McDonald's 'atrocious' earnings... Why the stock still surged... A great company to own for the next 15 years... Sjuggerud is right again... Nikkei hits an all-time high... Home sales hit a new high... Einhorn is bearish but says no bubble yet... Doc says the bull has legs...

"I know the earnings are going to be absolutely atrocious... terrifying."

Yesterday, Porter was predicting the result of today's earnings announcement from Stansberry's Investment Advisory recommendation McDonald's on the Stansberry Radio Advisory Roundtable episode, which was released today.

(The Advisory Roundtable is a monthly discussion between Porter and his research analysts. It's available only to Stansberry Radio Premium subscribers. To learn more about a subscription, click here.)

This was McDonald's first quarterly announcement under new CEO Steve Easterbrook. There's no doubt Easterbrook wanted the latest numbers (the final quarter under his predecessor, Don Thompson) to be horrible. It sets a low bar for Easterbrook going forward... and assigns a low value to his options.

And there's no doubt McDonald's latest quarter was bad...

The fast-food giant earned $1.01 per share versus expectations of $1.06 (and down from $1.21 a year earlier). Earnings fell nearly 33%, from $1.2 billion a year ago to $812 million today. That was partially due to "negative guest traffic in all major segments." Revenue was $5.96 billion, just barely beating expectations of $5.95 billion (but still down from $6.7 billion a year ago).

Operating income dropped 11% for McDonald's U.S. operations and 20% in Europe. The Asia Pacific Middle East and Africa (APMEA) segment saw operating income plunge 80%. Same-store sales were down across the board.

But the market was expecting this poor quarter, and McDonald's shares rallied as much as 4.7% today. That's also because Easterbrook said he would unveil the company's turnaround plan on May 4 to "to improve our performance and deliver enduring profitable growth."

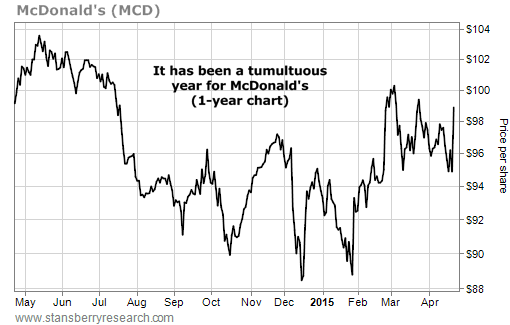

Regular Digest readers know we're bullish on McDonald's. As you can see from the chart below, shares took a beating as the company announced slowing sales due in part to a consumer shift toward fast-casual restaurants like Chipotle Mexican Grill... McDonald's also suffered from a scandal in China involving contaminated meat last July...

Despite its recent troubles, Porter thinks McDonald's will become one of the greatest recommendations of his career – right up there with candy maker Hershey.

Both companies produce huge amounts of cash selling branded products with huge margins. These are the poster children for capital efficiency (meaning they can return loads of capital to shareholders because the costs to maintain their businesses are low).

And despite what the mainstream media would have you believe, McDonald's isn't going anywhere... We'd happily take the other side of the bet that fast food is a dying business. McDonald's remains one of the largest restaurant companies in the world. And it will adapt.

Porter wrote more about McDonald's in the April 10 Digest. As he explained...

You'll notice that capital-efficient firms always report far more cash earnings than net income – the official GAAP accounting earnings number. That occurs because the size of the depreciation charges (which count against official net income earnings) are exaggerated in firms that have long-lived assets or, like McDonald's, that receive most of their income from intangible brands and from royalty streams.

Few investors realize what a great business McDonald's really is because most investors focus on GAAP accounting. Consider this... McDonald's current GAAP account price-to-earnings ratio is 20. That's pretty expensive. It's almost twice as expensive as we view the price of the company – 11 times EBITDA. But the stock is cheap (no matter what GAAP accounting claims) because McDonald's has been suffering from a bad CEO for several years (who was recently replaced). Because of this, McDonald's has seen revenues slow and even shrink slightly. And Wall Street worships growth above all else.

How does McDonald's perform on our capital-efficiency tests? Last year, its gross margins were almost 40% and its operating margins were an incredible 28% on sales of nearly $28 billion. And that was a "bad" year. Although GAAP accounting only credits McDonald's with earning $4.7 billion, the company actually produced 42% more cash from operations and was able to return more than $6 billion to its shareholders.

On the Advisory Roundtable episode, Porter said you should "be piling as much money as you can into McDonald's" if you have 10 to 15 years to invest.

Switching gears a bit, what would our daily Digest be without giving kudos to True Wealth editor Steve Sjuggerud? For the past five years, it seems Steve can do no wrong. Regular readers know he successfully predicted the "Bernanke Asset Bubble," making his subscribers a fortune in real estate (up 114%), health care (up 448%), technology (up 159%), and a number of other sectors.

As we discussed yesterday, he also correctly predicted the boom in Chinese stocks. And let's not forget his call for a rally in Japanese stocks in late 2012... What Steve called "Abe's Revenge."

Like his U.S. counterpart (then-Federal Reserve Chairman Ben Bernanke), Japanese Prime Minister Shinzo Abe pledged to do everything in his power to create inflation. And he kept his word.

