How we made 600% gains in 2009... And why we have the same opportunity today... Buying 'value destroyers'... The inherent cyclicality of resources... Buying before the price explosion... One of our top recommendations today...

The last time we saw this opportunity, readers made nearly 600% gains in less than a year...

The last time we saw this opportunity, readers made nearly 600% gains in less than a year...

That kind of opportunity only comes around once or twice a decade. We saw it in 2000... We saw it in 2009... And we have that opportunity again today...

Buying these stocks at the right time is one of the surest and most consistent bets in the market. It's one of the only trades you can make where prices essentially have to go up.

When I tell you what we're bullish on today – an opportunity we think can triple your money and pay you huge income – most of you will close this Digest in disgust. But that's great. Often, buying the best investments is hard to do... The sector is beaten-up and hated. Most investors have left it for dead (or vowed never to buy it again after suffering huge losses).

But the greatest values and biggest gains are born from these situations. And the handful of investors who have the stomach to purchase can make a fortune... In fact, they're almost guaranteed to make money. Some of the richest people we know (with billion-dollar fortunes) have used this strategy over and over again for decades. It's the classic contrarian setup.

Extreme Value editor Dan Ferris calls these situations "value destroyers." He explained the idea in the September 17 DailyWealth...

|

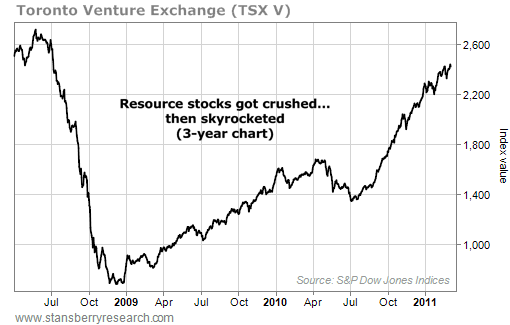

With the markets at all-time highs, natural resource stocks are one of the few values we see in the market. Consider what's going with the Toronto Venture Exchange – the "Dow Industrials of small resource companies." It's the most widely followed gauge of small-cap precious metals and energy firms. The following chart shows the struggle in resource stocks... As you can see, the Venture fell 66% from early 2011 to mid-2013…

We're not surprised to see resource stocks scraping along the bottom... The industry is inherently cyclical. And if you know how to spot these cycles, you can make huge money.

Resource markets are cyclical for two primary reasons... They're extremely capital-intensive and they're extremely time-intensive. It takes a lot of time and money to produce, mine, and extract resources. It's because of this long timeline (and huge capital expenditures) that big opportunities arise.

We're not surprised to see resource stocks scraping along the bottom... The industry is inherently cyclical. And if you know how to spot these cycles, you can make huge money.

Resource markets are cyclical for two primary reasons... They're extremely capital-intensive and they're extremely time-intensive. It takes a lot of time and money to produce, mine, and extract resources. It's because of this long timeline (and huge capital expenditures) that big opportunities arise.

As billionaire resource investor Rick Rule of Sprott Global explained in an educational interview titled "Mastering the Resource Market's Cyclicality"...

|

As Rick explained, on the other side, after supplies come onto the market, prices peak and start to fall. The industry regards its sunk costs as just that... sunk costs. So it's hesitant to slow production, despite high supplies and falling prices...

|

Said another way, the cure for high prices is high prices... And the cure for low prices is low prices.

Today, many resources have low prices. If you missed the major rallies in 2000 and 2009, don't worry... You have another chance today.

As we mentioned above, one of the highest-returning recommendations in Stansberry Research history was a value destroyer.

Resource stocks got crushed in 2008 during the subprime crisis. Beginning in late 2008 and early 2009, they staged a huge and rapid comeback...

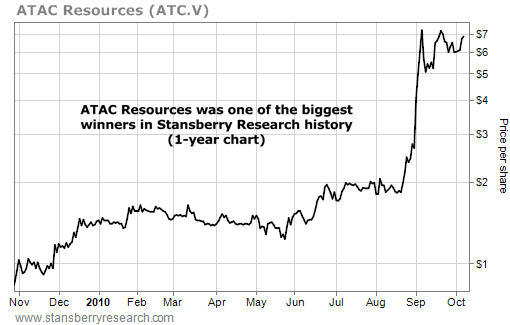

Our in-house resource expert Matt Badiali recommended shares of gold miner ATAC Resources (ATC.V) in the November 2009 issue of Phase 1 Investor. It was a tiny mining company with a solid project in Canada's Yukon Territory.

Our in-house resource expert Matt Badiali recommended shares of gold miner ATAC Resources (ATC.V) in the November 2009 issue of Phase 1 Investor. It was a tiny mining company with a solid project in Canada's Yukon Territory.

