The rout continues... Copper is falling... Iron ore is getting crushed... But production is still increasing... Dan Ferris is bullish on commodities... Has the dollar peaked?... Commodities will rally...

The rout in commodities continues...

The rout in commodities continues...

We're becoming bullish on certain commodities, which we'll discuss later. But for now, we're still on the sidelines with some industrial metals...

Copper prices sit at around $3.05 a pound today... just pennies away from a new four-year low. It's a huge move for a commodity that hit $4.63 a pound in early 2011.

Copper has widespread uses in most sectors of the economy. It conducts heat and electricity. It's used in building materials, manufactured goods, and as an ingredient in various metal alloys, among other applications.

And despite falling prices, the copper supply is in deficit. According to intergovernmental organization International Copper Study Group (ICSG), new copper projects coming online are slowing down.

ICSG expects world copper production to grow 3% in 2014 to 18.6 million tons. That's a significant slowdown from the 8% growth rate in 2013.

Meanwhile, demand in China – which accounts for 40% of the world's copper demand – is still holding strong... and expected to increase 7% this year (versus 3.5% growth in demand across the rest of the world).

As a result, ICSG anticipates copper supply to have a deficit of 307,000 tons in 2014. This would mark the fifth straight year where demand exceeded supply.

Copper is often referred to as "Dr. Copper" because its demand can be a reliable leading indicator of economic health. Thus, it can signal turning points in the global economy.

Usually, rising copper prices suggest strong copper demand and a growing global economy, while falling copper prices indicate an economic slowdown.

Today, Dr. Copper is telling us we're in an interesting situation where demand is heading higher, but prices are heading lower. We're not saying the bottom is in... But we're keeping an eye on copper.

Backstage at our Stansberry Conference Series event in Nashville, Tennessee over the weekend, resource expert Rick Rule told us he's bearish on iron ore prices – even though prices are already in the dumps.

Iron ore faces a 30%-40% global oversupply. In addition, growth in China – which consumes more than 60% of global iron ore – is slowing.

Iron ore is a low-margin, "boring" commodity... It wasn't until the China growth story gripped the world that prices boomed.

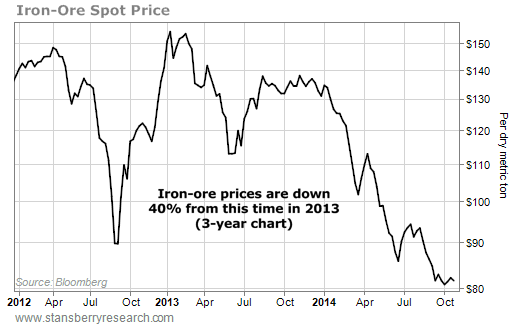

Just take a look at this chart...

Iron-ore prices have fallen to around $80 per metric ton today... a 40% drop from a year ago.

Iron-ore prices have fallen to around $80 per metric ton today... a 40% drop from a year ago.

And it's crushing iron-ore miners like Cliffs Natural Resources (CLF), which recently wrote down $6 billion mostly in relation to its purchase of a Canadian iron-ore mine.

It cost Cliffs $87.50 per ton to mine ore from its Eastern Canada operations in the second quarter... But prices were around $80 a ton. Cliffs lost $88.2 million in the first half of 2014.

Plus, the biggest producers – BHP Billiton (BBL) and Rio Tinto (RIO) – are ramping up production.

According to a recent article from the Financial Times, Rio Tinto is aiming to increase annual production to 360 million tons in 2015. Meanwhile, BHP Billiton – which is expected to produce around 230 million tons of iron ore this year – is looking to increase annual production capacity 30%, to 290 million tons, by 2017.

As Mike Henry, resource giant BHP Billiton's head of marketing, recently told the Australian Financial Review...

|

It's the perfect example of a commodity cycle. When a commodity hits record prices, producers scramble to bring more product online to take advantage of those prices... which leads to an oversupply... which leads to lower prices. Lower prices force some producers to stop production. But eventually, prices get too cheap, demand increases, and the cycle starts all over again...

As a side note, some producers will continue producing at a loss – as we're seeing with BHP and Rio Tinto – because it's either too expensive to close a mine, or they think they can outlast their struggling peers and have plenty of supply available for when the cycle picks up again.

We're not willing to try and pick the bottom in iron ore. Rick still thinks it has further to fall from here. There are better, safer opportunities in commodities today. At least, that's what several Stansberry Research analysts are saying...

As Dan Ferris explained in the October 17 DailyWealth...

|

Dan showed DailyWealth readers the three biggest tools you need to be a successful contrarian investor and buy commodity stocks today. You can read his piece for free right here.

S&A Short Report editor Jeff Clark also thinks commodities are a good buy today.

Commodities trade opposite of the dollar. When the dollar peaked in February, it coincided with a bottom in commodities. Between February and May, the dollar fell 4%... sending some commodities up 20%. But since May, the dollar is up about 8%, which has sent commodities tumbling lower.

Jeff says the dollar peaked in late September... which coincided with a bottom in commodities...

|

The decline in commodities has created a huge trading opportunity, according to True Wealth editor Steve Sjuggerud.

In the most recent issue, Steve urged subscribers to make two commodity trades with massive upside. He noted that stocks and real estate have soared over the past few years, but commodities in general have suffered big declines... and almost everyone has given up on the idea of owning them today. As he explained...

|

Steve also pointed out that commodities are currently trading near their all-time lows...

|

As we often say, the biggest gains come when depressed assets go from "bad to less bad." When everyone has given up on an asset, it becomes very cheap. When things get just a little "less bad," the super-depressed asset shoots up like a coiled spring.

