Do I Sound Like a Crazy Person?

Do I sound like a crazy person?... Bet you can't guess the 10-year return of the world's three biggest banks... Normalcy bias in action... A Goldman executive's gold mine... Our plan... Meeting on Wednesday night...

![]() As you'll recall... I (Porter) told you last Friday about the "Metropolitan Plan."

As you'll recall... I (Porter) told you last Friday about the "Metropolitan Plan."

That's my name for the working plan to swap out the Federal Reserve's paper assets for gold... a strategy that might be used in the future to stop a global run on the dollar.

Why would a former senior policy official even be working on such a thing? Why would major hedge-fund managers and investment banks be buying gold and gold stocks? Why would gun sales continue to increase in America, year after year? What's driving these fears and the growing sense that something has gone very, very wrong with our economic system, which seems to only serve the needs of the very rich?

![]() As you go about your everyday life, it's easy to forget how big the economic problems we face really are... and how desperate our political leaders have become to safeguard the existing system.

As you go about your everyday life, it's easy to forget how big the economic problems we face really are... and how desperate our political leaders have become to safeguard the existing system.

That's because of human psychology. It's called the "normalcy bias." It explains why, if you don't heat up the water too fast, the "frog" never jumps out of the pot before it starts to boil. People (the frogs) have a hard time believing that tomorrow won't be a lot like today. It can be almost impossible to open your mind enough to think about how the world might look a year from now... or five years from now... if there's a serious economic crisis.

![]() That's what I believe is going to happen. You've seen me write about the problems I see in the world economy over the past year or so. I've described the potential for $1.7 trillion in corporate-bond defaults, a credit crisis I've said would be "the largest legal transfer of wealth in history."

That's what I believe is going to happen. You've seen me write about the problems I see in the world economy over the past year or so. I've described the potential for $1.7 trillion in corporate-bond defaults, a credit crisis I've said would be "the largest legal transfer of wealth in history."

If you don't agree with me, then all of these warnings might make me sound like a crazy person. I probably sound crazy to a lot of people... at first. But I put the bug in their ear. Slowly, they start seeing what's happening. It takes time. But I believe, more and more, you're starting to see these things for yourself. It's getting harder to believe that everything is fine.

Meanwhile, I don't advocate selling everything you own and moving to New Zealand. Nor do I even recommend selling all of your stocks. I am telling you: Keep your head up and your mind open to the risks. What's about to happen isn't just a normal market correction or even a bad bear market. What's about to happen is a once-in-a-century debt-default cycle that could destroy the world's existing paper-money standard.

Think that's nuts? OK, maybe it is. But take a minute and look at this chart...

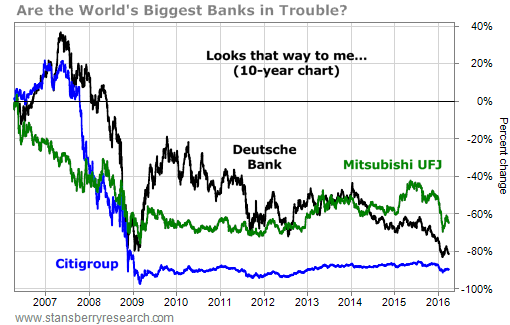

![]() This chart isn't hard to figure out. It simply compares the largest, most systematically important banks in the world: Mitsubishi UFJ (MTU), Deutsche Bank (DB), and Citigroup (C). Their share prices are down 72%, 83%, and 90% over the past 10 years.

This chart isn't hard to figure out. It simply compares the largest, most systematically important banks in the world: Mitsubishi UFJ (MTU), Deutsche Bank (DB), and Citigroup (C). Their share prices are down 72%, 83%, and 90% over the past 10 years.

How is that possible?

![]() I'd like for you to ask yourself two simple questions: First, if you believe that everything in the world's economy is basically fine and operating normally... how could the three most important banks in the world all be falling apart? Ask a reasonably well-read and knowledgeable person – like your broker, or the friend you always talk with about investments – what the 10-year return has been on the three largest banks in free-market capitalism. I guarantee they won't come anywhere close to the correct answer.

I'd like for you to ask yourself two simple questions: First, if you believe that everything in the world's economy is basically fine and operating normally... how could the three most important banks in the world all be falling apart? Ask a reasonably well-read and knowledgeable person – like your broker, or the friend you always talk with about investments – what the 10-year return has been on the three largest banks in free-market capitalism. I guarantee they won't come anywhere close to the correct answer.

