Carnage is here...

Carnage is here... Now what?... The '$64,000 question'... What you should know about 'junk' bonds now...

![]() In today's Friday Digest... we'll discuss opportunities that are emerging from the collapse of oil prices and the virtual shutdown of the corporate-bond market.

In today's Friday Digest... we'll discuss opportunities that are emerging from the collapse of oil prices and the virtual shutdown of the corporate-bond market.

I (Porter) have been warning about the inevitability of sub-$40 oil since 2011, and I've been predicting a big collapse in high-yield corporate bonds, so none of the carnage below should have hurt your wealth.

That is, none of these things should have hurt you on the way down. The question is, will you be able to capitalize on these opportunities on the way back up?

![]() Let's start with master limited partnerships (or "MLPs"). As some of you probably know, the capital-intensive and highly regulated parts of our country's energy infrastructure (mostly pipelines) are typically held by MLPs.

Let's start with master limited partnerships (or "MLPs"). As some of you probably know, the capital-intensive and highly regulated parts of our country's energy infrastructure (mostly pipelines) are typically held by MLPs.

These are essentially asset-holding companies formed to help offset the massive capital costs of this infrastructure. To encourage the development of this kind of asset base (which aids all kinds of other industrial businesses), Congress allows these firms to operate without paying income taxes, as long as they operate as "flow-through" entities. In short, they have to pay out 90% of their cash flows every year to their unitholders.

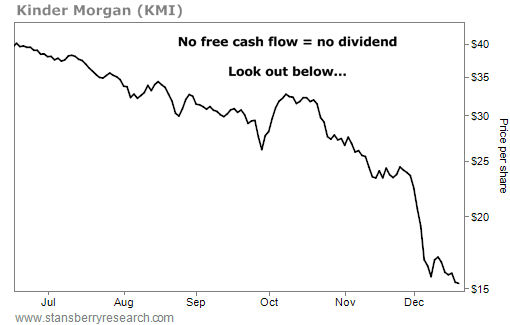

That makes these entities popular with retired investors and other folks who value yields above total returns. The "granddaddy" of MLPs is Richard Kinder's Kinder Morgan. Ironically, it isn't actually an MLP anymore, as the partnership was folded back into Kinder Morgan the corporation (KMI).

Two charts tell the story. First, here's Kinder Morgan over the past six months. It's down more than 60%...

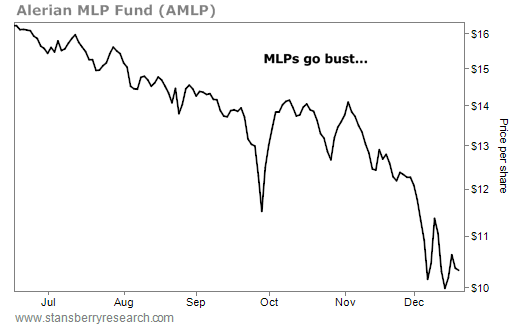

And here's a broader look at the entire MLP sector. This is the Alerian MLP Fund (AMLP), an exchange-traded fund that owns a huge basket of these types of partnerships. (Its three largest holdings are Enterprise Products Partners, Magellan Midstream Partners, and MarkWest Energy Partners.)

![]() George Soros was one of the first analysts anywhere to describe the inevitable boom-and-bust cycle of tax-favored corporate structures like MLPs and real estate investment trusts (or "REITs").

George Soros was one of the first analysts anywhere to describe the inevitable boom-and-bust cycle of tax-favored corporate structures like MLPs and real estate investment trusts (or "REITs").

Soros predicted in a famous report written in the 1960s that because these firms are required to distribute virtually all of their cash flows, they would likely rely heavily on the debt and equity markets to fund any growth. Thus, in bear markets when borrowing costs rise sharply, they might be forced to issue new equity at a low price and/or greatly reduce their dividends.

![]() Let me show you how this works. I'll use Enterprise Products Partners (EPD) as an example. The partnership is down 34% year to date. Over the last three years, the partnership generated $10.9 billion in cash flow from a tangible asset base worth around $40 billion – mostly oil and gas pipelines. These are dependable, generally low-yielding assets. Return on assets is only 4.5% a year. Investors wouldn't be interested in this firm if it didn't grow – a lot.

Let me show you how this works. I'll use Enterprise Products Partners (EPD) as an example. The partnership is down 34% year to date. Over the last three years, the partnership generated $10.9 billion in cash flow from a tangible asset base worth around $40 billion – mostly oil and gas pipelines. These are dependable, generally low-yielding assets. Return on assets is only 4.5% a year. Investors wouldn't be interested in this firm if it didn't grow – a lot.

