The key to making money in distressed markets...

The key to making money in distressed markets... A real-life example... A foolproof way to 'time' the market... Three things you must remember... Don't forget to sign up for Thursday's webinar...

![]() Over the last three Digests, I (Porter) have been explaining our strategy for making big profits in distressed equity markets.

Over the last three Digests, I (Porter) have been explaining our strategy for making big profits in distressed equity markets.

Hopefully by now you can see the key to our plan is using volatility to create income by selling puts. This income, in turn, provides the fuel for us to make far more speculative bets. We can use part of the premium we collect to buy call options.

If you don't know how to sell a put or how to buy a call, I'd suggest reviewing the previous Digests (here, here, and here) and also talking with your broker. Each firm's trading platform is going to be a little different, so just ask your broker to walk you through the process. Learn how to do it by trading one contract first and you'll see exactly how it works.

![]() In this way, trading in distressed equity markets is a lot like trading in distressed debt: The key is to make sure you're getting enough income to more than justify the risks you're taking. In today's Digest, I'm going to show you exactly how to make these trades, what to look for, and most important, how to manage the risks you're taking.

In this way, trading in distressed equity markets is a lot like trading in distressed debt: The key is to make sure you're getting enough income to more than justify the risks you're taking. In today's Digest, I'm going to show you exactly how to make these trades, what to look for, and most important, how to manage the risks you're taking.

![]() Not surprisingly, we've already gotten several notes from the "boo birds" in our audience. They see what we're doing as incredibly risky – even reckless. The same crowd attacked our distressed-credit strategy, too. They can't wrap their heads around the idea that volatile and distressed markets create massive opportunities. But of course, they do create those opportunities.

Not surprisingly, we've already gotten several notes from the "boo birds" in our audience. They see what we're doing as incredibly risky – even reckless. The same crowd attacked our distressed-credit strategy, too. They can't wrap their heads around the idea that volatile and distressed markets create massive opportunities. But of course, they do create those opportunities.

In the bond market, the key to success is avoiding default. In the stock market, the key to success is even easier: it's to only sell puts on stocks that you're genuinely happy to own and at a strike price that reflects an excellent value.

Let me give you a real example...

![]() Back in February 2009, the stock market had been in deep distress since the collapse of Lehman Brothers in mid-September 2008. Volatility (as measured by the "VIX") had been elevated (above 20, and usually above 30) for the entire period.

Back in February 2009, the stock market had been in deep distress since the collapse of Lehman Brothers in mid-September 2008. Volatility (as measured by the "VIX") had been elevated (above 20, and usually above 30) for the entire period.

Stocks had been falling, almost every month, for a year. Finally, on February 10, the market experienced yet another genuine panic. The Dow Jones Industrial Average was in virtual free fall, down 4% on the day. For distressed investors, this was the perfect market environment. Stocks had been beaten up for months and volatility was spiking.

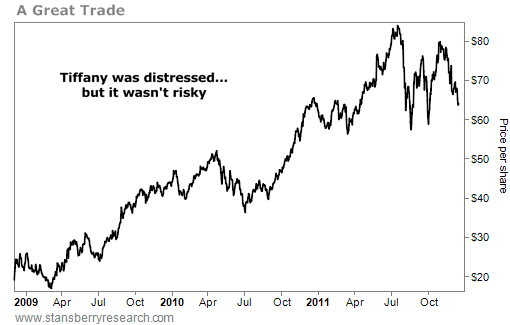

![]() Tiffany (TIF) is a company we have long admired. It has one of the world's foremost brands. It sells the highest-quality jewelry in the world – and more of it than any other company. Its profit margins are the envy of retailers.

Tiffany (TIF) is a company we have long admired. It has one of the world's foremost brands. It sells the highest-quality jewelry in the world – and more of it than any other company. Its profit margins are the envy of retailers.

Tiffany has fantastic retail locations and millions of repeat customers. Its balance sheet is full of gold, silver, platinum, precious stones, and real estate. What's not on its balance sheet (at least, not fairly represented) is the incredible value of its brand. However, a year into the worst bear market since the Great Depression, Tiffany's shares were trading for only $21.

