An Urgent Warning for Bond Investors

An urgent warning for bond investors... The worst trade in the history of the Treasury market... The 'Bond King' warns of panic and recommends gold... The news gets worse for SolarCity... The latest on Hershey... Porter reveals his first 'Magic Stock'...

![]() Insane central-bank policies have created unprecedented moves in the sovereign bond markets... and pushed yields to record lows around the world.

Insane central-bank policies have created unprecedented moves in the sovereign bond markets... and pushed yields to record lows around the world.

Regular Digest readers know that yields on the benchmark 10-year debt of major economies like Germany, Japan, and Switzerland are now negative for the first time in history...

And it may only be a matter of time before the global "reach for yield" pushes yields on U.S. Treasurys – the last so-called "safe haven" debt that still offers a positive nominal yield – near zero or below.

![]() But in the near term, Stansberry Short Report editor Jeff Clark says U.S. Treasury yields – particularly those of longer-term Treasury bonds – could move higher rather than lower. (Remember, bond prices and yields move inversely. When bond yields rise, bond prices fall, and vice versa.)

But in the near term, Stansberry Short Report editor Jeff Clark says U.S. Treasury yields – particularly those of longer-term Treasury bonds – could move higher rather than lower. (Remember, bond prices and yields move inversely. When bond yields rise, bond prices fall, and vice versa.)

Jeff notes 30-year "T-bonds" have rallied 10% since May... an extreme move in what's considered one of the world's most stable, safe investments. At the same time, he says the chart of long-term Treasurys is forming a concerning pattern. As he explained in this morning's edition of our free Growth Stock Wire e-letter...

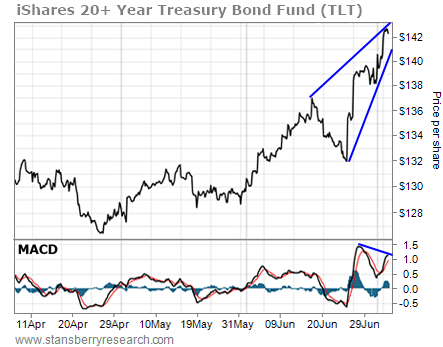

Take a look at this 60-minute chart of the iShares 20+ Year Treasury Bond Fund (TLT) – an exchange-traded fund that tracks the price of long-term T-bonds...

This chart is forming a bearish rising-wedge pattern with negative divergence on the moving average convergence divergence (MACD) momentum indicator. This type of pattern usually breaks to the downside.

![]() Jeff says there's still room for T-bonds to move higher over the next few days. He thinks TLT could run as high as $144 per share before peaking. But he says anyone who owns long-term T-bonds today could be taking a big risk...

Jeff says there's still room for T-bonds to move higher over the next few days. He thinks TLT could run as high as $144 per share before peaking. But he says anyone who owns long-term T-bonds today could be taking a big risk...

In this case, a breakdown could lead to a move for TLT all the way back to about $132 per share. That would essentially take back all of the gains in the Treasury bond market since the "Brexit" vote late last month...

This is a dangerous setup. After an 11% rally in just two months, the Treasury bond market is looking a little frothy. Investors buying T-bonds as a safe haven for their money today could regret it in a few weeks.

![]() As a trader, Jeff is more concerned with the near- and intermediate-term outlook. But several respected bond investors share his bearish view of Treasurys and other sovereign debt...

As a trader, Jeff is more concerned with the near- and intermediate-term outlook. But several respected bond investors share his bearish view of Treasurys and other sovereign debt...

In an interview yesterday, former "Bond King" Bill Gross – the most experienced fixed-income manager of the current generation – says government bonds aren't worth the risk today. As Bloomberg reported last night...

"The sovereign bonds are not up my alley," Gross, who built the world's biggest bond fund at Pacific Investment Management Co. and is now at Denver-based Janus Capital Group Inc., said... "It's too risky." Low yields mean bonds are especially vulnerable because a small increase can bring a large decline in price, he said.

Gross was referring to "duration risk." In short, this means longer-term debt is susceptible to surprisingly big losses from small increases in interest rates.

![]() Brilliant fixed-income manager Jeffrey Gundlach – considered by many to be the new Bond King – agrees. In an interview with news service Reuters yesterday, he singled out 10-year Treasurys in particular...

Brilliant fixed-income manager Jeffrey Gundlach – considered by many to be the new Bond King – agrees. In an interview with news service Reuters yesterday, he singled out 10-year Treasurys in particular...