To spice things up, Enterprise Products continues to spend billions on new pipelines. In total, the firm spent $9.9 billion in capital expenditures over the last three years and another $4.7 billion on investments. That's a lot more money than it made. And that's not counting the $7.2 billion it paid out in dividends!

How did the firm manage to spend nearly $15 billion on capital expenditures and investments in the last three years? By borrowing huge sums of capital, of course. Enterprise Products borrowed $6.5 billion and raised another $4 billion in new equity.

![]() But with yields on corporate debt soaring, that source of capital is unavailable for now. How will the firm maintain its dividend if it must begin to repay debt out of cash flows? How will it grow without ongoing access to large amounts of cheap capital? It won't. This business model doesn't work without lots of cheap capital.

But with yields on corporate debt soaring, that source of capital is unavailable for now. How will the firm maintain its dividend if it must begin to repay debt out of cash flows? How will it grow without ongoing access to large amounts of cheap capital? It won't. This business model doesn't work without lots of cheap capital.

Thus, the $64,000 question is: How cheap will these assets become before they're safe to buy again? Sooner or later, the credit markets will reopen. When they do, and these companies are able to grow again, they will soar. Figuring out when the next up-cycle is going to begin will be the focus of a lot of our work in Stansberry Data, which is part of our new program we've named "The Porter Group." (You can learn more about The Porter Group right here.)

![]() Lots of other oil-related businesses are heading for trouble, too.

Lots of other oil-related businesses are heading for trouble, too.

Most of the onshore oil and gas exploration and production (E&P) firms have been spending far more on capital investments than they're able to make in cash flow. They've been plugging the gap for years with cheap capital from the bond market. That gravy train is over.

Even huge firms like Marathon Oil (MRO) and Chevron (CVX) will be hit next. Both stocks will almost certainly cut their dividends, as they're no longer able to earn enough cash to support their payouts. Marathon, for example, has raised $1.5 billion in new equity only to see more than $1 billion of that capital go back out the door immediately as a dividend.

What's the point of buying stock in a company that's going to cut you a check, giving you your money back in a taxed dividend? Again, we will be following these firms closely in Stansberry Data. For now, our best advice is to stand clear.

![]() We've also been warning about high-yield bonds for years. But there's one part of the high-yield bond market that looks interesting enough for us to start following closely: closed-end bond funds. Please understand, I'm not suggesting you go out and buy high-yield closed-end bond funds today. But it's time to start watching them closely.

We've also been warning about high-yield bonds for years. But there's one part of the high-yield bond market that looks interesting enough for us to start following closely: closed-end bond funds. Please understand, I'm not suggesting you go out and buy high-yield closed-end bond funds today. But it's time to start watching them closely.

Unlike other bond funds, closed-end bond funds don't have to worry about redemptions. They are relatively fixed pools of capital that trade just like a stock. You can either buy or sell the pool of capital. The price of the pool depends on investors' appetites for such bonds. Sometimes, the fund will trade at a premium... and when times are tough, these pools of capital can trade at a big discount.

![]() Here's one example... the Pioneer Diversified High Income Trust (HNW) is a $200 million or so pile of bonds. It employs a bit of leverage (29%) to create a more attractive yield. The current yield is almost 10%. That's great, considering that more than 60% of these bonds are investment-grade and only about 20% are junk bonds.

Here's one example... the Pioneer Diversified High Income Trust (HNW) is a $200 million or so pile of bonds. It employs a bit of leverage (29%) to create a more attractive yield. The current yield is almost 10%. That's great, considering that more than 60% of these bonds are investment-grade and only about 20% are junk bonds.

This relatively high-quality pile of bonds has only seen a modest 3% decline in the value of its assets. But investors, running scared, have been selling shares in the trust hand over fist. As a result, this closed-end fund is now trading at a massive 17% discount to its net asset value (or "NAV").

Buying these trusts when they're trading at a big discount (20%-plus) is a great way to "dip your toe" into the distressed-debt market. The discount to NAV gives you a wide margin of safety.

However, I think we're still in the early days of what's going to be a massive transfer of wealth. The default rate on junk bonds has a long way to go before it reaches the peak of 12%-15% a year. We'll get there, but it's going to take a while.

In short, there's no hurry to buy a big pile of bonds yet. But it's something we're going to begin tracking carefully so that when the time comes, we'll know exactly what to recommend. Again, you're welcome to follow along – just join The Porter Group. Learn more here.

![]() On a different note... we have a few spots still open for our next trip to Rancho Santana in Nicaragua. We're hosting a small group down there January 23-27. Unfortunately, I will not be able to attend this time, due to a late scheduling conflict. But I invite you to join Doc Eifrig and some of our friends in my place.