It might be hard to understand how cheap that was. Let me explain it this way...

![]() Ben Graham – Warren Buffett's mentor and the longtime dean of value investing – created a formula for when to buy stocks in the midst of a crisis. This is the ultimate measure of high-quality value in stocks:

Ben Graham – Warren Buffett's mentor and the longtime dean of value investing – created a formula for when to buy stocks in the midst of a crisis. This is the ultimate measure of high-quality value in stocks:

| • | Assets greater than two times total liabilities |

| • | 10 consecutive years of profits |

| • | 20 years of uninterrupted dividend payments |

| • | Earnings growth in the past decade of at least 33% |

| • | A price-to-book ratio no higher than 1.5 |

Finding super-high-quality stocks with these value parameters is extremely rare. At the market bottom in 1991, only six stocks qualified. At the bottom in late 2002, only two stocks qualified. By early February 2009, eight stocks met this most stringent test of value... and Tiffany was one of them.

![]() And there was a huge hole missing from Graham's analysis: goodwill. Tiffany doesn't carry any goodwill on its balance sheet. That means you won't find the value of its brand or the value of its huge customer list anywhere on its financial statements.

And there was a huge hole missing from Graham's analysis: goodwill. Tiffany doesn't carry any goodwill on its balance sheet. That means you won't find the value of its brand or the value of its huge customer list anywhere on its financial statements.

Meanwhile, it is the brand that creates those 50%-plus gross margins. In short, buying Tiffany where it stood that day at $21 per share was one of the best opportunities I had ever seen in the stock market.

![]() I knew it was almost impossible for Tiffany's shares to trade lower. Someone would have bought the entire business, or Tiffany's management would have launched a massive share-buyback campaign (and later, it did). And yet... because there was so much volatility and so much fear, even far-out-of-the-money put options were trading at high prices.

I knew it was almost impossible for Tiffany's shares to trade lower. Someone would have bought the entire business, or Tiffany's management would have launched a massive share-buyback campaign (and later, it did). And yet... because there was so much volatility and so much fear, even far-out-of-the-money put options were trading at high prices.

We recommended selling a put option with a $15 strike price! That strike price was 28% "out-of-the-money." Again, in my view, it was functionally impossible for the stock to trade at that low of a price for long. I considered this put option to be 100% safe. There was no way Tiffany was going to trade for less than $15. No way. Meanwhile, we were paid $1 per share to assume that risk for 90 days. For every put contract we sold, we got $100 in cash upfront. (Remember, each option contract represents 100 shares.)

![]() Assuming you sold 10 contracts, you would have gotten $1,000 in cash upfront. Your "risk" was the obligation to purchase 1,000 shares of Tiffany at $15 in 90 days. Thus, measured against the capital you were potentially putting at risk ($15,000), you were going to earn more than 6.5% in 90 days. On an annualized basis, that's far more than you're likely to make in stocks.

Assuming you sold 10 contracts, you would have gotten $1,000 in cash upfront. Your "risk" was the obligation to purchase 1,000 shares of Tiffany at $15 in 90 days. Thus, measured against the capital you were potentially putting at risk ($15,000), you were going to earn more than 6.5% in 90 days. On an annualized basis, that's far more than you're likely to make in stocks.

And you shouldn't have had to put up $15,000 in capital, either. With a Level IV options account, you could have used your broker's capital to do this trade. You would have only put up $3,000 in margin. Thus, your return on margin would have been 33% in just 90 days. If there's a better way to make money in stocks, I haven't found it yet.

![]() But aren't options risky? In the minds of some of our subscribers, yes.

But aren't options risky? In the minds of some of our subscribers, yes.

They perceive selling options as being risky because if you're put the stock, you will have to buy $15,000 worth of shares.

