Feeling good after last week's rout... Blue chips getting destroyed... Buffett's record earnings... Have we seen the top in junk bonds?... Apollo's new hedge fund... Two-day plunge for GoPro... A big surprise in LA...

"Down days always make me feel good."

"Down days always make me feel good."

Following last week's selloff, we'll start today's Digest with a "feel good" story... and the above quote from billionaire investor Warren Buffett...

Buffett surprised 17-year-old Tre Grinner last week. Grinner, who suffers from Hodgkin's Lymphoma, wants to be an investment banker. So the Make-A-Wish Foundation arranged an internship for him with Goldman Sachs.

In a live interview with CNBC about his experience with Goldman, Grinner was treated to another gift – an on-air phone call with Buffett. You can see the full interview on CNBC's website here.

Buffett's advice to Grinner – the same wisdom he often spouts – was timely, given the market's terrible week...

|

He also urged Grinner to study accounting in college, which he called "the language of business."

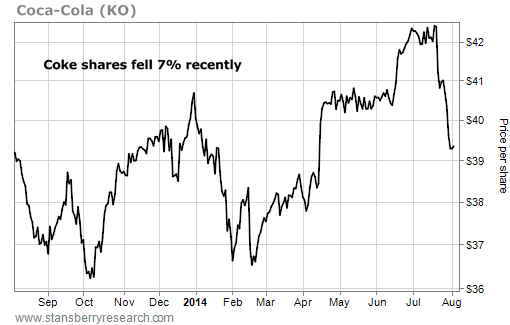

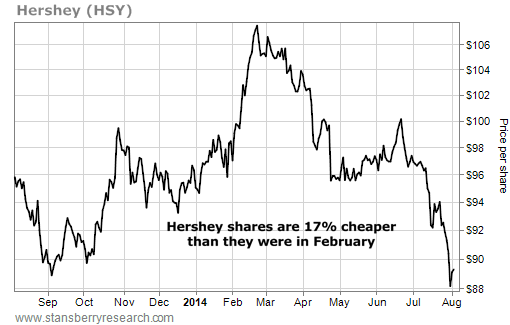

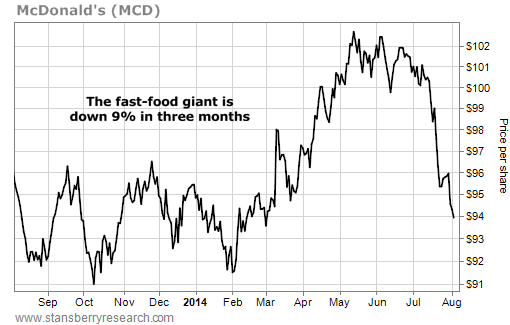

Some of the world's best businesses are going on sale...

These are some of the world's best (and simplest) businesses. You should be eager to scoop up shares when these companies sell off. For example, soft-drink giant Coca-Cola is still selling beverages all over the world and it's still gushing cash... The same could be said for Hershey and its chocolate bars.

In short, these are the same businesses they were a month ago... But you're paying less for them.

Maybe these lower prices will tempt Buffett to deploy some of the record $55.5 billion of cash Berkshire currently holds.

Berkshire announced quarterly revenue increased 11%, from $44.7 billion a year ago to $49.8 billion today. The company earned a record $6.4 billion last quarter, up 41% versus a year ago.

We asked Dr. David "Doc" Eifrig – who holds Berkshire shares in his Retirement Millionaire portfolio – for a comment on its earnings. He said Berkshire's blowout numbers are another sign our economy is slowly improving...

|

It may take some time for Buffett to deploy his record cash pile... Berkshire only bought $2.1 billion of equities in the first half of the year, about a third of the total from a year ago. Meanwhile, stock sales more than doubled to $3 billion. Like us, he's having a difficult time finding value (at least, until last week's pullback). Fortunately, we know Buffett is patient...

In the meantime, Retirement Millionaire subscribers are up 127% since Doc recommended shares in April 2009.

Outside of Berkshire, blue-chip stocks are getting walloped. But blue chips aren't the only area of the market taking a hit...

High-yield bonds (aka "junk bonds") have been one of the hottest sectors in the market. Junk bonds are debt issued from the riskiest corporate creditors. Because these companies are more likely to default, they have to pay higher interest rates to attract investors.

But in today's yield-starved environment, investors pushed junk-bond yields to a record-low 4.8% in June, according to data from investment bank Barclays. That is minuscule compared with an average yield of 22.9% back in 2008.

In the first seven months of the year, companies sold $210.8 billion of high-yield debt... the highest since at least 2000, according to international finance firm Dealogic.

But the trend changed last week...

U.S. junk-bond funds lost 1.3% last month, according to Barclays. It was the second-worst monthly performance since November 2011. The only worse single-month performance was June 2013, when the Federal Reserve started to hint it would scale back its quantitative easing efforts.

