Masters Series: The Simple Secret to Earning 30% a Year in Bonds

Editor's note: You can make plenty of money without ever touching bonds.

But if you truly understood the corporate-bond market, you would never buy another stock again.

Today's Masters Series essay was originally published in the Digest in June 2014. The numbers that follow reflect the prices available at the time the essay originally ran. In it, Porter shares a real-life example of how you could have made 30% a year buying the bonds of a high-quality company...

The Simple Secret to Earning 30% a Year in Bonds

Rather than blather on more about theory, I'd like to show you a real example of how bonds work. We'll use MGM Resorts (MGM), because it's a company almost everyone understands. The Las Vegas Strip-dominating hotel and casino company is one of our favorite "trophy asset" businesses.

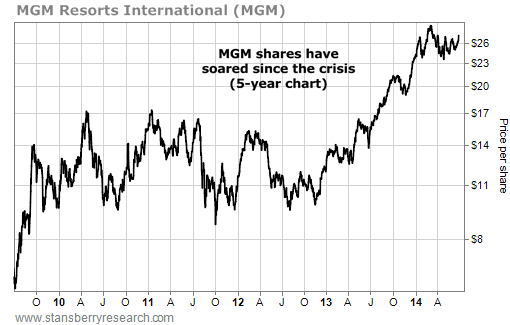

If you take a look at the company's five-year share-price history, you'll discover that MGM's shares got clobbered during the 2008-2009 financial meltdown. The shares later rebounded about 300% from their average price during 2009 (around $10).

The company built out a massive expansion (CityCenter) at exactly the wrong time. But... it still had great assets it could easily sell and it didn't have too much debt. In the middle of the crisis in 2009, the company sold one of its lowest-quality hotels (Treasure Island) for $14,000 per hotel room. Assuming it only got the same value for its more upscale hotels, the company's Vegas assets alone were worth far more than all its debts. And that assumes fire-sale pricing and ignores the company's substantial assets outside of Vegas and in China.

MGM was suffering a liquidity crisis, not a solvency crisis. And that meant buying its debt was safe. You couldn't say the same thing about its stock. Investors had no idea if management would get new funding – if it would be able to keep the "wolf" at bay. Before buying its shares, you needed to wait until you could see sustained improvements in its revenues and cash flows. That's what we did.

On the other hand, buying its debt was always safe. Because no matter what stupid thing management did next, the hotels and casinos were still going to be there... And they were extremely valuable, as the 2009 sale of Treasure Island proved.

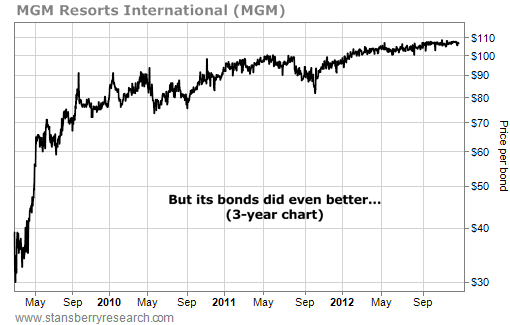

By early 2009, MGM bonds were trading for less than $0.50 on the dollar. They hit bottom at $0.30 on the dollar. Of course, nobody can know when markets will bottom and what the best available price will be. And we won't pretend that looking back we could have gotten the "low tick" in MGM's bonds.

But any price below $0.50 on the dollar would have qualified as a world-class opportunity. At that price, the yield on the bonds would have been 15% annually. That's like Santa Claus showing up at your office with a big sack of free money. Or as I like to say about really obvious investments: horse, meet water.

Only three years later, these bonds were trading back at "par" – 100 cents on the dollar. Over three years, these fully collateralized bonds would have doubled your money. And you also collected another 45% in coupon payments. In my view, earning 145% in three years – without taking any substantial financial risk – is a far better deal than buying any stock...

Sure, MGM's stockholders have done well, too. The stock is up about 150% over five years. But who knew back then if management could right the ship? Who knew what stupid thing it would do next? Who knew how long it would take?

That's the beauty of these deals... As bondholders, we truly didn't care what management did or didn't do. It was up to them to pay us or lose everything. It's like the movie Goodfellas. When the mob lends you money, you have to pay them. Recall the scene where the mobsters burned down the poor guy's restaurant? Oh, business is bad? Too bad, pay us. Oh, a bunch of jerks ran up big tabs and won't pay them? Too bad, pay us. Oh, someone burned down your restaurant? Too bad, pay us. Bondholders have the same exact view. Oh, global financial crisis hurt your business? Too bad, pay us.

If the big returns available in stocks are too irresistible, there's nothing stopping you from combining equity and debt into a single position. If you're fairly confident that management can bail out the ship, you can simply buy shares with the discounted portion of the bond.

Corporate bonds typically trade in face values of $1,000. So if you bought MGM's bonds at $0.50 on the dollar, that would have left you with $500 or so to buy shares. At the time, the stock was trading for less than $10. To make the math easy, let's say you got shares at $10. So you have a bond with a $1,000 face value (purchased at $500) and 50 shares of stock for a total investment of $1,000.