On the other hand, if you're able to look at the trade objectively, you'll see that there's virtually no risk at all. For us to lose money on this trade, Tiffany shares would have to trade below $14. That would be an additional 33% decline from its rock-bottom price of $21. And outside of a nuclear bomb going off in New York City, there's just no realistic way Tiffany would fall that far, that fast. It isn't a leveraged financial stock. It isn't in a commodity business. It's one of the world's truly great businesses. It wasn't going to fall 33% more in just 90 days.

![]() The other way to look at it is, what's the risk of buying a stock you want to own at a 33% discount from its current price? There's no risk at all, assuming you're prepared, willing, and able to hold the shares through the crisis. If that happens (and sooner or later, it will), you can generate additional income by selling call options against the position – something we'll discuss in our upcoming webinar. (By the way, you can sign up for the free webinar we're hosting on Thursday by clicking here.)

The other way to look at it is, what's the risk of buying a stock you want to own at a 33% discount from its current price? There's no risk at all, assuming you're prepared, willing, and able to hold the shares through the crisis. If that happens (and sooner or later, it will), you can generate additional income by selling call options against the position – something we'll discuss in our upcoming webinar. (By the way, you can sign up for the free webinar we're hosting on Thursday by clicking here.)

The point is, there are all kinds of ways to win. If the stock stays flat, you keep the premium. You win. If the stock goes up, you keep the premium. You win. And even if the stock falls 20% or 30%, you're still making money in this trade.

I know that seems incredible, but it's absolutely true. And if you end up being put the stock and you have to buy it, what's the downside? You just bought one of the world's bust businesses at a price that's far below the liquidation value of its inventory. Sooner or later, that asset is going to make you a lot of money.

![]() This isn't a hypothetical example. That's the exact trade we recommended in the February 10, 2009 issue of our Put Strategy Report. Here's exactly how I described the opportunity back then...

This isn't a hypothetical example. That's the exact trade we recommended in the February 10, 2009 issue of our Put Strategy Report. Here's exactly how I described the opportunity back then...

I would sell these options heavily – perhaps even up to 10% of my liquid net worth, assuming I could get $1 for the option. With the stock market in freefall, there's a very good chance these options will trade up to $1. Wait for them to reach our price. Don't agree to sell for a penny less... Assuming these options expire worthless, you'll make 33% against your margin in only three months – or roughly 133% on an annualized basis.

![]() As stocks sold off, these put options did trade for more than $1, putting our subscribers into the trade. As you surely know, Tiffany did not go out of business or anywhere close. Instead, these puts expired worthless in 90 days and we kept the entire $1-per-share premium. It was one of the best trades I had ever seen. And I'm certain we will see dozens more opportunities like this in the months to come, as the market begins to see more and more frequent moments of panic.

As stocks sold off, these put options did trade for more than $1, putting our subscribers into the trade. As you surely know, Tiffany did not go out of business or anywhere close. Instead, these puts expired worthless in 90 days and we kept the entire $1-per-share premium. It was one of the best trades I had ever seen. And I'm certain we will see dozens more opportunities like this in the months to come, as the market begins to see more and more frequent moments of panic.

![]() Is it possible to lose a lot of money selling puts? Yes, of course. Just like it's possible to lose a lot of money buying distressed debt. And lots of foolish investors will lose money in these markets because they won't stick to the safe trades like the Tiffany trade. Instead, they will "yield shop" and end up buying the riskiest bonds and selling the riskiest puts. Don't let that be you.

Is it possible to lose a lot of money selling puts? Yes, of course. Just like it's possible to lose a lot of money buying distressed debt. And lots of foolish investors will lose money in these markets because they won't stick to the safe trades like the Tiffany trade. Instead, they will "yield shop" and end up buying the riskiest bonds and selling the riskiest puts. Don't let that be you.

The amazing thing about distressed markets is that you don't have to take big risks to generate huge returns. In these markets, even the safest financial assets become mispriced and offer tremendous upside. All you have to do is take the easy deals. You can ignore everything else.

