A review of our warnings...

A review of our warnings... Why the 'lions' are still hunting... How to profit from panic... Victim or victor, what's it going to be?...

![]() There's a clear message in the markets today...

There's a clear message in the markets today...

Default rates on corporate bonds are rising. The "spreads" on corporate bonds – how much higher interest rates are on corporate bonds, as compared with Treasury bonds – are soaring...

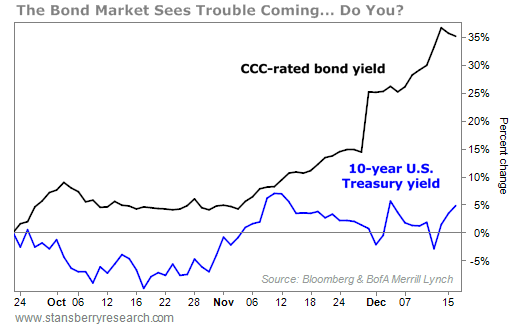

The following chart shows the percentage change in the yield of both the 10-year U.S. Treasury bond and the high-yield CCC-rated corporate bond...

![]() Thus, despite generally low interest rates, the conditions are already much tighter for corporate credit. And after nearly 14 years without a complete default cycle, there's tremendous fear that the long-delayed "cleansing" of the corporate-bond market has begun. And even though we're still in the early stages, we're already seeing massive redemptions in bond funds.

Thus, despite generally low interest rates, the conditions are already much tighter for corporate credit. And after nearly 14 years without a complete default cycle, there's tremendous fear that the long-delayed "cleansing" of the corporate-bond market has begun. And even though we're still in the early stages, we're already seeing massive redemptions in bond funds.

![]() We've been warning about the inevitability of this debt cycle for the past two years. And on the week of July 24, I saw what looked like panicked and forced selling in the precious metals sector. We thought the action was a warning sign for the broader market. We recommended taking profits in stocks...

We've been warning about the inevitability of this debt cycle for the past two years. And on the week of July 24, I saw what looked like panicked and forced selling in the precious metals sector. We thought the action was a warning sign for the broader market. We recommended taking profits in stocks...

I believe that some combination of rising interest rates, rising defaults in the corporate-bond market, and global currency/trade wars will likely cause the U.S. stock market to decline substantially. No, I don't know the exact timing of such a move. But I believe it will happen within the next few months... I recommend that you sell about 10% of your existing portfolio.

![]() Our warnings got more specific in mid-August. On August 14, I warned that "financial gravity" – the rising cost of capital – was sure to cause a bear market...

Our warnings got more specific in mid-August. On August 14, I warned that "financial gravity" – the rising cost of capital – was sure to cause a bear market...

The credit stimulation our economy received was phony. The capital wasn't earned or saved. The positive result was a boom. But these investments and this consumer borrowing happened in an environment nearly free of capital costs (zero gravity). In this world, almost anything would "fly."

A lot of the money invested in the oil business, for example, has gone into projects (like the oil sands) that aren't economic and aren't likely to be in a lifetime. A lot of cars were built and sold to people who can't actually afford them. These people will eventually default...

That's the downside to a phony boom. Since these investments weren't financed with actual savings, there won't be enough demand to sustain the debts that have been created... For the last six years, that has meant our economy was on "tilt" in a way most people think of as positive: huge investments in oil, plenty of credit for consumers.

Now, the opposite kind of "tilt" looms right in front of us. The boom, as it was not financed with savings, will surely lead to a bust of similar magnitude... These poor investments and poor lending decisions involved hundreds of billions of dollars in bonds and loans that have been packaged into bond-like securities. The worsening performance of these debts will eventually "spill over" into other areas of the bond market.

As I've been warning since 2013, the high-yield bond market reached completely unsustainable levels thanks to the Fed's massive credit inflation. As this credit bubble deflates, "gravity" will return to our economy. Capital costs will begin to grow. Terms for credit will get tougher. The rising cost of capital will result in bad loans, bankruptcies, repositions, unemployment, softer demand, and lower securities valuations. Winter is coming, friends.

![]() A week after I wrote those words, the Dow dropped 1,000 points in a day.

A week after I wrote those words, the Dow dropped 1,000 points in a day.