The result? The Nikkei, Japan's benchmark index, crossed 20,000 for the first time since 2000...

True Wealth subscribers are up 78% (including dividends) on Steve's recommendation of the WisdomTree Japan Hedged Equity Fund (DXJ)... The fund goes long Japanese stocks while hedging out the currency risk – an excellent call given the strength in the U.S. dollar...

One more bragging point for Steve...

In Monday's Digest, we reiterated Steve's bullish real estate call. Today, we see sales of existing U.S. homes hit their highest level in 18 months. According to news service Reuters, the National Association of Realtors announced that existing home sales rose 6.1%, the largest percent increase in more than four years. Meanwhile, February's sales pace was revised higher, from 4.88 million units to 4.89 million units.

One of the smartest hedge fund managers in the game, David Einhorn of Greenlight Capital, released his latest letter to investors. Einhorn is renowned for correctly predicting the collapse of Lehman Brothers. Today, he is incredibly bearish...

Bottom-up: Short candidates are easy to find, but as noted above, the opportunity set on the long side is quite constrained. Most of the investment theses we have reviewed over the past several months can at best be described as late-cycle opportunities, with valuations that often ignore historical economic sensitivity. The operating (and in some cases activist) execution needed to achieve target results has to be rated at Triple Lindy difficulty level.

Top-down: Valuations are on the high side and earnings are in a precarious spot. Last year's snow slowed the entire economy, setting up the first quarter to be the easiest comparison quarter of the year. It nonetheless hasn't turned out to be a good quarter (despite this year's snow confining itself mostly to New England). At year-end, first quarter earnings were supposed to grow about 5%, but now, they are expected to decline by a similar amount, and this doesn't even include GE's large, anticipated first-quarter charge as it exits most of GE Capital.

The bull case is that equities haven't yet reached bubble levels at a time when fixed income is behaving bubbly, and that the Fed will support the market. As to the former, it may prove true. We don't like the proposition of betting on a bubble, though one may yet emerge (or, more clearly, a bubble might expand beyond the current small group of high flying stocks). As to the latter, despite all the attention paid to every utterance of any member of the FOMC, it is clear that the Fed isn't going to add further accommodation unless conditions deteriorate substantially. How fast it tightens should be less important than the fact that it will tighten.

Einhorn still thinks Apple is cheap today. The consumer-products company is his largest position. His third-largest position, according to his letter, is gold.

Our own Dr. David "Doc" Eifrig agrees that we're not yet in bubble territory... only he isn't as bearish as Einhorn is.

In today's DailyWealth, Doc told readers to remember what a bubble looks like... Greed runs rampant. Safeguards go out the window. People can't buy enough stocks, real estate, etc.

But as Doc showed, that's not what's happening today...

The best-performing investments have been the safest ones. Blue-chip dividend-payers have outperformed the market drastically. The thing is, it's strange to have the old, stodgy, and boring companies lead the way.

But it's rare that they outperform the market over this long of a term. It's a clear sign that investors aren't taking risks. They are buying the safest stocks.

Worse than buying conservative equities, investors are also buying U.S. Treasurys at low yields... and buying German and Swiss bonds at negative yields. More from Doc...

That's not to say that we won't see corrections in the coming months. We never try to predict such things. But we feel confident that a major bear market is still not a threat in the immediate future.

Yes, the market is getting expensive... and this bull market is closer to the end than the beginning. But for now, stay the course.

New 52-week highs (as of 4/21/15): Deutsche X-trackers Harvest China A-Shares Fund (ASHR), Blackstone Mortgage Trust (BXMT), WisdomTree Japan Hedged Equity Fund (DFJ), SPDR S&P International Health Care Sector Fund (IRY), and Varian Medical Systems (VAR).

In the mailbag, a question about Steve Sjuggerud's incredible Blackstone recommendation. Keep the questions coming at feedback@stansberryresearch.com.

"In the 'Market Notes' section [of today's DailyWealth], it says that Blackstone's annual dividend yield has skyrocketed. Are we to infer that is due to the dividend being increased a large amount? You don't say why it's up, but if the stock has more than doubled, wouldn't that mean that the dividend would have to increase to increase the yield?" – Paid-up subscriber Jeff Kelsey

Goldsmith comment: Yes. As we explained in the April 16 Digest, Steve recommended shares of Blackstone back in November 2012 at $13.52 per share. Yesterday, Blackstone closed at $41.72... a 237% gain in two and a half years.

In November 2012, Blackstone paid a $0.52 per share annual dividend (a 3.8% yield). That annual dividend has grown to $2.12 per share (based on the previous 12 months). So anyone who took Steve's advice and bought at $13.52 per share earned $2.12 per share in dividends in the last year ($2.12 / $13.52 = 15.7%). That's why we say Steve's subscribers are earning a 15.7% dividend on their initial investment.

The dividend has grown as Blackstone earns more and more cash from profitable asset sales. In fact, the company announced last week it would pay a first-quarter dividend of $0.89. That's the largest quarterly dividend in the firm's history, resulting from its most profitable quarter ever.

Regards,

Sean Goldsmith

Baltimore, Maryland

April 22, 2015