You're seeing people who hated the 10-year [when it was yielding 2%] suddenly loving it at a 1.38%-1.39% revisit of the all-time-low closing yield. If you buy 10-year Treasuries now, I would say, it is a terrible trade location. It is the worst trade location in the history of the 10-year Treasury.

![]() While Gundlach doesn't like sovereign debt today, he is still incredibly bullish on gold.

While Gundlach doesn't like sovereign debt today, he is still incredibly bullish on gold.

He says both bullion and gold stocks are incredibly "attractive" today compared with expensive government bonds, and he believes troubles in Europe could send gold prices much higher from here. From the interview...

"Things are shaky and feeling dangerous... I am not selling gold."

Gundlach, who oversees $100 billion at Los Angeles-based DoubleLine, said gold is attractive against the backdrop of "a banking system in Europe, which is in a state of heading toward insolvency."

He was referring to Banca Monte dei Paschi di Siena, Italy's third largest bank, whose pile of bad debts and capital shortfalls are threatening contagion to other European Union nations. Gundlach also cited Deutsche Bank (DB), whose shares hit a new record low Wednesday and whose value has halved since the beginning of the year.

"Banks are dying and policymakers don't know what to do," Gundlach said. "Watch Deutsche Bank shares go to single digits and people will start to panic... you'll see someone say, 'Someone is going to have to do something'."

![]() Gundlach isn't the only notable name calling for higher gold prices today...

Gundlach isn't the only notable name calling for higher gold prices today...

ABN AMRO Bank currency and commodity analyst Georgette Boele – rated by Bloomberg as the most accurate gold forecaster over the past several years – believes the rally will continue.

Boele turned bearish when gold failed a "retest" of its highs in late 2012, just before prices plunged more than 40% over the next few years. She then turned bullish again for the first time early this year.

She now says gold will climb to new three-year highs above $1,425 over the next several months before a more meaningful pullback occurs.

As we noted yesterday, the biggest risk in gold today is not that you'll buy before a sharp correction... it's that you won't own enough.

![]() Switching gears, the news for beleaguered solar-panel installer SolarCity (SCTY) isn't getting any better.

Switching gears, the news for beleaguered solar-panel installer SolarCity (SCTY) isn't getting any better.

According to a report from news service Reuters, solar power will contribute more new electricity to the U.S. power grid than any other source of energy this year. Unfortunately for SolarCity, it won't come from do-it-yourself folks putting panels on their roofs. From the report...

The early solar industry was dominated by rooftop panels that powered individual homes and businesses. But such small-scale installations are expensive, requiring hefty incentives to make them attractive to homeowners.

Today, large systems that sell directly to utilities dominate. They are expected to account for more than 70% of new solar added to the grid this year, according to industry research firm GTM Research.

So-called "Big Solar" is yet another serious threat to SolarCity's survival. After all, if large-scale solar fields are cheaper, and don't require government incentives... why should the government keep handing out free cash to middlemen like SolarCity?

![]() According to GTM Research, unsubsidized power from "Big Solar" costs $50-$70 per megawatt hour (MWh), compared with $52-$78 per MWh for natural gas power plants. However, rooftop solar panels like the ones SolarCity sells cost between $184-$300 per MWh before subsidies.

According to GTM Research, unsubsidized power from "Big Solar" costs $50-$70 per megawatt hour (MWh), compared with $52-$78 per MWh for natural gas power plants. However, rooftop solar panels like the ones SolarCity sells cost between $184-$300 per MWh before subsidies.

In short, SolarCity is providing an outdated product... at a price point more than three times higher than what the market will pay. Or as Porter and his research team wrote in the June issue of Stansberry's Investment Advisory, "SolarCity is running out of money, and it's running out of people dumb enough to give it more."

![]() Finally, we note longtime Stansberry's Investment Advisory holding Hershey (HSY) has rejected the $23 billion takeover bid from Mondelez International (MDLZ) – the maker of Oreo cookies and Cadbury chocolate.

Finally, we note longtime Stansberry's Investment Advisory holding Hershey (HSY) has rejected the $23 billion takeover bid from Mondelez International (MDLZ) – the maker of Oreo cookies and Cadbury chocolate.

However, Hershey shares remain well above the offer's value of $107 per share... suggesting investors expect a new proposal.

As we mentioned last week, the Hershey Trust controls 80% of the company's voting rights. This means it would have to approve of any sale.

But there's a little more to the story. As Porter explained when he originally recommended shares in Stansberry's Investment Advisory...