It discovered gold in late 2008, but Matt said the company was still early in the "Discovery Curve"... And it would find lots more gold. Matt was right. ATAC proved it held a valuable asset... It reported positive drilling results, and in July 2010, ATAC announced a huge discovery with grades four to five times the original discovery. As you can see from the chart below, shares soared...

When shares of ATAC took off, it happened fast. We think the sector could take off again at any moment... When our recommended stocks pop 50% or 100% in a month, they won't be nearly as attractive as they are today.

When shares of ATAC took off, it happened fast. We think the sector could take off again at any moment... When our recommended stocks pop 50% or 100% in a month, they won't be nearly as attractive as they are today.

That's why it's so important to buy into the resource sector soon... before stocks take off.

Once again, we have a rare chance to buy some of the world's best resource companies at depressed prices.

Commodities are down across the board. According to precious-metals firm Kitco, silver and gold are down 64% and 37%, respectively, from their peaks. Mining-research firm InfoMine reports that uranium, coal, and copper are down 75%, 59%, and 31%, respectively, from their peaks.

As a result, resource stocks have taken a hit.

And in Extreme Value, Dan is preparing his subscribers for the eventual turnaround. Dan has recommended a handful of excellent resource companies you can buy today at bargain prices... Today, four of the six remain in buy range.

But Dan is touting one company above all others... He says this stock is so safe and cheap, it's one of five companies he'd put in a "set it and forget it" portfolio right now.

To give you an idea of how solid Dan believes this tiny resource stock is, some of the other companies in the "set it and forget it" portfolio are $40 billion payroll processor Automatic Data Processing (ADP) and $17 billion booze giant Constellation Brands (STZ).

Regular Digest readers will recognize this company's name... It's one of our highest-conviction recommendations today.

Dan calls this investment "by far one of the best opportunities in the natural resource sector I've seen in my entire career." It profits from a handful of different commodities, like gold, uranium, coal, and potash... In other words, its fate isn't tied to the price of a single commodity.

And the company's earnings (and share price) are about to soar...

It recently completed a deal that will pay huge royalties in the future... Dan says the deal will boost its revenue 10-fold. And he is 100% certain the company will start paying a "substantial" dividend in the next couple years... He thinks it will be a double-digit yield based on today's share price.

Considering today's yield-starved market, once word gets out that this natural resources firm is paying a huge dividend, shares will skyrocket.

As we explained, the stock is a great value today... But we think it could jump 50% higher any day now. And we won't feel comfortable recommending this investment at such an elevated price (though we do believe the upside is much greater than 50%).

If you're looking for a diversified way to invest in the beaten-down commodity space and purchase a stock before it starts paying out a huge dividend (which by itself will send shares soaring higher), we recommend you look further into this idea.

Again, this is only the third time since 2000 where we've had such a great entry point into commodities. We hope you don't miss out. To learn more about Extreme Value – and Dan's top recommendation – click here.

New 52-week highs (as of 9/19/14): WisdomTree Japan Hedged Equity Fund (DXJ), ProShares UltraShort Euro Fund (EUO), Google (GOOG), Johnson & Johnson (JNJ), Altria (MO), Microsoft (MSFT), Pepsico (PEP), and ProShares Ultra Health Care Fund (RXL).

As expected, dozens of you wrote in (and copied us) to voice your opinion on Devon Energy from Porter's Friday Digest. We're running just a tiny sample of them below. Send us your thoughts – Devon-related or otherwise – to feedback@stansberryresearch.com.

"I would like to see Devon greatly increase its operating margins and its return on equity by continuing to sell its low-margin operations, most importantly, its Jackfish Canadian oil-sands operations. Please note that nearly all of the other management teams at similarly positioned, low-margin energy producers (like Chesapeake and Hess) have been replaced because they were not responsive to investor demands to improve results. I plan to vote against ALL of the incumbent directors next year unless immediate changes are made to improve Devon's profitability by selling the Canadian oil-sands project." – Paid-up subscriber Gary Helwig

"Dear Sirs, as a stock holder of Devon I would like to give you the below suggestions:

New 52-week highs (as of 9/19/14): WisdomTree Japan Hedged Equity Fund (DXJ), ProShares UltraShort Euro Fund (EUO), Google (GOOG), Johnson & Johnson (JNJ), Altria (MO), Microsoft (MSFT), Pepsico (PEP), and ProShares Ultra Health Care Fund (RXL).

As expected, dozens of you wrote in (and copied us) to voice your opinion on Devon Energy from Porter's Friday Digest. We're running just a tiny sample of them below. Send us your thoughts – Devon-related or otherwise – to feedback@stansberryresearch.com.

