The most crowded party... Mutual funds go to Silicon Valley... Why startup investing will crush individual investors... Hot IPO tips!... David Stockman crushes Tesla... Germany issues negative-yield debt... JPMorgan is charging depositors to park cash...

"This is the most crowded party that's ever been thrown," Bill Gurley told the Wall Street Journal at the recent Goldman Sachs technology conference.

"This is the most crowded party that's ever been thrown," Bill Gurley told the Wall Street Journal at the recent Goldman Sachs technology conference.

Gurley, a partner at venture-capital firm Benchmark, was warning about the huge institutional interest in funding Silicon Valley startups like on-demand transportation service Uber... a high-risk, high-reward market traditionally dominated by niche venture capital (VC) investors.

Gurley knows a thing or two about VC investing. Benchmark has been doing deals since 1999. It invested in Uber (worth $40 billion), social-media app Snapchat ($19 billion), online-reservation firm OpenTable, online real estate company Zillow, and a handful of other companies worth more than $1 billion.

Though Gurley's speech was a warning to the audience, attendees were still salivating at the huge profit opportunities in the sector. The Wall Street Journal reports...

|

This is how bubbles get started...

Venture-capital firms provide startups with early-stage money. They make some huge, 1,000-times returns in companies like Facebook, Twitter, and Uber.

Tempted by massive riches, more traditional institutional investors like hedge funds and large family offices get involved. They make a fortune financing these companies in later rounds.

The public catches on... stories of Silicon Valley riches dominate the headlines. They want in on the action, not satisfied with merely tripling their money tracking the S&P 500 since 2008. They want the BIG money.

First, investment bank Goldman Sachs secures a $1.6 billion chunk of Uber's convertible debt to share with its clients (which happened in January)... The capital raise values the transportation service at more than $40 billion.

Goldman's clients don't care. They want to buy Uber – the hottest startup in the world – before it goes public. They'll pay any price.

Then, these deals flow down to you, the individual investor...

Four or five rounds later, the easy money is gone from these skyrocketing startups. But given the frenzy to invest, mutual funds start sniffing around... Yes, the same mutual funds you probably hold in your 401(k). As Gurley put it in his speech, these investors suffer from "FOMO," or fear of missing out.

Then, money managers swarm VC investors at conferences... moments after they've warned against investing in startups. It always ends the same way: poorly.

Gurley says the new investors don't understand the risks involved. They're investing in these companies as if they're the new initial public offerings (IPOs)... But not all these companies are IPO quality. "Would you hand a teenager $200,000?" Gurley asked. Venture capitalist Kamal Ravikant of Evolve VC spoke at our conference in Los Angeles last year. Kamal has worked on several startups (including one that went public) since the late 1990s. And he has made investors big profits in Evolve.

He gave the audience a primer on VC investing... and why, despite the headlines, it's much harder than it looks. He said...

|

Most investors don't have the stomach to watch 90% of their investments fail (which would be the case if mutual funds started investing in startups)... They can't withstand that kind of volatility.

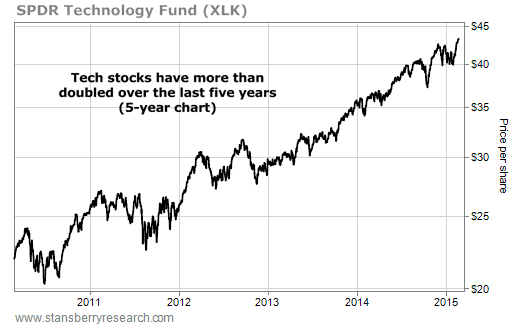

And as for the mutual-fund managers who said big tech stocks aren't "delivering enough growth"... here's a five-year chart of the tech-stock fund XLK. It holds the biggest names in technology, like Apple, Google, Intel, and Microsoft.

It has provided investors with a decent return of late...

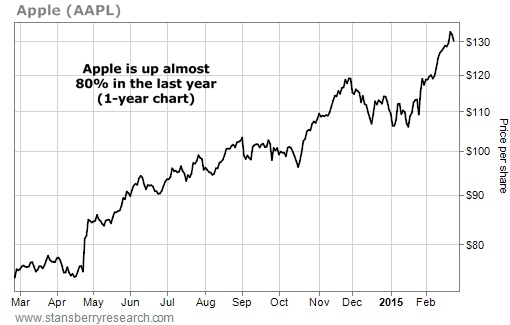

Now, let's just look at the performance of Apple – the largest publicly traded company in the history of the world – over the past year...

Now, let's just look at the performance of Apple – the largest publicly traded company in the history of the world – over the past year... Greed will prevail. We'll see more and more capital flow into speculative startups... Already, according to the Wall Street Journal, there are 73 private companies with a valuation of more than $1 billion.