Back in 2002, after listening to a bunch of investment bankers who were eager for deal fees, the Trust decided it needed to "diversify" its endowment beyond the shares of only one stock, Hershey Co. When you've got a business this good, anything else you buy is bound to be a disappointment. Clearly the folks running the Trust were about to make a big mistake.

Luckily, the decision to sell so enraged the public in Pennsylvania, the state legislature passed a law requiring the Trust to give advanced notice of any sale or merger that would result in the Hershey Trust no longer having complete voting control over Hershey Co. The law further provides specific authority for the attorney general to stop any transaction that isn't necessary to the future economic viability of Hershey Co.

For all practical purposes then, the Trust can never sell its shares, which means Hershey will in all likelihood remain an independent company forever – which suits our purposes exactly.

But some analysts are still holding out hope that the company's famous defenses are lowered and a deal may be approved...

![]() Reuters reported last week that the Pennsylvania attorney general's office is investigating the Trust...

Reuters reported last week that the Pennsylvania attorney general's office is investigating the Trust...

The AG's office has called for the resignation of three of its longest-tenured employees. Separately, this year, the Trust fired its executive vice president, after he pled guilty to wire fraud associated with campaign contributions.

At the same time, the state's current attorney, Kathleen Kane, has been indicted. She is expected to go on trial next month for leaking e-mails to a reporter. According to the New York Times, her law license has already been suspended.

We can't know for certain how this will all turn out. But we're skeptical a deal will be done.

In the meantime, Stansberry's Investment Advisory subscribers have more than tripled their money in Hershey... a position that Porter predicted would turn out to be the single best stock recommendation of his career.

![]() Why was Porter so sure Hershey would be a winner? Because it is a high-quality company, and one of just a small number of publicly traded companies that qualify as "capital efficient."

Why was Porter so sure Hershey would be a winner? Because it is a high-quality company, and one of just a small number of publicly traded companies that qualify as "capital efficient."

As the name suggests, these rare stocks have low capital requirements. They're able to increase their cash profits steadily without having to put a lot of new money back into the business.

This allows them to produce extremely high and consistent rates of return on the capital they hold... and return more and more cash to shareholders every year.

In short, owning capital-efficient stocks like Hershey is the perhaps the surest and safest way to earn a literal fortune in the stock market.

![]() But Porter believes he has found an even better opportunity today...

But Porter believes he has found an even better opportunity today...

Over the past few years, he and his research team have refined this strategy. They've discovered a short list of additional characteristics that – when combined with a high level of capital efficiency – lead to even better returns.

They call the stocks that meet these strict criteria "Magic Stocks." These are stocks you can safely put a significant portion of money into and compound your wealth at high rates of return for decades... no matter what happens to the economy, the U.S. dollar, or the stock market.

There's just one catch... It's extremely rare to find a stock that meets all of these criteria at any time. In fact, most of the time, these opportunities simply don't exist.

But as of last week, that's no longer the case.

Last Friday evening, Porter officially revealed his first Magic Stock recommendation. He's convinced it is the absolute best – and safest – opportunity for new money today. Click here for all the details.

![]() New 52-week highs (as of 7/6/16): Automatic Data Processing (ADP), AutoZone (AZO), Central Fund of Canada (CEF), Ciner Resources (CINR), Deutsche Bank Gold Double Long Fund (DGP), Western Asset Emerging Markets Debt Fund (ESD), Franco-Nevada (FNV), Fidelity Select Medical Equipment and Systems Fund (FSMEX), VanEck Vectors Junior Gold Miners Fund (GDXJ), SPDR Gold Trust (GLD), Johnson & Johnson (JNJ), Nuveen Preferred Securities Income Fund (JPS), Kaminak Gold (KAM.V), Mid-America Apartment Communities (MAA), Medtronic (MDT), Altria (MO), Nuveen AMT-Free Municipal Income Fund (NEA), Newmont Mining (NEM), NovaGold Resources (NG), New Gold (NGD), OceanaGold (OGC.TO), Osisko Gold Royalties (OR.TO), ETFS Physical Platinum Shares Fund (PPLT), Pretium Resources (PVG), Regions Financial – Series B (RF-PB), Seabridge Gold (SA), SEMAFO (SMF.TO), Silver Standard Resources (SSRI), Sysco (SYY), Vanguard Inflation-Protected Securities Fund (VIPSX), Wells Fargo – Series W (WFC-PW), ExxonMobil (XOM), and PIMCO 25+ Year Zero Coupon U.S. Treasury Index Fund (ZROZ).