In the past three weeks, investors have pulled more than $5.5 billion out of junk-bond funds. As Marty Fridson, one of the world's top bond analysts, told the Financial Times...

|

We previously shared Fridson's dire views regarding the corporate-bond market in the May 16 Digest after seeing him speak at the Grant's Interest Rate Observer Conference in New York City...

|

In addition to rich valuations, investors are also selling junk bonds out of fear that the secondary market may be drying up. As we noted above, the primary market for junk bonds (companies selling debt to the public) is booming. But trading after the fact is thinning. Part of this is due to tougher capital regulations on banks... forcing them to hold higher-quality assets on the balance sheet.

Dealer inventories for junk bonds dropped to $4.8 billion in July, the lowest level since April 2013, when the Federal Reserve Bank of New York began publishing data for different types of debt. That's down from $7.9 billion the previous week.

And only 1.8% of outstanding U.S. bonds traded on an average day in the first quarter of this year, down from 2.2% a year ago. (From 2002 to 2008, the figure was 3%, according to the Securities Industry and Financial Markets Association.)

And institutional investors are seeing the effects...

Brian Connolly, co-founder of hedge fund Millstreet Capital Management, told the Wall Street Journal he recently tried to sell $3 million of energy company bonds but couldn't find buyers for three days. That trade would typically have taken a maximum of one day... "It has become increasingly harder to trade," he said.

Ben Inker, co-head of asset allocation at the $118 billion asset manager GMO, also says it's tougher to trade...

He sold short some bonds earlier this year... When he recently tried to close the position (by buying back the bonds in the open market), he "couldn't find any of the bonds," he told the Journal.

Fridson says the banks' holdings don't matter all that much... We'll face a much larger problem with banks when the market turns... As he told the Financial Times, "The reality is when the market starts to go down, [the banks] stop answering the telephones."

One more factor will add to the severity of a junk-bond selloff...

"Mom and Pop" investors own more than one-third of corporate bonds through bond funds and exchange-traded funds (ETFs). These retail investors think ETFs solve the liquidity problem for bonds. But as SkyBridge Capital managing partner Raymond Nolte told the Financial Times...

|

Porter offered his take on the situation in the May 16 Digest...

|

Right now, many of the world's largest bond funds have huge positions in junk bonds... To learn more about which funds are potentially investing your money in these risky securities, be sure to reread the May 29 Digest.

One final bit on junk bonds... Private-equity giant Apollo Global Management recently announced it was starting a hedge fund to bet against U.S. junk bonds.

The firm – which boasts $101 billion under management – started trading for the fund last November using the firm's own money. It began fundraising this month and plans to go live this fall, according to the Wall Street Journal.

Shares of camera maker GoPro (GPRO) fell nearly 15% last Friday after quarterly earnings failed to live up to the hype. You may remember our skepticism following the company's recent initial public offering (IPO). We wrote about GoPro at length in the June 30 Digest. As we explained...

|

So far, it looks like we're right...

Revenues for the second quarter were $244.6 million, up 38% versus the same period a year ago. But revenues only increased 4% versus the $235.7 million reported in the first quarter of 2014.

And the company lost $19.8 million for the quarter... worse than the $5.1 million it lost in the same period a year ago.

GoPro shares fell as much as 5% today. We bet the rout is just beginning...

We have an exciting update on our conference taking place in Los Angeles on August 23...

Last week, we secured the chief technology officer (CTO) from a company we discuss often in the Digest... a certain electric car manufacturer.

If you couldn't guess, I'm talking about Tesla. CTO J.B. Straubel is joining us in LA. This is one of the first public appearances he has ever made.

If you would like to see Straubel face off with Porter, you'll need to join us in Los Angeles for our third live event.

Straubel is only one of the amazing presenters we've arranged... We have also booked Chris Anderson, the former editor of Wired magazine and one of the brightest minds in technology. Anderson is going to share his vision of the future in terms of technology... And he's also going to demonstrate one of the newest and most popular consumer technologies live from the stage.

You'll also hear from Porter, Steve Sjuggerud, former head of Morgan Stanley Asia Peter Churchouse, and famed societal satirist P.J. O'Rourke.

And if you joined us in Dallas, you know we always have a couple surprises planned... Like when Porter made his presentation dressed as General Motors CEO Mary Barra.

We hope to see you in LA. If you're interested in reserving a seat, you should act quickly... We're raising the price on August 8. Click here to sign up.

New 52-week highs (as of 8/1/14): Lynden Energy (LVL.V).

Two pieces of positive feedback in today's mailbag... You all must have had a good weekend. Send your e-mails to feedback@stansberryresearch.com.

