficult, either. While our TradeSmith software can do it for you automatically, you can easily track them yourself in a basic spreadsheet.

To calculate your trailing stops, you really only need two pieces of information for each stock...

- The stock's highest CLOSING price since you bought it.

- The fixed-percentage trailing stop you'd like to use.

The math works like this:

Trailing Stop Price = Highest Close Price Since Purchase - (Highest Close Price Since Purchase x Trailing Stop Percentage)

In our last example of a stock trading at a new high of $20 with a 25% trailing stop, it would look like this...

Trailing Stop Price = $20 - ($20 x 0.25) = $15

Notice I emphasized "closing" prices. This is because even the least-risky stocks sometimes experience big intraday price swings that can trigger stop prices before reversing.

Using closing prices helps to eliminate this "noise" and ensure you aren't kicked out of a position prematurely.

Unfortunately, trailing-stop orders at most brokerages are typically based on intraday prices rather than closing prices. This is one of the biggest reasons we recommend tracking your trailing stops yourself, rather than placing them with your broker.

(The other has to do with the risk of "stop hunting." While it's probably less likely with today's digital trading platforms than it was in the past, there may still be a risk that market makers – the firms that match buy and sell orders – could see your stop and exploit it.)

Trailing stops can make a huge difference in your investing. And I can tell you this from my own personal experience...

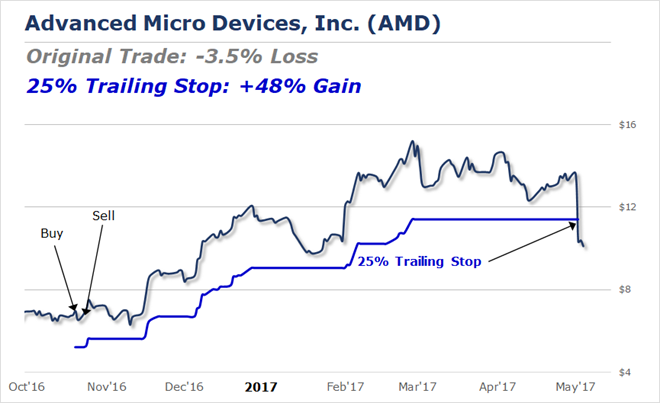

A few years ago, before I joined the TradeSmith family, I bought shares of a company you might have heard of called Advanced Micro Devices (AMD).

I won't bore you with all the details about why I bought AMD. All you really need to know is that I thought the market had mispriced the stock... and I was convinced it would quickly head much higher.

Well, as you can probably guess, that was not what happened. It went up a little, then it went down a lot more. I immediately began to second-guess my decision. And when it finally bounced back to near my entry price, I gave up and sold my shares for a small 3.5% loss.

A small loss is certainly better than a big one. It could've been worse. But it turns out if I had done absolutely nothing different except used a 25% trailing stop on that stock, the outcome would've been much different.

Instead of selling for a 3.5% loss, I would've held on for a 48% gain less than one year later.

That's a HUGE improvement. And even better, I could've avoided the emotional roller coaster that had led me to sell those shares too soon in the first place.

I hope this explanation helped clear up some confusion about the "basics" of trailing stops. If you do nothing else, please consider removing some of the emotion from your financial life by using a 25% trailing stop on all your investments today.

Now, let's move on to the second rule of successful investing...

- You should never risk too much of your money in any single position.

This rule pertains to what we call "position sizing."

Like our other two rules, this one is pretty easy to understand. But don't let that fool you. It's super important. In fact, it may be the most important of the three.

That's because proper position sizing is your first line of defense against what's known as a "catastrophic loss."

A catastrophic loss is the kind of loss that wipes out a massive chunk of your savings. It can set your retirement back years... or even decades. And it's almost always the result of betting too much – of going "all in" – on a single stock or investment.

Of course, even the world's best investors suffer losses. Losses are a natural and unavoidable part of investing.

But if you hope to be successful over the long run, you must keep those losses relatively small.

It's just simple math. As losses grow larger, the return required to recover those losses grows much faster. For example...

- A loss of 10% requires an 11.1% gain to break even

- A loss of 25% requires a 33.3% gain to break even

- A loss of 50% requires a 100% gain to break even

- A loss of 75% requires a 300% gain to break even

- A loss of 90% requires a 900% gain to break even

As you can see, the numbers really start to get ugly above a 50% loss. So your priority as an investor should be to avoid those kinds of losses.

Like I said, proper position sizing is one of the best and easiest ways to do so. And it all starts with changing how you think about your investments.

Pause for a moment and just answer this question to yourself first...

"How do I determine how much money to put into a trade?"

And if you're seasoned, answer that question to yourself relating to when you bought your first stock!

You see, novice investors tend to think about position size in terms of how many shares they own of a particular asset. And they typically don't put much thought into this decision. Often, they decide based on little more than the share price of the asset and how bullish they're feeling.

For example, they may buy 100 shares of Stock A, 300 shares of similarly priced Stock B (which they're really excited about), 10 shares of higher-priced Stock C, 1,000 shares of lower-priced Stock D, and so on.

But a better way to think about position sizing is in terms of risk. In other words, how much of your total portfolio are you risking in each position?

I recommend a "risk parity" approach to investing. That's just a fancy way of saying you should risk the same amount of money in each position. And I generally recommend limiting that risk to no more than 3% or so of your total portfolio in each position.

For most folks, most of the time, risking somewhere between 1% and 2% is probably ideal. But if you're new to investing or extremely risk-averse, there's no reason you can't initially risk 1% or even less.

Once you've decided how much you're comfortable risking in each position, you can easily calculate the appropriate position size for a particular investment in just four simple steps.

As a simple example, we'll assume you have a $100,000 portfolio, are willing to risk 2% of your portfolio in each position, and want to invest in a stock trading at $10 per share.

First, you'll multiply your total portfolio size ($100,000) by your preferred risk percentage (2%) to come up with the nominal amount of risk per position...

$100,000 x 0.02 = $2,000

Second, you'll choose a trailing stop loss for this position using the guidelines I laid out earlier. You'll then divide 1 by your trailing-stop percentage. For this example, we'll assume you're using a 25% trailing stop...

1 ÷ 0.25 = 4

Next, you'll multiply the result of the first step by the result of the second step to get the total position size...

$2,000 x 4 = $8,000

And finally, you'll divide the total position size by the share price of the stock you want to buy...

$8,000 ÷ $10 = 800 shares

So in this case, you'd buy 800 shares of the stock.

If the stock were to fall and hit its 25% stop loss, you would stand to lose just $2.50 per share. That's $2,000, or 2% of your total portfolio.

That's all there is to it.

And the math works the same regardless of portfolio size, risk tolerance, trailing-stop percentage, or share price.

Tomorrow, I'll share the third rule of successful investing. In the meantime, if you're not already using them, I hope you'll give trailing stops and position sizing a try today.

Good investing,

Keith Kaplan

Editor's note: Keith says fixed-percentage trailing stops and position sizing can help keep you from taking on too much risk. But there's another strategy he believes is far better than a "one size fits all" approach...

In short, Keith and the TradeSmith team have developed a "smarter" way to calculate trailing stops... uniquely tailored to each position in your portfolio. He says this method can even prevent you from selling too soon – ensuring you don't miss a massive run-up.

Keith shared all the details about his one-of-a-kind system in a special presentation... including how it could have warned you about the March 2020 COVID-19 crash days before it happened. Click here to learn more.