It's a bull market, you know... Yellen gets dovish... Everything is hitting new highs... One type of oil stock is doing well... Another record for Apple... Tesla gets slammed by Bank of America Merrill Lynch... Shares could fall to $65... Sprott: A wave of consolidation in the gold sector...

It's a bull market, you know...

It's a bull market, you know...

Officials in the European currency union (or "eurozone") reportedly approved Greece's reform plans... and the country is back on track for its four-month bailout extension. Regular Digest readers know we aren't concerned with the situation in Greece. As we explained yesterday, it's in everybody's best interest for the eurozone and Greece to cooperate. And we're sure they'll eventually reach a deal.

Also, Federal Reserve Chair Janet Yellen testified to Congress today. She took a "dovish" tone, hinting that interest rates could remain low for longer than previously expected. (The market had previously expected a rate increase in June.) From her speech...

|

Yellen also said she would give the markets plenty of notice before hiking rates...

|

A quick glance at the stocks hitting new 52-week highs shows the U.S. consumer is alive and well.

First, home-improvement retailer Home Depot announced a 36% increase in fourth-quarter earnings to $1.4 billion. Revenue rose 8.3% to $19.2 billion. Home Depot also said it was buying back $18 billion of shares.

Fellow home-improvement chain Lowe's and homebuilders Lennar and D.R. Horton also hit new highs.

Restaurants Darden Restaurants (which owns Olive Garden, Longhorn Steakhouse, and Capital Grille), Domino's, Restaurant Brands International (Burger King and Tim Horton's), Papa John's, Popeyes, Jack in the Box, Sonic, Starbucks, and Texas Roadhouse all hit new highs, too.

Booze giant Anheuser-Busch InBev and cigarette companies Altria, Lorillard, and Reynolds American hit new highs. "Middle American" retailers AutoZone, Dillard's, Dollar General, and Ross Stores hit new highs.

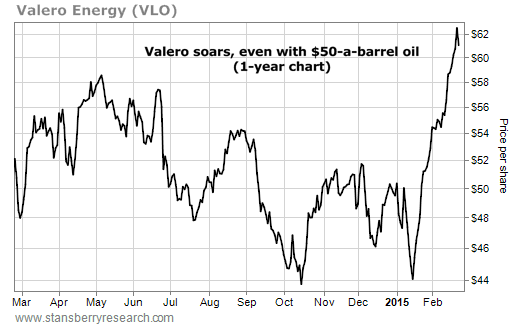

Stansberry Resource Report recommendation Valero Energy (VLO) is also trading at a new high.

Shares of the world's largest independent refiner have been on a tear lately. They're up more than 35% since the middle of January...

The growth in U.S. crude oil production ensures that Valero's most important raw material will remain available.

Editor Matt Badiali noted another positive for the company: Valero uses natural gas as the primary power source to run its plants. Gas was around $4 per thousand cubic feet (mcf) when Matt recommended the company in October. Today, prices are at $2.90 per mcf. Cheaper gas means bigger margins for Valero.

And Valero is operating well. In the first three quarters of last year, Valero had a 96% utilization rate at its plants. This was its highest rate in the past five years.

The more Valero produces, the more money it makes. Valero's sales have more than doubled since 2009, to nearly $131 billion last year. And its EBITDA margin (earnings before interest, taxes, depreciation, and amortization as a percentage of sales) increased by 150% over this period to 5.8%.

In short, the company is doing well in all facets. Valero raised its quarterly dividend by 45% in January... the eighth time it has increased its dividend since 2011. Over that period, Valero increased the dividend nearly 800%, from $0.045 to $0.40 per share.

Matt's Resource Report subscribers are up 40% on the recommendation.

And Apple hit another record high of more than $133 a share today, pushing the market cap to more than $775 billion.

The consumer-products giant jumped 2.7% yesterday partly due to a Barron's article that said the stock could hit $160. Barron's said at $160, Apple would still trade at a 17 times forward earnings multiple – in line with the S&P 500.

As we noted in the February 18 Digest, Extreme Value editor Dan Ferris says Apple could reach a $1 trillion market cap.

As we mentioned earlier, "it's a bull market, you know." I borrowed the line from one of the greatest books ever written on trading – Reminiscences of a Stock Operator, by Edwin Lefevre. The quote comes from a trader in the book nicknamed "Old Turkey." And Old Turkey's advice is as good today as it was when the book was published in the 1920s. When the market is rising, it pays to be along for the ride.

We excerpted a bit about Old Turkey in a classic DailyWealth essay from 2007. It's a great, short read. Click here to read it.

In the midst of this bull market, Bank of America Merrill Lynch analyst John Lovallo published an incredibly bearish piece on electric-car manufacturer Tesla.

Lovallo cut his price target on the stock from $70 to $65. (It trades at $205 today.) He noted that a major bull-case for the stock is inaccurate. Tesla founder and CEO Elon Musk has repeatedly said his company can't keep up with demand... and that the only limit to the company right now is its ability to supply cars.