And the sectors we'd been warning about led the move lower. These are the "lions" we warned would continue to devour investors who didn't yet understand how serious the problems in credit had become. As I explained...

In summary, the lions are still hunting. Don't be a zebra. Don't ignore these problems. Wait for some concrete signs of stability in the oil industry, emerging markets, corporate high-yield debt, and in the Dow Jones Transportation Average before you make any major investments in U.S. stocks. In my view, there's almost certainly another 20%-30% decline ahead of us... maybe more.

.png)

![]() As I've tried to explain and show you, problems in the credit markets are far more serious than a simple stock-market correction. There are hundreds of billions of dollars of bad debt in the U.S. energy sector alone.

As I've tried to explain and show you, problems in the credit markets are far more serious than a simple stock-market correction. There are hundreds of billions of dollars of bad debt in the U.S. energy sector alone.

With Iran ramping up production, Venezuela striving to avoid a complete economic collapse, and Saudi Arabia fighting a proxy war in Yemen, there's simply no chance of any material reduction in oil supplies in 2016.

As U.S. oil and gas firms see their hedges roll off, there will be another massive reduction in cash flows for that industry. There will be massive bankruptcies across the sector and up and down the supply chain. See the big move today in Teekay LNG Partners (TGP) – down 50% as of midday trading – as a sign of things to come.

And those are merely the most obvious problems. After record issuance of high-yield bonds over the past five years, a huge wave of default is bound to happen. That's the way the market works: Rapid growth in outstanding credit is always followed by a similar increase in defaults.

Just remember that between 2011 and 2014, we saw three years of record high-yield issuance, each of which more than doubled the previous all-time high issuance. There's an enormous wave of bankruptcy and default ahead of us. Winter is coming.

![]() Generally speaking, most stock investors don't pay enough attention to the bond market. Professional investors, on the other hand, know that bond investors tend to be much better informed and more rational about the prospects for a given business. That's why we always look at a company's bonds (and its balance sheet) before we look at any other factor. It was our focus on credit that allowed us to see trouble coming this year to stocks. And it's what will help us continue to guide you through this credit-default cycle. Our expertise in credit gives us a gigantic advantage in the equity markets.

Generally speaking, most stock investors don't pay enough attention to the bond market. Professional investors, on the other hand, know that bond investors tend to be much better informed and more rational about the prospects for a given business. That's why we always look at a company's bonds (and its balance sheet) before we look at any other factor. It was our focus on credit that allowed us to see trouble coming this year to stocks. And it's what will help us continue to guide you through this credit-default cycle. Our expertise in credit gives us a gigantic advantage in the equity markets.

![]() Now... you have a choice to make. You can do one of two things to be successful as an investor over the next two or three years. The first is simple: All you have to do is break even to beat the equity markets. Stocks will finish this year down. They will be down next year, and probably in 2017, too.

Now... you have a choice to make. You can do one of two things to be successful as an investor over the next two or three years. The first is simple: All you have to do is break even to beat the equity markets. Stocks will finish this year down. They will be down next year, and probably in 2017, too.

Going to cash and holding short-term (90-day) Treasury bills will almost certainly be a winning strategy. The trouble is, few people can survive not earning any income whatsoever on their financial assets. So while going to cash might be the safest and most logical choice... it isn't practical.

![]() The other option is to do some mixture of these three things:

The other option is to do some mixture of these three things:

1. Sell short companies with weak balance sheets in sectors of the market that are harmed the most by overcapacity. That's energy, retail, technology, auto, and finance. These kinds of trades have been working in energy and retail. They've just started working in finance. They will begin working in the technology and auto sectors next year.

Shorting is difficult and scares most people. But trust me when I tell you this: Shorting stocks with 10% to 20% of your portfolio over the next two years will dramatically reduce the risks you face. I'm 100% certain our short-sell recommendations will prove to be extremely profitable over the next 24 months.

If you've never shorted a stock before, now is the time to try it. As always, my advice if you've never done something before is to call your broker and talk about what you want to do. Make sure he can explain it to you thoroughly. Then, start small. Short a single share. See how it goes. If you're comfortable and you understand how it works, short larger amounts. As you'll find out, there's essentially no difference between buying stocks and shorting them, if you're using a good broker.