New 52-week highs (as of 7/6/16): Automatic Data Processing (ADP), AutoZone (AZO), Central Fund of Canada (CEF), Ciner Resources (CINR), Deutsche Bank Gold Double Long Fund (DGP), Western Asset Emerging Markets Debt Fund (ESD), Franco-Nevada (FNV), Fidelity Select Medical Equipment and Systems Fund (FSMEX), VanEck Vectors Junior Gold Miners Fund (GDXJ), SPDR Gold Trust (GLD), Johnson & Johnson (JNJ), Nuveen Preferred Securities Income Fund (JPS), Kaminak Gold (KAM.V), Mid-America Apartment Communities (MAA), Medtronic (MDT), Altria (MO), Nuveen AMT-Free Municipal Income Fund (NEA), Newmont Mining (NEM), NovaGold Resources (NG), New Gold (NGD), OceanaGold (OGC.TO), Osisko Gold Royalties (OR.TO), ETFS Physical Platinum Shares Fund (PPLT), Pretium Resources (PVG), Regions Financial – Series B (RF-PB), Seabridge Gold (SA), SEMAFO (SMF.TO), Silver Standard Resources (SSRI), Sysco (SYY), Vanguard Inflation-Protected Securities Fund (VIPSX), Wells Fargo – Series W (WFC-PW), ExxonMobil (XOM), and PIMCO 25+ Year Zero Coupon U.S. Treasury Index Fund (ZROZ).

![]() In today's mailbag, subscribers weigh in on our "trading for income" strategies... the "Brexit"... and the latest from best-selling author and Digest contributing editor P.J. O'Rourke. Send your questions, comments, and complaints to feedback@stansberryresearch.com.

In today's mailbag, subscribers weigh in on our "trading for income" strategies... the "Brexit"... and the latest from best-selling author and Digest contributing editor P.J. O'Rourke. Send your questions, comments, and complaints to feedback@stansberryresearch.com.

![]() "Last year I quit my regular job at age 58 and began 'Trading for Income' for a living. I started with my own account and now I also manage a family member's account. I spent a full year studying the work of DailyWealth Trader, Doc Eifrig and Jeff Clark learning about selling naked puts. I also follow Steve Sjuggerud, converting his recommendations into put trades. Last year I had an 87% winning trade rate with an ROI of 80%. After six months this year I have an unbelievable 98% winning percentage, 212 of 216 closed trades were profitable. My return on margin is 47% so far, 94% annualized.

"Last year I quit my regular job at age 58 and began 'Trading for Income' for a living. I started with my own account and now I also manage a family member's account. I spent a full year studying the work of DailyWealth Trader, Doc Eifrig and Jeff Clark learning about selling naked puts. I also follow Steve Sjuggerud, converting his recommendations into put trades. Last year I had an 87% winning trade rate with an ROI of 80%. After six months this year I have an unbelievable 98% winning percentage, 212 of 216 closed trades were profitable. My return on margin is 47% so far, 94% annualized.

"After trying everything else, and losing money at it, I am now convinced there is nothing else I can do better than sell naked puts. Well, with maybe one exception, I added [Stansberry] Gold Investor to my membership. Nice hedge to protect my core account so I can keep selling puts... even selling puts on gold miners as recommended in DWT. I changed my life with the help of Stansberry Research... 'putting' it all together... thank you!" – Paid-up subscriber Bob B.

![]() "Looks like the British are winning the race to the bottom (devaluing the pound) and all it took was a 'Brexit.' Now they can pay back their creditors... I'm glad I don't own any of their sovereign debt." – Paid-up subscriber Mike C.

"Looks like the British are winning the race to the bottom (devaluing the pound) and all it took was a 'Brexit.' Now they can pay back their creditors... I'm glad I don't own any of their sovereign debt." – Paid-up subscriber Mike C.

![]() "I love your article about the iPhone. Young people will sit together using their phones to communicate without ever talking. I use my phone for everything. Text, talk, pics videos, price compare, shop, look things up, check on kids, etc. the only thing I wish I could do on it is buy and sell stocks and download seeing things for my sewing machine. Hint hint, Apple. Yes, I'm in my 60's." – Paid-up subscriber T.J.

"I love your article about the iPhone. Young people will sit together using their phones to communicate without ever talking. I use my phone for everything. Text, talk, pics videos, price compare, shop, look things up, check on kids, etc. the only thing I wish I could do on it is buy and sell stocks and download seeing things for my sewing machine. Hint hint, Apple. Yes, I'm in my 60's." – Paid-up subscriber T.J.

Regards,

Justin Brill

Baltimore, Maryland

July 7, 2016

|