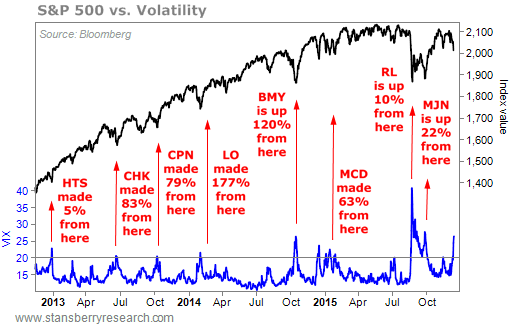

![]() But is it possible to actually time the market this way? Yes. It's easy. You don't have to try to predict when the market will panic. You just have to wait until it does. In our Stansberry Alpha newsletter, we've established positions 13 times around spikes above 20 in the VIX. We've made money on these trades 85% of the time, producing annualized returns on margin of 50%.

But is it possible to actually time the market this way? Yes. It's easy. You don't have to try to predict when the market will panic. You just have to wait until it does. In our Stansberry Alpha newsletter, we've established positions 13 times around spikes above 20 in the VIX. We've made money on these trades 85% of the time, producing annualized returns on margin of 50%.

Doing this kind of trading on distressed stocks is the safest and most lucrative way I know to make money in the stock market. And we're entering a period where there will be three or four opportunities every year to establish new positions.

As you can see from the chart below, you don't have to guess when volatility will spike, you just have to wait until it does...

![]() If you want to make a lot of money trading around distressed stocks and panicking equity markets, you just need to remember a few basics...

If you want to make a lot of money trading around distressed stocks and panicking equity markets, you just need to remember a few basics...

First and foremost, never sell a put on a stock you don't want to own and at a strike price you're not thrilled to pay. Most subscribers will eventually break this rule. They'll lose discipline and start chasing yield... and they'll get hurt. Don't let that be you.

Second, you have to make sure that the income you're going to receive and the strike price you've selected offers you a huge margin of safety. Look at that Tiffany trade. If we had been put the shares, our entry price would have been $14 per share. That was 33% less than the Ben Graham "bottom" that investors very rarely see in high-quality stocks.

In a situation like that, earning a profit on that investment would have been essentially guaranteed. A little more than two years later, the shares were almost to $80. If we had been put the stock, we would have made more than 400%. For us, there was no actual downside to this trade. It was only a question of whether we would make a lot of money quickly or a lot of money over two years...

And third... you want to find options with a high implied volatility. This is a confusing topic that requires a lot of hard math to figure out. That's why your broker will simply give you the implied volatility of the option you're buying.

Options are priced based on the volatility of the shares. The more the stock moves around, the more expensive the options will become. And sometimes, the implied volatility of the option is much higher than the actual volatility in the shares. Those are the options you want to sell, because they are too expensive relative to the underlying stock.

![]() Now, listen... You don't need to worry about trying to figure out implied volatility on your own. We're building a computer system to scan the entire market and isolate individual options that are badly mispriced.

Now, listen... You don't need to worry about trying to figure out implied volatility on your own. We're building a computer system to scan the entire market and isolate individual options that are badly mispriced.

We did the same thing in our distressed-credit product, Stansberry's Credit Opportunities. We built a proprietary system to analyze almost every individual corporate bond that matures in the next five years. This lets us quickly and easily identify the outliers. Our system gives us a huge advantage. We'll have a similar advantage when dealing with distressed equities, too.

![]() Tomorrow, we'll go through a real example, from start to finish. We'll look at different strike prices and maturity dates to find the best fit between price and implied volatility. This will be a real trade – something you might want to try with your own account. And tomorrow night, I'll host a webinar detailing this strategy. I'll explain everything and answer any of your questions.

Tomorrow, we'll go through a real example, from start to finish. We'll look at different strike prices and maturity dates to find the best fit between price and implied volatility. This will be a real trade – something you might want to try with your own account. And tomorrow night, I'll host a webinar detailing this strategy. I'll explain everything and answer any of your questions.