That's normalcy bias in action. People constantly disregard any facts or data points that don't match their underlying assumptions, especially when those data points would disrupt a long-held belief or worldview. Let me say this as plainly as I can: If our global financial system were working normally, the returns on these major, immensely important piles of capital would at least be positive.

![]() Here's the second question I want you to think about carefully: How far will these banks have to fall before you think seriously about taking all of your savings out of the banking system? If these banks fail, the system will fail. And how much faster will you make the decision to pull your cash if these banks begin charging you to hold your cash in their bankrupt vaults? My bet is when you start thinking about these questions, you'll suddenly realize why a senior policymaker is working on the Metropolitan Plan.

Here's the second question I want you to think about carefully: How far will these banks have to fall before you think seriously about taking all of your savings out of the banking system? If these banks fail, the system will fail. And how much faster will you make the decision to pull your cash if these banks begin charging you to hold your cash in their bankrupt vaults? My bet is when you start thinking about these questions, you'll suddenly realize why a senior policymaker is working on the Metropolitan Plan.

![]() Now... let me back up for a second.

Now... let me back up for a second.

The reason these banks have struggled for an entire decade isn't hard to understand. You don't need to be an economist. If you have been alive for the last 20 years, you know what happened...

A tremendous amount of credit was created out of thin air around the world. You can measure it in plenty of ways: total debt to GDP, the size of financial earnings as a percentage of GDP, debt service as a percentage of household income. I could bury you in numbers... but they all mean the same thing.

For an entire generation, most people in the world's major, wealthiest economies consumed far more than they produced, resulting in a debt bubble of mind-boggling, epic proportions.

![]() This process of unlimited credit creation is hitting the wall of economic reality. Wages haven't grown. Productivity hasn't grown as fast. And various economic tricks to extend even more credit – like increasing international trade, manipulating currencies, and printing money – are running out of steam. Thus, this massive, global bubble is beginning to deflate. Before that can happen, though... credit has to stop expanding. That'll be the first sign that the real collapse is happening.

This process of unlimited credit creation is hitting the wall of economic reality. Wages haven't grown. Productivity hasn't grown as fast. And various economic tricks to extend even more credit – like increasing international trade, manipulating currencies, and printing money – are running out of steam. Thus, this massive, global bubble is beginning to deflate. Before that can happen, though... credit has to stop expanding. That'll be the first sign that the real collapse is happening.

![]() As you'll recall, a lot of the credit created in our economy relied on ever-increasing housing prices. Fannie Mae and Freddie Mac were the primary guarantors of the bubble in the U.S. – a total of $5 trillion in credit was created in about a decade on just two balance sheets.

As you'll recall, a lot of the credit created in our economy relied on ever-increasing housing prices. Fannie Mae and Freddie Mac were the primary guarantors of the bubble in the U.S. – a total of $5 trillion in credit was created in about a decade on just two balance sheets.

Lately, though, credit has only been expanding in far less secure ways. Globally, credit has been expanding by lending to corrupt emerging markets (like China, Brazil, and Russia). In the U.S., credit has been piled onto the backs of college students and subprime auto-lending (nuts!). Sovereign debt around the world has technically been expanding, too... but as you know, that's a rigged game where the national treasuries offer bonds and the central banks buy them with newly printed money.

![]() And so... the world economy has moved from making loans on good collateral (sound residential mortgages) to lending billions to corrupt dictatorships, unemployed college students, and subprime auto-buyers. Oh, we're also growing credit by printing money. No wonder those major banks are falling apart. I'd be willing to bet a huge amount of money that the folks auditing the banks' loan books don't keep their cash in those banks.

And so... the world economy has moved from making loans on good collateral (sound residential mortgages) to lending billions to corrupt dictatorships, unemployed college students, and subprime auto-buyers. Oh, we're also growing credit by printing money. No wonder those major banks are falling apart. I'd be willing to bet a huge amount of money that the folks auditing the banks' loan books don't keep their cash in those banks.

![]() In various ways, all of these bad loans end up on the balance sheets of the world's biggest banks. The means of transmission are varied: The loans are securitized, they're sold, they're "swapped." These loans and their underlying collateral end up in a myriad of different derivative products. In short, they're everywhere. These loans are at the heart of the financial system we use to drive the world economy. And today, they've transformed the global economy into a mountain of hugely inflated value... a giant pile of steaming, worthless garbage.