"I would like to see Devon greatly increase its operating margins and its return on equity by continuing to sell its low-margin operations, most importantly, its Jackfish Canadian oil-sands operations. Please note that nearly all of the other management teams at similarly positioned, low-margin energy producers (like Chesapeake and Hess) have been replaced because they were not responsive to investor demands to improve results. I plan to vote against ALL of the incumbent directors next year unless immediate changes are made to improve Devon's profitability by selling the Canadian oil-sands project." – Paid-up subscriber Gary Helwig

"Dear Sirs, as a stock holder of Devon I would like to give you the below suggestions:

"First, I want to tell the non-management directors that I would like to see Devon greatly increase its operating margins and its return on equity by continuing to sell its low-margin operations, most importantly, its Jackfish Canadian oil-sands operations. Second, I want to remind you that nearly all of the other management teams at similarly positioned, low-margin energy producers (like Chesapeake and Hess) have been replaced because they were not responsive to investor demands to improve results.

"Currently I own over 200 shares of Devon and I will vote against ALL of the incumbent directors next year unless immediate changes are made to improve Devon's profitability by selling the Canadian oil-sands project." – Paid-up subscriber Dennis A. Brimeyer

"I would like to see Devon increase its operating margins and its return on equity by continuing to sell its low-margin operations. Selling the Canadian oil-sands project seems like the obvious thing to do. I will be voting my 100 shares for or against based on what actions I observe." Paid-up subscriber Dwight Carlson

"When the proxy materials arrive rest assured I will vote against every board member if Devon remains in the Canadian oil sand. Company involvement needs to be sold off." – Paid-up subscriber Cecil Hash

"I am a current Devon shareholder and do not think the company is being managed in a way that is attempting to maximize shareholder value and in fact is negligent. It surely begs some questioning of management competence when the company is valued at 1.4 times book value when comparable companies such as EOG Resources with similar holdings is valued at 3.5 times book value. I would like to see Devon greatly increase its operating margins and its return on equity by continuing to sell its low-margin operations, most importantly, its Jackfish Canadian oil-sands operations.

"In regard to the points I raise in the first paragraph nearly all of the other management teams at similarly positioned, low-margin energy producers (like Chesapeake and Hess) have been replaced because they were not responsive to investor demands to improve results. I own approximately 1000 shares and have held them approximately two months. I plan to vote against ALL of the incumbent directors next year unless immediate changes are made to improve Devon's profitability by selling the Canadian oil-sands project.

"Please evaluate the direction of Devon compared to its competitors in the Bakken and similar shale plays in Texas. Devon is declining in value while your competitors are increasing. Senior management in this company need to seriously re-evaluate the company's direction as the shareholders will not stand idling by hoping they come to their senses." – Paid-up subscriber Bill Randall

Regards,

Sean Goldsmith

September 22, 2014

How to find great buying opportunities in small-cap stocks...

Small Stock Specialist editor Frank Curzio has delivered several huge winners to his subscribers. And despite most stocks trading near all-time highs today, Frank says one trend in the market is "great news for small-cap stocks."

In today's Digest Premium, he'll explain why... And he'll share the strategy he used to lead his subscribers to gains of 118% in Steel Dynamics (STLD), 104% in semiconductor firm Skyworks Solutions (SWKS), 87% in private-equity giant KKR (KKR), and 80% in oil-services stock Superior Energy Services (SPN)...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

How to find great buying opportunities in small-cap stocks...

Editor's note: Small Stock Specialist editor Frank Curzio has delivered several huge winners to his subscribers. And despite stocks trading near all-time highs today, Frank says one trend in the market is "great news for small-cap stocks."

In today's Digest Premium, he'll explain why... And he'll share the strategy he used to lead his subscribers to gains of 118% in Steel Dynamics (STLD), 104% in semiconductor firm Skyworks Solutions, 87% in private-equity giant KKR (KKR), and 80% in oil-services stock Superior Energy Services (SPN)...

Right now, large-cap companies are struggling for growth.

Many are having difficulty growing earnings. They have been able to mask this through record amounts of share buybacks. This is a great strategy when your stock price is cheap. However, the average large-cap stock is trading at 18 times forward earnings. That's a little expensive – even with short-term interest rates near record-low levels.

And not every company has pricing power. Most companies can only raise their prices so much. In short, large-cap companies are running out of ways to grow earnings. So they're turning to small-cap stocks for that. Some small-cap companies are growing two or three times faster than the overall market.

A lot of large-cap companies have strong balance sheets and are willing to pay huge premiums to buy this growth. That's why we're seeing a lot of acquisitions and takeovers today, especially in biotech and technology stocks. I expect this trend to continue over the long term. And that's great news for small-cap stocks.

It's also great news for stocks in the Small Stock Specialist portfolio, where I've been focusing on cheap companies with huge growth potential. Not only do they provide upside based on valuation, but the fact that they are growing faster than the market makes them all takeover candidates.