2. Look to buy high-quality credit when, during periods of market panic, the corporate-bond market goes "no-bid." We've already seen panic grip the corporate-bond market. That's what happened a week ago when famed investor Carl Icahn went on CNBC and warned everyone (yet again) that the size of bond mutual funds and bond exchange-traded funds ("ETFs"), mixed with the relative illiquidity of the bond market, was a recipe for an eventual disaster.

We got the first taste of that as the iShares iBoxx High-Yield Corporate Bond Fund (HYG) was hit with $1 billion in redemption demands in one day. Over the next two years, there will be plenty of "forced selling" of relatively illiquid corporate debt. These will be unbelievably good opportunities – as good as or better than the similar opportunities we saw back in 2009.

If you're reading our Stansberry's Credit Opportunities newsletter, you should be able to build a portfolio of four-to-seven-year maturities, offering current yields, on average, between 15% and 25%, and average capital gains of more than 15% annually. These returns will dwarf what you could make in stocks over the next five years.

3. Learn to trade stock-market volatility to generate immediate income and substantial capital gains. Remember... the market isn't going to go straight down. There will be plenty of bull moves. And bull moves tend to be extremely volatile during bear markets. We've been talking about a strategy to capitalize on this volatility over the past five Digests. I've written them all personally because I believe this information is the most valuable advice I could give you as we face this bear market.

The strategy is easy to understand. We simply wait until volatility (as measured by the "VIX") soars to more than 20 (good), 30 (better), or 40 (best)... and then we sell puts on stocks we want to own, at strike prices we are genuinely happy to pay. The time to buy stocks is during bear markets. That's when you're going to get great businesses at good prices. There's virtually no risk to being paid 10% or 15% in premium to buy a stock you want to buy anyway, for significantly less than the market price.

But we aren't selling these puts with the intention of buying. We don't want to tie up our capital. That's why it's important to have a Level IV options account, so that you are able to use margin in these trades. Doing so will allow you to trade more contracts and generate more income. We'll try to roll our capital every 60 to 90 days to produce mountains of income.

Unlike other put-selling strategies, we also will spend some of this income to purchase call options on the stock. That will allow us to capture the potentially explosive upside of a bull move in the markets. The reality is, even though we're trading options on stocks, what we're really doing is capitalizing on the impact of volatility in the options market. We're selling puts when put premiums soar. And we're buying calls when they're cheap, because we know that sooner or later, the market's volatility will produce a dramatic move higher, too.

![]() Naturally, many subscribers haven't understood why this strategy works, or even what it's supposed to do. The biggest misunderstanding is that what we're doing is tantamount to just buying the dips. No, that's not what we're doing.

Naturally, many subscribers haven't understood why this strategy works, or even what it's supposed to do. The biggest misunderstanding is that what we're doing is tantamount to just buying the dips. No, that's not what we're doing.

Let me show you a real-life example of how a trade would work out using our Stansberry Alpha strategy...

Last Friday, the VIX closed at 24. That would give us a green light to trade, following our distressed-equity strategy. We'd pick up our "shopping list" and find a stock to trade options on. We're looking for the world's absolute best businesses – companies with great operating margins, plenty of cash flow, great brands, capital-efficient business models, great balance sheets, and absolute certainty of future growth. We're also looking for companies that, for one reason or another, are under some distress. Even great businesses can suffer from temporary pressures.

![]() Here's one example: fashion icon Ralph Lauren (RL). Surely you know the business, its brands, and its products. This is a very good business. Even with the strong dollar (which has caused weak earnings this year), the company still earns nearly 10% a year on its assets and 15% a year on its equity – all powered by operating margins above 12%. This year, the business will produce something around $900 million in cash and return around $600 million to shareholders through dividends and buybacks. This is a rock-solid business that everyone should be happy to own at a reasonable price.

Here's one example: fashion icon Ralph Lauren (RL). Surely you know the business, its brands, and its products. This is a very good business. Even with the strong dollar (which has caused weak earnings this year), the company still earns nearly 10% a year on its assets and 15% a year on its equity – all powered by operating margins above 12%. This year, the business will produce something around $900 million in cash and return around $600 million to shareholders through dividends and buybacks. This is a rock-solid business that everyone should be happy to own at a reasonable price.