In various ways, all of these bad loans end up on the balance sheets of the world's biggest banks. The means of transmission are varied: The loans are securitized, they're sold, they're "swapped." These loans and their underlying collateral end up in a myriad of different derivative products. In short, they're everywhere. These loans are at the heart of the financial system we use to drive the world economy. And today, they've transformed the global economy into a mountain of hugely inflated value... a giant pile of steaming, worthless garbage.

So what happens when suddenly, for no discernable reason at all, everyone decides to stop pretending otherwise?

![]() When that happens, the authorities will have three choices. They can...

When that happens, the authorities will have three choices. They can...

1. Inflate away the bad debt by devaluing the currency and propping up the banking system with newly printed money and trade surpluses. That's the International Monetary Fund's playbook. It's what Japan has tried to do for 30 years. And it seems like that's what America and Europe are going to try now, too. Or...

2. Write off the bad loans, shut down the bad banks, and suffer a severe (but short) crisis. That's the sound-money option. (Nobody does that anymore, because depositors in the bad banks would lose everything... and they vote.) Or...

3. Simply repudiate a lot of the debt and stiff the creditors, like Russia did in 1998 and Iceland did in 2008. (That option works best if you have foreign creditors... like Argentina did in 2002.)

![]() Nobody knows what's going to happen when most of the world's wealthiest and largest economies try option No. 1 at the same time. But let me hazard a guess: The outcome isn't going to be good for people who saved all of their money in paper currencies.

Nobody knows what's going to happen when most of the world's wealthiest and largest economies try option No. 1 at the same time. But let me hazard a guess: The outcome isn't going to be good for people who saved all of their money in paper currencies.

![]() And that brings us to gold. As you may know, gold had its best quarter since 1986. The metal's spot price was up more than 16% in the first quarter of 2016. Yes, this could be simply a random price move. But I don't think so.

And that brings us to gold. As you may know, gold had its best quarter since 1986. The metal's spot price was up more than 16% in the first quarter of 2016. Yes, this could be simply a random price move. But I don't think so.

My friend Dr. Steve Sjuggerud has done careful studies of what moves of this magnitude mean in the market for gold. His research analyst Brett Eversole published the results of one of their most recent studies in the March 8 edition of our company's free DailyWealth e-letter. Their work shows that given gold's recent price moves, they would expect gold to move 19% more over the next 12 months.

Keep in mind, that's based on the last 40 years of trading during normal market conditions... not a period that features a global financial crisis like the kind I expect. So it's a good time to buy gold, even if the crisis we expect doesn't materialize.

![]() Gold does best when real interest rates are negative. The reason is easy to understand: Gold is the ultimate hedge against the loss of purchasing power in paper currencies. If governments can't offer a real rate of return for holding their bonds, then investors aren't being protected against inflation. And as a result, they flee to gold.

Gold does best when real interest rates are negative. The reason is easy to understand: Gold is the ultimate hedge against the loss of purchasing power in paper currencies. If governments can't offer a real rate of return for holding their bonds, then investors aren't being protected against inflation. And as a result, they flee to gold.

Negative interest rates would greatly exacerbate this logical market preference... and that's exactly why gold has been soaring lately. As Steve explained in the March 15 DailyWealth...

When both gold and paper money pay zero-percent interest, investors prefer gold over paper. Right now, paper money is paying you zero [or even less]... It's time for people to own gold.

![]() These are just a few of the core reasons we've organized a meeting for investors on Wednesday night. I want to make sure that you understand all of these fundamental and technical factors. And I want to make sure you understand the big risks that I see... risks that could drive gold much higher than anyone expects right now.

These are just a few of the core reasons we've organized a meeting for investors on Wednesday night. I want to make sure that you understand all of these fundamental and technical factors. And I want to make sure you understand the big risks that I see... risks that could drive gold much higher than anyone expects right now.