The bulls believe Tesla will crank up supply and money will fall from the skies. Musk says 2015 production could ramp up from around 33,000 vehicles last year to 55,000 vehicles this year.

Just two weeks ago, we discussed how Tesla – one of our favorite short targets – reported a fourth-quarter loss of $108 million.

And the company only delivered 9,834 vehicles in the quarter, well short of expectations for 11,142. Tesla said it couldn't deliver 1,400 vehicles due to "customers being on vacation, severe winter weather, and shipping problems (with actual ships)," supporting the bulls' thesis that supply issues (rather than demand) are holding the company back. From Lovallo...

|

If Lovallo is correct, it would be devastating for Tesla's stock, which is already down nearly 30% from its September highs.

And remember... we don't need a disaster for Tesla shares to tumble. This company is priced for perfection at nine times sales. And it has huge interest from the public.

Things only need to go from "great to less great" for Tesla shares to fall.

A research note from resource-investing firm Sprott Resources discussed the current state of the market from company Chairman Eric Sprott and Rick Rule, founder of global companies at Sprott. It also features commentary from Gloom Boom & Doom Report editor Marc Faber.

As gold prices marched to $1,900 an ounce in 2011, mining companies went on a buying spree, thinking the good times couldn't end. Then gold prices fell. Miners were forced to liquidate assets and take huge write-offs.

But the Sprott team says we're about to see some activity in the sector...

|

They also noted that "cash is king" in this market...

Mining companies require loads of capital to bring an asset into production. And many junior miners – which start with a small amount of capital anyway – are running out of money. Sprott noted the cash held by junior gold miners listed on the benchmark TSX Venture Index fell from C$3.5 billion in early 2010 to around C$1 billion today – a fall of more than 70%.

Some miners are closing their doors. The good projects are desperate for cash to keep their projects alive... which is why Sprott says "cash is king." And certain players in the gold sector will benefit for the need for capital...

|

As regular Digest readers know, we're also bullish on gold and gold stocks today.

The thesis is straightforward: Central banks are cutting rates, printing money, and engaging in all-out currency wars. And gold is the best insurance to protect yourself from this madness.

Also, record-low (and negative) interest rates make gold's 0% yield more attractive.

Plus, gold's price action is super-bullish as it's outperforming all major currencies.

As we also noted yesterday, True Wealth Systems editor Steve Sjuggerud recommended his top gold trade in February issue. He said his "super signal" flashed buy... When this happens, the asset Steve recommends returns 47% on an annualized basis.

New 52-week highs (as of 2/23/15): Apple (AAPL), Automatic Data Processing (ADP), Brookfield Asset Management (BAM), Becton Dickinson (BDX), ProShares Ultra Nasdaq Biotech Fund (BIB), Cempra (CEMP), Cisco (CSCO), Express Scripts (ESRX), iShares Core S&P Small-Cap Fund (IJR), SPDR S&P International Health Care Sector Fund (IRY), Medtronic (MDT), 3M (MMM), PowerShares QQQ Fund (QQQ), PowerShares Ultra Technology Fund (ROM), ProShares Ultra Health Care Fund (RXL), and Valero Energy (VLO).

In today's mailbag, Steve Sjuggerud responds to a reader's question about his investment strategies. Do you subscribe to True Wealth or True Wealth Systems? Let us know about the biggest winners you're enjoying in your portfolio today. E-mail us at feedback@stansberryresearch.com.

"Hi, I have done well over the years following Steve's recommendations. It began early on when he was director of The Oxford Club. I don't usually write in but I felt I needed an answer as to why Steve recommended selling ROM in True Wealth Systems, (which I sold at $148.00) yet leaving ROM in the True Wealth portfolio where it has since climbed almost 20 points in 2 weeks?

"Now I know to be disciplined and sell if a stock closes at or below your stop. But if it is an ETF that has performed well and has incredible companies within it, shouldn't it have a different set of rules? What I take from this is fundamentals, tech indicators and market momentum don't really matter when selling, only the stop matters, whether it is an ETF or individual stock. Thanks." – Paid-up subscriber Michael Kinney

Sjuggerud comment: Thank you for the kind words, Michael. I'm thrilled to report that we're up 169% on the ProShares Ultra Technology Fund (ROM) in True Wealth. To answer your question, there is a major difference between True Wealth and True Wealth Systems (TWS)... In True Wealth, I call the shots. In True Wealth Systems, our computers call the shots. We trade what the computers tell us to trade, and we don't break those rules. Sometimes, my opinion in True Wealth will be different than what our TWS computers say.

In True Wealth, I'm investing for the long run. In True Wealth Systems, our computers are trading in and out a bit more in the short run. Of course, there will be some overlap, since TWS is built on my ideas. Based on Porter's annual Report Cards (which you can read here and here), my TWS computers have been smarter than me so far. Thanks again for the kudos.

Regards,

Sean Goldsmith

Delray Beach, Florida

February 24, 2015