"You and your team are the best I've come across in my 43 years. Best advice for the money, hands down. It's unfortunate that you have to advertise the way you do. It's only unfortunate because you only do it because it works. It's almost like the opposite of the old "bait and switch." What you actually provide is far more valuable than the hype of the ads. But people need excitement I guess. (You're not building Stansberry Coliseum any time soon I hope.) As a friend once told me: 'The only people that complain, are the complainers.' Keep doing what you're doing and the rest will take care of itself. Cheers." – Paid-up subscriber Jeff Wright

"Having just been to the motley fool meeting in San Fran (which was interesting but not a Stansberry level) I realize just how much your editors and you (and Bill Bonner which they quoted often at this event) have fundamentally taught me (sorry not taught, what I have learned) about the markets, economics trading, investing and especially options. What you offer does not exist anywhere else and although I think I can learn quite a bit on my own now (thanks to the foundation you have provided) I am convinced that your 'system' of providing learning opportunities daily is the most important and why I encourage anyone who will listen to read your info – the more the better so the bias of one editor can be compared to others. Great job!!" – Paid-up subscriber DB

New 52-week highs (as of 8/1/14): Lynden Energy (LVL.V).

Two pieces of positive feedback in today's mailbag... You all must have had a good weekend. Send your e-mails to feedback@stansberryresearch.com.

"You and your team are the best I've come across in my 43 years. Best advice for the money, hands down. It's unfortunate that you have to advertise the way you do. It's only unfortunate because you only do it because it works. It's almost like the opposite of the old "bait and switch." What you actually provide is far more valuable than the hype of the ads. But people need excitement I guess. (You're not building Stansberry Coliseum any time soon I hope.) As a friend once told me: 'The only people that complain, are the complainers.' Keep doing what you're doing and the rest will take care of itself. Cheers." – Paid-up subscriber Jeff Wright

"Having just been to the motley fool meeting in San Fran (which was interesting but not a Stansberry level) I realize just how much your editors and you (and Bill Bonner which they quoted often at this event) have fundamentally taught me (sorry not taught, what I have learned) about the markets, economics trading, investing and especially options. What you offer does not exist anywhere else and although I think I can learn quite a bit on my own now (thanks to the foundation you have provided) I am convinced that your 'system' of providing learning opportunities daily is the most important and why I encourage anyone who will listen to read your info – the more the better so the bias of one editor can be compared to others. Great job!!" – Paid-up subscriber DB

Regards,

Sean Goldsmith

August 4, 2014

Why the latest Russian sanctions may affect your brokerage account...

In today's Digest Premium, S&A Global Contrarian editor Kim Iskyan explains what the latest Russian sanctions mean. Plus, he explains how they may personally affect your investment accounts...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

Why the latest Russian sanctions may affect your brokerage account...

Editor's note: In today's Digest Premium, S&A Global Contrarian editor Kim Iskyan explains what the latest Russian sanctions mean. Plus, he explains how they may affect your personal investment accounts...

Last week, the U.S. and European Union rolled out their latest sanctions aimed toward forcing Russia to pull back on its activities in Ukraine. Regulators and investors and other market participants are still in the process of figuring them out... and the investment implications may be bigger than they first appeared.

As part of the sanctions, the U.S. prohibited a number of Russian companies from raising new equity or debt from Western investors. One of the companies on the list was Russia's second-largest bank, VTB. The bank is state-controlled, but minority shareholders own a 39% stake. And a large portion of those shareholders are foreign investors.

VTB has no current plans to raise new funding, although it may need to at some point. Western investors could violate sanctions if VTB tried to raise new capital.

Why should you care about this? You may not know it, but you may own a small stake of VTB. If you own an emerging-market mutual fund, exchange-traded fund, pension fund, or a similar pooled investment, chances are good you hold some shares.

The number of shares of VTB that a fund holds is likely in part a function of the benchmark holding. These benchmarks can show how much of a generic emerging-market portfolio would be allocated to each emerging market, usually based on the overall market size. Portfolio managers use these weightings to help determine how to manage their portfolios.

In the world of asset management, these companies are very important. An organization's decision to increase or decrease the weighting of a particular country or company in an index can trigger massive inflows into or outflows from a market or a stock.

On Thursday, finance firm MSCI announced it might have to exclude VTB from its indexes to avoid potentially violating sanctions. If MSCI follows through with this – and it will announce its decision on Friday – investors could sell as much as $900 million in shares. For a bank with a market cap of $14 billion, that's a significant chunk of stock.

This could be just the tip of the iceberg. If more big Russian stocks end up on the sanctions list, MSCI could strike them from its indexes, which could lead to investors essentially fleeing from Russian stocks.

Of course, for every seller of a share, there's a buyer... but a lot of forced selling could lead to a sharp decline in share prices. And if a large segment of the investors who focus on emerging markets are no longer able to buy Russian stocks, these companies – and the Russian stock market – could remain cheap for a long time.

– Kim Iskyan

Why the latest Russian sanctions may affect your brokerage account...

In today's Digest Premium, S&A Global Contrarian editor Kim Iskyan explains what the latest Russian sanctions mean. Plus, he explains how they may personally affect your investment accounts...

To continue reading, scroll down or click here.