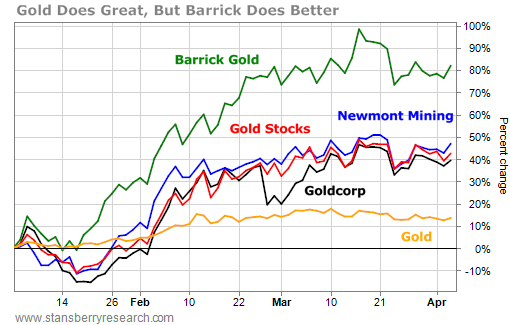

I also want to show you what our research group can do to help make your gold investments far better than average. For example, we know that out of all of the large gold producers, Barrick Gold (ABX) is likely to perform the best – far better than the price of gold and far better than the Market Vectors Gold Miners Fund (GDX).

![]() Just consider the last three months. Gold is up 13%. That's one of its biggest three-month moves ever. If you bought the metal in January, you've done well. If you bought any of the largest gold producers, you've done even better: Goldcorp (GG) is up nearly 40%, and Newmont Mining (NEM) is up more than 45%. Or if you simply bought GDX, you've done well, too. It's up 43%.

Just consider the last three months. Gold is up 13%. That's one of its biggest three-month moves ever. If you bought the metal in January, you've done well. If you bought any of the largest gold producers, you've done even better: Goldcorp (GG) is up nearly 40%, and Newmont Mining (NEM) is up more than 45%. Or if you simply bought GDX, you've done well, too. It's up 43%.

You don't need our specific stock advice to do well in gold over the next several years. The metal is going up, and it's going to lift just about every gold producer and gold exchange-traded fund along with it.

![]() On the other hand, you might want our best gold coverage because it can make a huge difference in your returns. Our top large-cap gold recommendation is Barrick. A former president of the investment bank Goldman Sachs, John Thornton, has been the company's executive chairman since late 2012. He has put in place a far better management team, and he has been streamlining the company's asset base while reducing debt. There's a big story here, one that few investors know anything about.

On the other hand, you might want our best gold coverage because it can make a huge difference in your returns. Our top large-cap gold recommendation is Barrick. A former president of the investment bank Goldman Sachs, John Thornton, has been the company's executive chairman since late 2012. He has put in place a far better management team, and he has been streamlining the company's asset base while reducing debt. There's a big story here, one that few investors know anything about.

![]() Barrick's former management team made a series of big mistakes during the last run up in the price of gold (from 2005 to 2011). In total, it spent $21 billion on acquisitions during this period. These deals were so bad that they led to $28 billion in write-offs.

Barrick's former management team made a series of big mistakes during the last run up in the price of gold (from 2005 to 2011). In total, it spent $21 billion on acquisitions during this period. These deals were so bad that they led to $28 billion in write-offs.

The worst deal was paying $7.5 billion for copper miner Equinox Minerals in 2011. This was the last straw. It was the deal that led to the wholesale replacement of the management team. Barrick's former managers ran the company's debt load from less than $2 billion to almost $14 billion. This debt load threatened to bankrupt the company when the prices of gold and copper fell.

As a result, the share price has been completely destroyed, falling almost 75% over the last five years. In terms of share price, you have to go all the way back to 1992 – almost 25 years ago – to find a lower price on the stock.

![]() But here's the thing... despite the gross mismanagement, Barrick still owns most of the highest-quality gold mines in the world. And the new management team is made up of top-quality global bankers. They've been selling assets, as well as refinancing and paying down debt, which is already less than $10 billion and on schedule to fall another $2 billion this year.

But here's the thing... despite the gross mismanagement, Barrick still owns most of the highest-quality gold mines in the world. And the new management team is made up of top-quality global bankers. They've been selling assets, as well as refinancing and paying down debt, which is already less than $10 billion and on schedule to fall another $2 billion this year.

In short, the tremendous transformation in internal and capital structure going on at Barrick is going to create billions of dollars in value for shareholders... even if the price of gold doesn't move.

![]() Consider this: Back in 2006, when gold was trading for about half the price of what it is today, Barrick paid $10 billion for one of the best mining companies in the world, Placer Dome. Placer brought Barrick a high-quality portfolio of operating mines and top-quality prospects, like Alaska's Donlin mine. But at the bottom of its share price last September, Barrick Gold, including all of its assets, was trading for less than $8 billion – a discount to the price of the Placer acquisition back in 2006.