Greed will prevail. We'll see more and more capital flow into speculative startups... Already, according to the Wall Street Journal, there are 73 private companies with a valuation of more than $1 billion.

Extreme Value editor Dan Ferris e-mailed us yesterday to point out that a company is starting a daily letter touting the latest IPOs. Longtime Digest readers know we're skeptical...

One sign of the market's thirst for "hot tech stocks" is the fact that Tesla still sports a $26 billion market cap.

Like most IPOs, we're also against Tesla. Our reasons are numerous. We shared some thoughts on the company in yesterday's Digest, including a recent report from a Bank of America Merrill Lynch analyst saying the stock will fall from its current levels of $206 per share to $65.

Today, we saw a bearish essay on the company from David Stockman, a former congressman, budget director under the Reagan administration, and partner of private-equity firm Blackstone Group.

Today, Stockman is an outspoken opponent of the current monetary policy. He argues that Tesla and its sky-high valuation are a product of a money-printing Federal Reserve.

He wrote an essay for our friends at Casey Research (which you can read here). We've excerpted bits from the essay below...

|

Like us, Stockman notes Tesla's inability to make a profit...

|

Stockman says that Tesla only exists because it got a $500 million bailout from the U.S. government... and it's taking advantage of low interest rates and the Fed's money manipulation to raise more and more capital (like the startups Gurley discussed above). But can you blame investors for shifting their capital into these types of companies? When governments debase currencies, the people lose faith in their money. They spend recklessly. They gamble. How would you characterize Fidelity investing in Silicon Valley startups anything other than gambling? Consider the alternatives...

Today, for the first time in history, the German government sold five-year bonds with a negative yield.

The country sold 3.28 billion euros of bonds due in April 2020 at an average yield of negative 0.08%. Finland sold similar debt earlier this month yielding negative 0.02%.

And while it's not negative, Irish 10-year debt yields less than 1% today. The U.S. government pays double what Ireland pays to borrow money for 10 years.

As we've discussed before, there's tons of government debt with negative yields today. Central banks are cutting rates to force investors into riskier assets. We're already seeing some money flow that way... But there's plenty more where that came from.

And it's not just the central banks...

Banking giant JPMorgan will now charge some large depositors to hold their cash.

Since the financial crisis, regulators have forced banks to hold more high-quality assets that they could quickly convert into cash during times of crisis. Because large uninsured deposits would likely be the first money out the door, banks are required to hold reserves against that money. Because it can't use those deposits for lending, it's no longer profitable for the bank to hold them.

"The world has changed," Jerome Schneider, managing director at PIMCO, told the Wall Street Journal. "Investors who want their cash to be safe no longer have a free ride."

JPMorgan plans to cut around $100 billion of these deposits by year's end.

For now, people will accept slightly negative rates to safely park their cash. But we'll hit a point where negative yields get egregious. The money will leave. And we'll see a massive wave of cash flow into stocks.

New 52-week highs (as of 2/24/15): Automatic Data Processing (ADP), Becton Dickinson (BDX), Cempra (CEMP), CME Group (CME), Dollar General (DG), Express Scripts (ESRX), Expeditors International of Washington (EXPD), WisdomTree Europe Hedged Equity Fund (HEDJ), iShares Core S&P Small-Cap Fund (IJR), SPDR S&P International Health Care Sector Fund (IRY), iShares U.S. Home Construction Fund (ITB), 3M (MMM), Altria (MO), PowerShares Buyback Achievers Fund (PKW), PowerShares QQQ Fund (QQQ), PowerShares Ultra Technology Fund (ROM), ProShares Ultra S&P 500 Fund (SSO), Cambria Shareholder Yield Fund (SYLD), and Walgreens (WBA). A bit of kudos for Kim Iskyan's latest issue of Global Contrarian in today's mailbag. Have you enjoyed a specific piece of our editorial lately? Drop us a line to tell us about it at feedback@stansberryresearch.com. Just wanted to compliment you on your Singapore article [from this month's issue of the Global Contrarian]. I have been doing business in S'pore for over ten years and have a few friends there. I have never seen a more accurate description of the place than your article. Stansberry readers have probably only ever encountered glowing descriptions of Singapore as some sort of free-market libertarian utopia. That is not the whole picture, and you are discerning, sophisticated, and comprehensive in your description. Really good work." – Paid-up subscriber Marc Elardo

Goldsmith comment: Kim has been doing a great job with the Global Contrarian. In the last six months alone, he has visited Singapore, Sri Lanka, Venezuela, Myanmar, and Macau. We'll share an excerpt from Kim's latest issue in an upcoming Digest.

Regards,

Sean Goldsmith

Delray Beach, Florida

February 25, 2015