But you have to do one thing first. You have to call your broker and get access to a Level IV options-trading account. Without this approval, you won't be able to use margin to back up the puts we're going to be selling. That means you won't be able to do as many trades or make as much money.

Be prepared to call several brokers until you find one willing to work with you. (And for subscribers who have done this, please send us a note about which broker you're using and what the process was like. We'll pass along the info to other subscribers looking for a good broker.)

![]() Before I sign off, I just want you to think about how your account might look if you take advantage of this strategy...

Before I sign off, I just want you to think about how your account might look if you take advantage of this strategy...

Let's say you have a $100,000 portfolio. You're aware that we're entering a period of credit distress and rising default rates. You've already sold about half of your stocks because they've hit trailing stop losses or because you thought it was prudent to raise some cash ahead of what's likely to be a bear market.

As a result, you have $50,000 in cash. You've begun to buy some distressed bonds, and you have a few long-term stock investments that you're sure will survive the storm and pay you great dividends along the way, so you don't want to sell them. Let's say your portfolio is 50% in cash, 25% in bonds, and 25% in high-quality stocks.

Your plan is to execute the trades we recommend in Stansberry Alpha when the VIX spikes to 30 or higher. Just as an example, let's assume that all of the trades you end up putting on are exactly like the Tiffany trade I described above. These opportunities also have $15 strike prices and $1 premiums. You sell 10 contracts on each of the four positions, so each position has a potential obligation of $15,000. You're limiting your potential obligation to $60,000, or 60% of your portfolio.

Keep in mind, using your broker's capital, you should only have to tie up $12,000 of your cash. That's great, because it keeps most of your powder dry, so when good new bond opportunities arrive, you'll still have plenty of capital available.

These four Alpha positions will each give you $1,000 in cash upfront. Every 90 days, you'll earn $4,000 on your $12,000 margin (33%). As you roll these positions forward, you'll keep making at least $4,000 as long as the stocks go up or fall less than 20% in 90 days.

If you repeat this strategy over the course of a year, you'll earn $16,000 for your portfolio, while only tying up $12,000 of capital. And with some of this money, you can buy cheap, out-of-the-money call options. That gives you the potential to make huge profits if these stocks rebound strongly (which they usually do).

What's your risk? Well, assuming you've picked four conservative, high-quality businesses, your risk is that you will end up buying some of these shares. That will require more capital. But if you've done your homework, there's no real downside, because these are businesses you wanted to own anyway, and you're buying in at incredibly low prices.

![]() So... let's consider those numbers. If your Alpha strategy campaign goes off without a hitch next year, you will earn an extra $16,000 in essentially risk-free profits on your $100,000 account. And you will have made income using only a small fraction of your capital ($12,000).

So... let's consider those numbers. If your Alpha strategy campaign goes off without a hitch next year, you will earn an extra $16,000 in essentially risk-free profits on your $100,000 account. And you will have made income using only a small fraction of your capital ($12,000).

Using volatility like this can dramatically increase the amount of income your portfolio produces. During periods of market stress, that's incredibly important. You will want as much cash as you can generate because there will be so many fantastic long-term opportunities to buy great businesses.

That's assuming that none of your call options end up in the money. If you take just a fraction of this income (say, $1,000 out of each $4,000 earned) and speculate in out-of-the-money call options, if just one of them hits, you'll probably double your returns. Instead of making $4,000 in each cycle, you could wind up making $8,000.

That's the beauty of this approach. There are lots of ways to win, and almost no ways to lose.

Please plan to join us at tomorrow's free, live webinar to learn more about this incredible strategy. You can sign up here.

![]() New 52-week highs (as of 12/15/15): Bristol-Myers Squibb (BMY).

New 52-week highs (as of 12/15/15): Bristol-Myers Squibb (BMY).

![]() Please continue to send your questions about this strategy to feedback@stansberryresearch.com.

Please continue to send your questions about this strategy to feedback@stansberryresearch.com.

Regards,

Porter Stansberry

Baltimore, Maryland

December 16, 2015

|