Consider this: Back in 2006, when gold was trading for about half the price of what it is today, Barrick paid $10 billion for one of the best mining companies in the world, Placer Dome. Placer brought Barrick a high-quality portfolio of operating mines and top-quality prospects, like Alaska's Donlin mine. But at the bottom of its share price last September, Barrick Gold, including all of its assets, was trading for less than $8 billion – a discount to the price of the Placer acquisition back in 2006.

If Thornton continues his successful turnaround of Barrick, there's no doubt in my mind the company will far outperform its peers and the GDX fund. Barrick was by far the most beaten-up major stock in the sector. It could double from here and still be cheap.

![]() That's just one example of the kind of work we'll be doing for gold investors during the coming bull market in gold. I'm confident that even a small allocation into gold and gold stocks of your portfolio (say, 15% to 20%) will be enough, with a few of our best ideas, to hedge your entire portfolio. This will allow you to continue to generate wealth even if the kind of bear market I expect develops.

That's just one example of the kind of work we'll be doing for gold investors during the coming bull market in gold. I'm confident that even a small allocation into gold and gold stocks of your portfolio (say, 15% to 20%) will be enough, with a few of our best ideas, to hedge your entire portfolio. This will allow you to continue to generate wealth even if the kind of bear market I expect develops.

And what if we're wrong? Then these stocks will just produce average returns, as we're going to pick the best companies in the sector... stocks like Barrick that will do well for investors, even if gold doesn't soar like we expect.

![]() Please... join us Wednesday to learn a lot more. I believe it could turn out to be the most valuable evening of your life. Major turning points like this don't happen often in gold. You have to be ready – and onboard – when they do.

Please... join us Wednesday to learn a lot more. I believe it could turn out to be the most valuable evening of your life. Major turning points like this don't happen often in gold. You have to be ready – and onboard – when they do.

Steve Sjuggerud will join us. He'll review all of his historical data studies, plus give us his fundamental outlook for gold. I'll be on the call with my analysts to talk about the kind of work we've been doing in individual gold-stock names (like you see here about Barrick). And of course, we'll talk about the likelihood of the Metropolitan Plan coming to pass, along with reviewing the other major calls we're making now about the coming big wave of credit defaults.

Best of all? Consider the price. The conference call is 100% free. Reserve your spot by clicking here.

![]() New 52-week highs (as of 4/4/16): Coca-Cola (KO), McDonald's (MCD), Altria (MO), Nuveen AMT-Free Municipal Income Fund (NEA), Nuveen Premium Income Municipal Fund 2 (NPM), Public Storage (PSA), Travelers (TRV), and Wells Fargo – Series W (WFC-PW).

New 52-week highs (as of 4/4/16): Coca-Cola (KO), McDonald's (MCD), Altria (MO), Nuveen AMT-Free Municipal Income Fund (NEA), Nuveen Premium Income Municipal Fund 2 (NPM), Public Storage (PSA), Travelers (TRV), and Wells Fargo – Series W (WFC-PW).

![]() Several more subscribers weigh in on the "Metropolitan Plan" and how they've personally taken our warnings to heart. We've also received hundreds of questions about these ideas and our upcoming conference call tomorrow night. As you know, we can't provide individual advice, but I'll be answering several of the most common questions in tomorrow's Digest. Send yours to feedback@stansberryresearch.com.

Several more subscribers weigh in on the "Metropolitan Plan" and how they've personally taken our warnings to heart. We've also received hundreds of questions about these ideas and our upcoming conference call tomorrow night. As you know, we can't provide individual advice, but I'll be answering several of the most common questions in tomorrow's Digest. Send yours to feedback@stansberryresearch.com.

![]() "I read with great interest your report on the Metropolitan Plan. I have been wondering what I have been calling the 'the day after' plan would look like for several years now. That the crisis is coming, I have been without doubt for over a decade now. How it will play out, I see one to three scenarios (all of which you have written about at length), and have been taking steps to prepare for any of them. It's the 'what happens next' that has intrigued me, and I must admit that the Metropolitan Plan has me with my eyebrows up. Clearly pegging the dollar to metals is the smart thing to do, which is why I naturally assumed that it would be the LAST thing that politicians would think to do... I cannot wait until Wednesday to hear more, as well as how I might benefit further.