What's a reasonable price? Well, this year, the stock has fallen from $180 all the way down to around $100. The company named a new CEO, which saw its shares bounce back to around $115. At these prices, you're buying Ralph Lauren for around eight times its cash flow, including all of its debt. That's a good price to pay for a great business. Over the long term, I'd expect equity investors to make 10% to 15% a year in this stock by buying at these prices.

But last Friday, the market panicked. Shares of Ralph Lauren fell from $115 to $112. The prices of its put options rose. We could have sold put options with a strike price of $115 – because we believe the stock is very undervalued at its current price. These options were trading for around $11 (up from $8 the day before) last Monday.

Selling 10 options contracts at $11 would instantly generate $11,000 for you. Your potential obligation – to buy 1,000 shares of Ralph Lauren – would require $115,000 of capital in your account. But using margin, you would only have to set aside $23,000 for this trade.

(If you don't have that much capital, or if such a position size would be more than 10% of your account, then you could sell fewer options contracts. I'm using 10 contracts to make the math easy for everyone to understand.) On this margin ($23,000) this trade would earn nearly 50% in about four months. You aren't going to make that kind of return buying stocks.

Meanwhile, chances are good that you will not even have to buy the stock. To be "put" these shares, Ralph Lauren would have to trade below $115 between now and next April. To lose money on this trade, shares would have to fall to less than $104.

The put premium you received gives you a huge "cushion" that folks who are merely buying the dip won't ever get. And this cushion – combined with the already dirt-cheap price of the stock – gives us a wide margin of safety. The put premium is the key to the whole deal. It gives us cushion for the stock to fall and it generates immediate cash. We can use that cash to buy call options. And that's where the big payoffs are...

![]() This is the part of the trade that most people will never understand... but it's critical to your success. Last Friday, while put option prices were moving much higher (because the market was falling), the call options were falling in price. That doesn't make sense. Volatility was soaring... but call options react differently to volatility than put options do.

This is the part of the trade that most people will never understand... but it's critical to your success. Last Friday, while put option prices were moving much higher (because the market was falling), the call options were falling in price. That doesn't make sense. Volatility was soaring... but call options react differently to volatility than put options do.

The price of Ralph Lauren's April $130 call options fell from $3.50 to $2.70. That means you could have bought a call option to pair with each put option you sold and still keep $8.30 in put premium. That's the beauty of an Alpha trade during a distressed-equity market: You can get huge amounts of downside protection on the stocks you want to own, and the upside is almost free.

![]() What will happen next? Well, Ralph Lauren has a "beta" of 0.63. That means it's about 40% less volatile than the market as a whole, on average. Assuming you use $2.70 of your put premium to buy the call option, you're protected from loss in the shares down to $106.70.

What will happen next? Well, Ralph Lauren has a "beta" of 0.63. That means it's about 40% less volatile than the market as a whole, on average. Assuming you use $2.70 of your put premium to buy the call option, you're protected from loss in the shares down to $106.70.

Or, in plain English, the stock has to fall another 6% before you'll lose money on this trade. That would make you "long" Ralph Lauren at a price that's more than 40% below its 12-month high and well below its low for the year ($108). In fact, with the exception of the most recent selloff in August and September, the stock hasn't closed below $108 since 2011. And because Ralph Lauren isn't a volatile stock, that's highly unlikely to happen, unless the stock market as a whole falls another 10% or more before next April. While that's possible... it's not likely.

![]() There are lots of other ways to structure these trades if you want to be more conservative. You could have selected a lower strike price and have had a much lower chance of being put the stock. But I would have been comfortable with the $115 strike price because Ralph Lauren is a stock we'd love to own and we doubt the stock will trade below its recent lows. In fact, we think it's likely the stock performs well next year. If it does, we could have made big profits with our call options.

There are lots of other ways to structure these trades if you want to be more conservative. You could have selected a lower strike price and have had a much lower chance of being put the stock. But I would have been comfortable with the $115 strike price because Ralph Lauren is a stock we'd love to own and we doubt the stock will trade below its recent lows. In fact, we think it's likely the stock performs well next year. If it does, we could have made big profits with our call options.