On a different note... we have a few spots still open for our next trip to Rancho Santana in Nicaragua. We're hosting a small group down there January 23-27. Unfortunately, I will not be able to attend this time, due to a late scheduling conflict. But I invite you to join Doc Eifrig and some of our friends in my place.

It's an ideal location to get some money offshore... and it's a great place to relax, play golf, surf, and enjoy life with like-minded friends. And I'm not the only one who thinks so... The renowned New York Times travel section just featured it this month, joining the long list of major travel and destination publications – including Forbes, Fortune, Travel + Leisure, and Food & Wine magazine – to do so.

As I mentioned last time, if you're going to build a second home anywhere in the world, you shouldn't do it until you've compared that opportunity with Rancho Santana. I'm confident you will get far more for your money, see far more appreciation, have far more asset protection, and enjoy being in this community more than you will anywhere else in the world.

Still, I know that no matter what I tell you about "The Ranch," you'll never really understand unless you see it for yourself. So if you're in a position to take advantage of this opportunity, I urge you to do two things today...

First, go back and read what I wrote in the October 16 Digest. Then contact Rancho Santana Director of Sales Marc Brown at marcb@ranchosantana.com or (530) 563-8558, and plan to join us next month to experience it for yourself.

![]() Finally, a personal note. Today is my 43rd birthday. I'm old enough now that I don't take birthdays for granted. I'm very grateful to be alive. And I'm even more grateful to share my life with a wonderful family, with dozens of great friends, hundreds of business colleagues, and hundreds of thousands of dear subscribers.

Finally, a personal note. Today is my 43rd birthday. I'm old enough now that I don't take birthdays for granted. I'm very grateful to be alive. And I'm even more grateful to share my life with a wonderful family, with dozens of great friends, hundreds of business colleagues, and hundreds of thousands of dear subscribers.

I've spent 20 years building this business... and building my life.

I sit here today at my desk with a profound sense of gratitude. I just never dreamed life could be so sweet. So thank you – all of you.

I'll spend the next two weeks with my family. We will head to our mountain lodge (Twin Valley Lodge – aptly named because my wife has an identical twin) next week to celebrate Christmas. Hopefully, there will be a bit of snow. Either way, I'm sure there will be a gigantic Christmas tree. I don't believe in moderation when it comes to Christmas. My children, Traveler (8) and Seaton (4), still fully believe in Santa, so our house will be filled with wonder and joy. And I can't wait.

After Christmas, we'll fly down to Chub Cay in the Bahamas. My sister and her family are going to join us for a week of fishing and snorkeling around New Year's.

And my mistress is going to join us, too. She's the other love of my life. (I, of course, am referring to my boat, Two Suns.)

Whatever your plans for the holidays, I hope you will put all of your thoughts about money and finance away for a few days. What's money compared with the love of your family and your friends? And how important are your finances compared with the precious time you have to enjoy life?

Don't worry, I won't become a philosopher.

As soon as the New Year is passed, you'll find me back at my post – writing about the grubby world of the money changers.

I'm sure that 2016 is going to be a challenging year for most investors. It's our mission to make sure that you're able to navigate those choppy waters.

![]() New 52-week highs (as of 12/17/15): Becton Dickinson (BDX).

New 52-week highs (as of 12/17/15): Becton Dickinson (BDX).

![]() Did you enjoy the five-part Digest series? Please send a quick e-mail to feedback@stansberryresearch.com to let me know what you thought. I can't respond to each e-mail I receive, but I read every one.

Did you enjoy the five-part Digest series? Please send a quick e-mail to feedback@stansberryresearch.com to let me know what you thought. I can't respond to each e-mail I receive, but I read every one.

![]() "Porter, I have been using options for a long time. Yours and Dr Eifrig's explanations are the best I have ever seen. That plus the way to assess stocks to use options on in conjunction with the VIX is great. I have been experimenting using a put sell with a call buy and the opposite. A paper trade selling JNJ $105 calls and buying $102 puts when it closed outside the upper Bollinger band the other day is doing very well. I agree that I will probably start using option for trading exclusively." – Paid-up subscriber William LePage

"Porter, I have been using options for a long time. Yours and Dr Eifrig's explanations are the best I have ever seen. That plus the way to assess stocks to use options on in conjunction with the VIX is great. I have been experimenting using a put sell with a call buy and the opposite. A paper trade selling JNJ $105 calls and buying $102 puts when it closed outside the upper Bollinger band the other day is doing very well. I agree that I will probably start using option for trading exclusively." – Paid-up subscriber William LePage

Happy holidays,

Porter Stansberry

Baltimore, Maryland

December 18, 2015

P.S. We are going to send you a series of "best of" Digests over the next several days. They will also feature some special offers... I hope you'll find something you want to buy!

|