"I read with great interest your report on the Metropolitan Plan. I have been wondering what I have been calling the 'the day after' plan would look like for several years now. That the crisis is coming, I have been without doubt for over a decade now. How it will play out, I see one to three scenarios (all of which you have written about at length), and have been taking steps to prepare for any of them. It's the 'what happens next' that has intrigued me, and I must admit that the Metropolitan Plan has me with my eyebrows up. Clearly pegging the dollar to metals is the smart thing to do, which is why I naturally assumed that it would be the LAST thing that politicians would think to do... I cannot wait until Wednesday to hear more, as well as how I might benefit further.

"With that, I have to add, I disagree with the common assumption among talking heads that a strong dollar inevitably means a crash to our economy. Sure, I get it that a strong dollar means people spend more on imported goods than domestic goods. But at some point, people stop buying cheap foreign crap. After all, your shelves can only hold so many tchotchkes. True, foreign cars would then become more competitive (as in the '70s) BUT, at the same time, manufacturers would then be able to buy the parts, and raw materials that they need from overseas to build their 'stuff' much cheaper, which means that US manufacturers can be competitive despite a strong dollar.

"So just as some industries do better in a strong economy and others in a weak economy, while car manufacturers would suffer, etc. and anything dependent on imported parts (electronics) would sour. Lastly, the collapse in oil prices may have been very bad news for the oil business, but I have yet to hear a single driver complain about getting gas cheaper... I can only assume that the same would hold true if the US Dollar is the only currency that is considered to be worth anything (how ironic would that be given how badly it's been debased?), and so with a stronger dollar so too would be a more eager consumer...

"HOWEVER, I COMPLETELY agree that my opinion on the economy does not matter for squat, given that I'm not likely to be appointed to the position of Chairman of the Fed anytime soon, and with that, I admit that I agree with your (Porter's) assumption that the government will take the very steps described here (but first they will likely attempt to raise taxes, and attempt to restrict the use of paper money (if not outright ban it), and prohibit, or tax the use of precious metals)... Anyway, if nothing else, the next decade or two will at a minimum be... interesting." – Paid-up subscriber Joe J.

![]() "Porter, I think you have the basic thesis pretty much on the mark. But I have doubts about negative rates in the US. First, it seems that central bankers are discovering a truth: that dropping interest rates 1/4%, say from 2% to 1 3/4%, or 1/2% to 1/4%, or even 1/4% to 0%, has a very different result than going from 0% to negative 1/4%. I suspect most of your readers will go 'DUH!' or similar, as did Munich Re. It's sort of like climbing down the ladder on a dock on the lake. The difference in altitude does not make much difference in breathing. But when you go a little lower, just so your mouth and nose are below the surface of the water, it is a whole different environment. So far the results of negative rates have not produced anything close to the expected/hoped results. In some cases the opposite.

"Porter, I think you have the basic thesis pretty much on the mark. But I have doubts about negative rates in the US. First, it seems that central bankers are discovering a truth: that dropping interest rates 1/4%, say from 2% to 1 3/4%, or 1/2% to 1/4%, or even 1/4% to 0%, has a very different result than going from 0% to negative 1/4%. I suspect most of your readers will go 'DUH!' or similar, as did Munich Re. It's sort of like climbing down the ladder on a dock on the lake. The difference in altitude does not make much difference in breathing. But when you go a little lower, just so your mouth and nose are below the surface of the water, it is a whole different environment. So far the results of negative rates have not produced anything close to the expected/hoped results. In some cases the opposite.

"Ok, it is possible that the FED would go there anyway even with this contradictive evidence. But I assume/hope they will realize it won't work here either. Something else will trigger the 'run on the dollar.' There all too many possible triggers. Which one and when, that is anyone's guess. Some guesses are better informed than others, though; but guessing correctly here does not earn extra points.

"I had started to believe that the US will muddle through, as it always has; at least during my lifetime. I base that on the fact that most of the rest of the world is in just as bad shape as the US, or worse. That a contingency plan for negative rates is even being considered, makes me think I might be the one having to use the gold and silver (and bullets), instead of my children or grandchildren." – Paid-up subscriber H.E.

![]() "Approx 1/3 of investable assets in physical gold/silver. Very little debt. Live on rural acreage. Cash on hand. Read Stansberry!" – Anonymous

"Approx 1/3 of investable assets in physical gold/silver. Very little debt. Live on rural acreage. Cash on hand. Read Stansberry!" – Anonymous

Regards,

Porter Stansberry

Baltimore, Maryland

April 5, 2016

|