One example is the 3D-printing sector. Many of the companies in this sector have pulled back from their highs. Large-cap tech companies like Hewlett-Packard are late to the party and are just now jumping in. I wouldn't be surprised if we see several deals in this sector over the next few months now that their shares have pulled back.

We're also seeing some incredible volatility in the sector. We're seeing 30% declines almost immediately after a small-cap stock reports bad news or misses earnings. But digging into the research, these stocks should not be selling off this much. It's an overreaction.

One example is a stock we hold in the Small Stock Specialist portfolio, in-flight connectivity firm Gogo (GOGO). GOGO shares fell 60% off their highs, and a lot of that is due to news that AT&T is going to enter the market. AT&T has a fortress balance sheet – and can pour a lot of cash into this major growth trend. Investors are concerned AT&T can take considerable market share from GOGO, so they ran to the exits. Meanwhile, we're up 29% in four months.

But if you take a closer look, you'll see that GOGO commands 80% market share of in-flight connectivity in the U.S. It has 10-year contracts with every major airline. By the time AT&T enters this market (in 2016), GOGO will probably have a 50% share of the international market, which is three times bigger than the domestic market.

Plus, AT&T announced it would enter the in-flight connectivity market before announcing its $48 billion bid for satellite television provider DirecTV. In short, AT&T has its hands full right now with regulators trying to get this deal to pass. That could push AT&T's timetable to get into the in-flight market back another year.

We got into GOGO at around $14.50 per share after the stock pulled back. But investors didn't know about all those contracts, and AT&T isn't going to be competition for two more years. We are already up 32% on our position in four months.

We used the same strategy to buy companies like private-equity firm KKR (KKR), steel company Steel Dynamics (STLD), oil and gas services company Security Energy Services (SPN), and chip manufacturer Skyworks Solutions (SWKS). Right now, we're up 97% on average in those four positions. That's because we were patient and bought shares following major overreactions. These 20% or 30% declines in small caps happen often – almost daily. And it makes for a fantastic opportunity for someone like me who watches the sector every day.

– Frank Curzio

Editor's note: Last week, Frank told Small Stock Specialist subscribers about two companies with massive upside potential. As he explained, "It will lower the price of nearly everything, allow us to predict the future, and let you sleep while you drive." Plus, for a limited time, Frank is offering one year of his newsletter for 60% off the retail price. To learn more about Small Stock Specialist and Frank's research, click here.

How to find great buying opportunities in small-cap stocks...

Small Stock Specialist editor Frank Curzio has delivered several huge winners to his subscribers. And despite most stocks trading near all-time highs today, Frank says one trend in the market is "great news for small-cap stocks."

In today's Digest Premium, he'll explain why... And he'll share the strategy he used to lead his subscribers to gains of 118% in Steel Dynamics (STLD), 104% in semiconductor firm Skyworks Solutions (SWKS), 87% in private-equity giant KKR (KKR), and 80% in oil-services stock Superior Energy Services (SPN)...

To continue reading, scroll down or click here.

Stansberry & Associates Top 10 Open Recommendations

(Top 10 highest-returning open positions across all S&A portfolios)

As of 07/21/2014

| Stock | Symbol | Buy Date | Return | Publication | Editor |

| Prestige Brands | PBH | 05/13/09 | 411.6% | Extreme Value | Ferris |

| Enterprise | EPD | 10/15/08 | 316.2% | The 12% Letter | Dyson |

| Constellation Brands | STZ | 06/02/11 | 310.5% | Extreme Value | Ferris |

| Ultra Health Care | RXL | 03/17/11 | 268.2% | True Wealth | Sjuggerud |

| Ultra Health Care | RXL | 01/04/12 | 222.2% | True Wealth Sys | Sjuggerud |

| Altria | MO | 11/19/08 | 210.2% | The 12% Letter | Dyson |

| Targa Resources | TRGP | 12/13/12 | 187.6% | SIA | Stansberry |

| Blackstone Group | BX | 11/15/12 | 179.1% | True Wealth | Sjuggerud |

| McDonald's | MCD | 11/28/06 | 178.1% | The 12% Letter | Dyson |

| Automatic Data Proc | ADP | 10/09/08 | 158.2% | Extreme Value | Ferris |

Please note: Securities appearing in the Top 10 are not necessarily recommended buys at current prices. The list reflects the best-performing positions currently in the model portfolio of any S&A publication. The buy date reflects when the editor recommended the investment in the listed publication, and the return shows its performance since that date. To learn if a security is still a recommended buy today, you must be a subscriber to that publication and refer to the most recent portfolio.

| Top 10 Totals |

| 3 | Extreme Value | Ferris |

| 3 | The 12% Letter | Dyson |

| 2 | True Wealth | Sjuggerud |

| 1 | True Wealth Sys | Sjuggerud |

| 1 | SIA | Stansberry |