Here's the best part: No matter what happens to the shares, you're going to get all of your capital back, because those bonds mature in 2016 and then the company has to pay you back your $1,000. Even though the stock was really risky back then, you were protected. By today, the bond would have paid you $375 in coupons... and it's trading at a premium to face value. And the shares would be worth roughly $26 each, or $1,300, for a total return of 167% over five years – far more than 30% a year. And again, you really didn't take any risk in this trade.

There are, of course, plenty of pitfalls and problems associated with investing in corporate bonds. The biggest problem is that high-quality assets like MGM's aren't often available as collateral on bonds yielding more than 10%, let alone 15%. There is, however, a regular cycle in the corporate-bond market. Once every seven to 10 years, the market completely blows up. When bond liquidations start, even the highest-quality issuers will see their bonds trading at big discounts to par. A few rules of thumb can help you easily time these cycles.

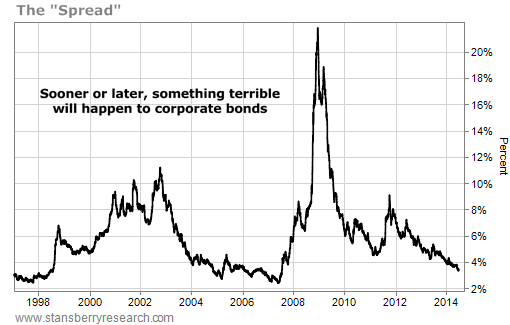

First and foremost, you want to watch the spread (the difference) between high-yield corporate bonds and U.S. Treasurys. This will generally tell you whether corporate bonds are distressed or – as they are now – trading in the clouds.

As you can see in the chart below, the spread between high-yield bonds and U.S. Treasury bonds has rarely been this small. The last time it was this small was 2007. When capital is this cheap and easy, you simply must stand aside from this market, as far too many loans are going to be made to far too many low-quality companies. The result will be a huge wave of debt defaults at some point. We can't know when it will happen – but we know it will happen. Just look back at history...

This chart, from the U.S. Federal Reserve, shows the spread between so-called "risk free" bonds (based on U.S. Treasury bonds with a similar duration) and the Merrill Lynch high-yield corporate-bond index. This is the standard measure of corporate credit conditions. When the spread is low, credit is widely available and cheap. When the spread is high, credit is tight and can be incredibly expensive. Corporate-bond investors should wait to buy corporate bonds until credit is tight and attractive yields abound.

There's something about watching and waiting for the bond market to "roll over" that I really enjoy. This is a when investment, not an if investment. All we have to do is be patient. We know that the feckless, reckless, and stupid management teams running most American companies will borrow too much money and end up in a jam.

It happens every eight years or so. That's about perfect timing for patient investors, as most corporate debt is issued for periods of less than 10 years. You can lock in a solid rate of return buying bonds when they go on sale – when they are trading for less than $0.70 on the dollar and paying more than 10% annually. If you begin to do this, I promise, you'll buy far fewer stocks. You'll make a lot more money as an investor. You'll take dramatically fewer risks. And you'll produce way more income.

Now, I know a lot of you may be scratching your head at what I've written here. After all, no one has issued more adamant warnings about the bubble that has developed in the bond market. And yes... now is not the time to make big investments in the corporate-bond market.

But this essay isn't about what to buy today or tomorrow. I want you to recognize the incredible opportunity corporate bonds represent when the conditions are right, when you can get them at the right time and price. Remember, at some point, all markets turn around. After the bond market collapses, most investors will want nothing to do with fixed-income investments. That's when we'll find lots of great opportunities in this market... ones that meet all three of my guidelines for buying corporate bonds.

How do you buy bonds? And which exact ones should you buy? Don't worry. As you may know, we closed our bond-focused service, True Income, because of the imminent danger I saw in the bond market. In November 2015, we launched a brand-new bond service, called Stansberry's Credit Opportunities. During the last cycle, our bond service did great – we made 81%, on average, in 2009-2010. And as you may have noticed, the Rite-Aid bond we recommended way back then is No. 2 in the Stansberry Research Hall of Fame.

If you want to go forth on your own, remember to focus on companies with lots of very high-quality and easily marketable assets. Judging collateral is a lot different from judging an operating business. You have to think like a pawn dealer: how hard would it be to unload these assets if the idiots running this business really screw the pooch? That's a far different question from figuring out a reasonable price to pay for future cash flows, or brand value, etc.

You'll see me writing far more about bonds in the future than I have in the past. More and more, I believe they're far better investment instruments for most investors. The funny thing is, most brokerage firms make it very difficult for individuals to buy high-yield corporate bonds. Most won't even tell you what bonds are available. And most will only sell you the bonds you want if you're able to tell them the precise CUSIP number of the bond (its trading symbol). That's the best indicator of all. Wall Street's smart money doesn't want you figuring out the best deals in the bond market, which, by the way, is vastly larger than the stock market. Interesting, isn't it?

Regards,

Porter Stansberry

Editor's note: The continuing debt crisis Porter has been predicting will be the greatest opportunity to build wealth in a generation. And the next phase could start as early as October. Investors who follow Porter's bond recommendations will have the chance to make hundreds of percent in capital gains AND lock in income payments of up to 20% per year. Learn how to get started right here.