![]() Executing these trades is an excellent and low-risk way to generate lots of income during market panics. I promise... if you start doing this kind of trading, you may decide to stop buying stocks altogether. I know you think that seems like an exaggeration, but there's no doubt that on average, you'll make more money and you'll take less risk doing this type of trading – and that's especially true when put premiums soar thanks to market volatility.

Executing these trades is an excellent and low-risk way to generate lots of income during market panics. I promise... if you start doing this kind of trading, you may decide to stop buying stocks altogether. I know you think that seems like an exaggeration, but there's no doubt that on average, you'll make more money and you'll take less risk doing this type of trading – and that's especially true when put premiums soar thanks to market volatility.

At the very least, I urge you to set up your account so that you can make these types of trades and try, at least once, to see how it goes for you. To learn more, I encourage you to attend our webinar this evening. It starts at 8 p.m. And it's not too late to sign up. The education is free. Click here to reserve your spot.

![]() In closing... I hope you realize that I've personally done everything I could to help you understand and prepare for the tough market conditions I expect to see next year and beyond. If I've helped you at all, I hope you'll take the time to drop me a quick note. Knowing that I'm helping even one person makes a big difference to me: feedback@stansberryresearch.com.

In closing... I hope you realize that I've personally done everything I could to help you understand and prepare for the tough market conditions I expect to see next year and beyond. If I've helped you at all, I hope you'll take the time to drop me a quick note. Knowing that I'm helping even one person makes a big difference to me: feedback@stansberryresearch.com.

![]() Meanwhile, almost all of the notes we get are from folks who don't understand what we're trying to do. I can't explain our strategies in more detail than I've done here. It's not that they can't understand what we're doing... it's that they can't abandon their long-held prejudices. Logic has nothing to do with it. It's all pride.

Meanwhile, almost all of the notes we get are from folks who don't understand what we're trying to do. I can't explain our strategies in more detail than I've done here. It's not that they can't understand what we're doing... it's that they can't abandon their long-held prejudices. Logic has nothing to do with it. It's all pride.

![]() Even worse are the letters I get from folks who wouldn't lift a finger to help themselves. They wouldn't find a broker to help them. They wouldn't get an options-trading account. They wouldn't call around to find that bond. They couldn't be troubled to short a stock. And they're sorry, but there's no point to reading our newsletters anymore because their money is all gone.

Even worse are the letters I get from folks who wouldn't lift a finger to help themselves. They wouldn't find a broker to help them. They wouldn't get an options-trading account. They wouldn't call around to find that bond. They couldn't be troubled to short a stock. And they're sorry, but there's no point to reading our newsletters anymore because their money is all gone.

Nothing makes me want to pull out my hair more than listening to you, dear subscribers, invent yet another excuse to explain why, even when you knew that trouble was coming, you did nothing to protect yourself. And that's exactly what most of you will do. You will suffer huge losses because you aren't willing to try something new.

![]() The unfortunate truth is that most of my readers – probably more than 90% – will never short a stock. They will never buy a distressed credit. And they will never put on an Alpha trade. For all of these people, rising yields, soaring volatility, and falling stock prices will be the harbingers of enormous wealth destruction.

The unfortunate truth is that most of my readers – probably more than 90% – will never short a stock. They will never buy a distressed credit. And they will never put on an Alpha trade. For all of these people, rising yields, soaring volatility, and falling stock prices will be the harbingers of enormous wealth destruction.

I can only lead the horse to water. I can't make him drink. But there is no reason you should fear bear markets, or distressed credits, or volatility. There are reasonable strategies (not crazy risk-taking) to profit from these market environments. In fact, it's easier to make big returns in volatile markets and in distressed credit than it is to make big gains in most bull markets. The best time to take advantage of our research is during these tough markets.

But... you have to take the first step. You have to educate yourself. You have to pay attention. And you have to get your account set up to do this kind of trading. None of this stuff is hard... it just takes a tiny bit of effort.

So please... for Pete's sake... do something. Don't just sit there and pretend that it's all too complicated for you. Anyone can do these things. Anyone. All it takes is just a tiny bit of effort on your part. A few phone calls. A little bit of reading. You can either be a victim or a victor. What's it going to be?

![]() New 52-week highs (as of 12/16/15): Becton Dickinson (BDX), Bristol-Myers Squibb (BMY), Delta Air Lines (DAL), Coca-Cola (KO), McDonald's (MCD), Microsoft (MSFT), NovaGold Resources (NG), and Public Storage (PSA).

New 52-week highs (as of 12/16/15): Becton Dickinson (BDX), Bristol-Myers Squibb (BMY), Delta Air Lines (DAL), Coca-Cola (KO), McDonald's (MCD), Microsoft (MSFT), NovaGold Resources (NG), and Public Storage (PSA).

![]() In the mailbag, one subscriber has had success with selling puts, and another asks about portfolio sizes. Send your questions to feedback@stansberryresearch.com.

In the mailbag, one subscriber has had success with selling puts, and another asks about portfolio sizes. Send your questions to feedback@stansberryresearch.com.

![]() "I began selling naked puts April of this year. I wish I would have started three years ago but it took me that long to get comfortable with the idea. Now, I know there is no better way to make money in the stock market, safely. In fact, it is the only thing I do in the market now.

"I began selling naked puts April of this year. I wish I would have started three years ago but it took me that long to get comfortable with the idea. Now, I know there is no better way to make money in the stock market, safely. In fact, it is the only thing I do in the market now.

"I have 'retired' to do this full-time, living near the beach and playing golf. And it takes surprisingly little money to do it. The last four puts I sold my average gain was 5.3%, with all positions held less than 8 days. The companies: SAVE, MET, ORCL and AAPL. All companies I would want to own at the strike price I chose. As a Flex Alliance member I often use specific Stansberry Research recommendations, but more importantly I have learned how to create my own trades, and thus become self-employed, by studying your work.

"It is also a relief to know that using this strategy I can make money regardless of the market direction. In fact, my ROI has increased since August. I do not fear the next correction or crash. I no longer worry about being long or short and what the futures are when I wake up in the morning. Most days I can enter my trades at the price I want and then walk away. My blood pressure is down and my retirement outlook is up." – Paid-up subscriber Bob B

![]() "Porter, is it wise to begin selling puts of the type you are currently describing with a portfolio of only $15,000? It seems like I would only have enough money for a few trades since I am possibly buying 100 shares of a stock if the price goes down far enough." – Paid-up subscriber James P.

"Porter, is it wise to begin selling puts of the type you are currently describing with a portfolio of only $15,000? It seems like I would only have enough money for a few trades since I am possibly buying 100 shares of a stock if the price goes down far enough." – Paid-up subscriber James P.

Porter comment: James, I wish I could give you a "friendlier" answer (and so does my marketing department), but I have a form of Tourette's that causes me to give people my unvarnished opinion. I don't think anyone with less than $50,000 should be buying stocks, period.

That will surely upset a lot of people who will accuse me of being an elitist. But from what I've seen working with investors over many years is that almost everyone greatly overestimates their risk tolerance, and almost everyone ends up putting far too much capital in one or two favorites. That's a recipe that's guaranteed to cause huge losses sooner or later.

These bad habits seem to be even more pronounced in small-lot traders. To be reasonably diversified, you must have, at a minimum, some capital in stocks, bonds, cash, and precious metals. Assuming you're going to have a fairly ordinary allocation, you might have 40% in stocks, 30% in bonds, 10% in precious metals, and 20% in cash. That means you'd have $6,000 in stocks. I wouldn't recommend an equity portfolio with fewer than 12 positions... meaning you have $500 in each one. I don't see how you can responsibly handle 100-share options contracts in that kind of an account. I don't think it's even close.

That's the bad news. But here's the good news: Taking the time to build a $50,000 nest egg is difficult. It will require patience, discipline, and wisdom. Those are the same skills you'll have to acquire to be successful as an investor. In other words, don't think of the time you're spending to build a nest egg as what you have to do before you become an investor. It's all part of the same journey. You can (and should) use this time to paper trade your portfolio. You can learn a lot of good lessons this way... about the markets and about yourself.

Regards,

Porter Stansberry

Baltimore, Maryland

December 17, 2015

|