In the latest issue of True Wealth, Steve recommended two commodity trades. One has triple-digit upside potential and just 7% downside risk. The other could return nearly 40% in the next six months.

You can access Steve's latest issue with a four-month, 100% risk-free trial subscription to True Wealth. Click here to learn more.

New 52-week highs (as of 10/22/14): CVS Health (CVS) and Altria (MO).

It seems that the people who attended our Stansberry Conference Series event over the weekend in Nashville, Tennessee enjoyed themselves. In today's mailbag, two subscribers share their experience... and another asks for the best crab cake in Baltimore. Drop us a note with your opinion on either topic at feedback@stansberryresearch.com.

"I wanted to provide my feedback regarding the conference in Nashville. I took advantage of the fact that it was only a 2-hour drive from my home and, although the prices of the various hotels caused a bit of sticker shock, the ability to drive made attendance an option I could easily afford. Although the speakers were excellent (where else would you get to see a lineup that included Ron Paul, Bill Bonner, Rick Rule and James Rickards?), I was a little disappointed that much of the information was a repetition of information that I've read from my various Stansberry subscriptions. But I guess that also shows you've done a good job of providing some excellent information in your newsletters.

New 52-week highs (as of 10/22/14): CVS Health (CVS) and Altria (MO).

It seems that the people who attended our Stansberry Conference Series event over the weekend in Nashville, Tennessee enjoyed themselves. In today's mailbag, two subscribers share their experience... and another asks for the best crab cake in Baltimore. Drop us a note with your opinion on either topic at feedback@stansberryresearch.com.

"I wanted to provide my feedback regarding the conference in Nashville. I took advantage of the fact that it was only a 2-hour drive from my home and, although the prices of the various hotels caused a bit of sticker shock, the ability to drive made attendance an option I could easily afford. Although the speakers were excellent (where else would you get to see a lineup that included Ron Paul, Bill Bonner, Rick Rule and James Rickards?), I was a little disappointed that much of the information was a repetition of information that I've read from my various Stansberry subscriptions. But I guess that also shows you've done a good job of providing some excellent information in your newsletters.

"But for me, the highlight of the conference was Lindsay Lou and the Flatbellys! I'm not sure who at S&A was responsible for finding this gem of a bluegrass//contemporary string band out of Michigan, but please extend my thanks for the introduction to such a talented group of musical artists! I picked up a couple of their CDs at the conference and have been playing them non-stop since the weekend." – Paid-up subscriber Dr. Sandra L. Kilpatrick

"Streamed the Nashville conference this past weekend – very good presentation by Amber Lee Mason. Every word carefully chosen, no wasted palaver, somewhat nervous only added to humility quotient (rare these days) – I would have bought whatever she recommended. So when it turned out to be NOBL, I saw the ball sail over the fence and out of the park. My young daughter will be rich at 50 (from investments alone) because of Mason. Nice job hiring that one!" – Paid-up subscriber L.A.F.

"Hello, I am visiting Baltimore for the Remodelers Show, and wanted to get your opinion on the best place to get crab cakes in town. Also, do you allow visits to your office? Thanks!" – Paid-up subscriber Eddie Casanave

Goldsmith comment: The best crab cake is one of the most debated topics in town. You can't go wrong with Faidley's in Lexington Market. Just be sure to go during the day... That area can get a little dicey at night. As for your other question... We're always grateful for our subscribers' support and enthusiasm. But per company policy, we don't host visits from our readers. But don't worry, you aren't missing much... just a bunch of hardworking folks working on their computers.

Regards,

Sean Goldsmith

October 23, 2014

The hidden costs of investing in art...

Jeff Rabin is principal and cofounder of Artvest Partners, a firm that offers investment advice for the art market, including custom strategies for acquiring and selling, financing, protecting art wealth, and passing it on to future generations.

In today's Digest Premium, he explains why investing in art is different than investing in stocks... and reveals some of the hidden costs in the art market...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

The hidden costs of investing in art...

Editor's note: Jeff Rabin is principal and cofounder of Artvest Partners, a firm that offers investment advice for the art market, including custom strategies for acquiring and selling, financing, protecting art wealth, and passing it on to future generations. In today's Digest Premium, he explains why investing in art is different than investing in stocks... and reveals some of the hidden costs in the art market...

The art market is different from any other market. It is opaque, unregulated, and illiquid. Those three aspects make it much more difficult to navigate than continuously traded markets such as stocks and bonds.

Each sector of the art market performs differently from each other. The press reports don't tell the whole story of what's actually happening. And the diversification that exists in terms of what you can collect is pretty wide-ranging – from antiquity all the way up through contemporary. Again, each sector performs differently... and the art market is also seasonal.

The art market is divided into two main categories. One is the auction market, which is approximately 50% of the traded market. Those are published prices that you can verify. If something trades in the auction market, you can see the date, the object, the description, the high and low estimates, and the "hammer price" (or sale price).

The other side of the market is the private market, which is dealers and art fairs that sell directly to the public. None of those prices are published. You may get a sense of what things sold for in the dealer community, but there's no way to verify pricing. So right off the bat, you don't know what has transpired in half of the market.

Also, because fine art is unique, it can be difficult to assess the right price to buy or sell a work of art.

The way it traditionally works in the art market is that people do comparables of a work that is coming up for sale. The way to understand the value of a specific piece is to look at other pieces by that artist or other works from a similar year, size, and medium. That way, you get a sense of the estimated sale price from the auction house or dealer.

That's a little easier when you're dealing with artists who have large bodies of work in the market. Often, the artists who have produced more works – and therefore, their works are slightly more liquid – are easier to sell and command higher prices, like Picasso and Warhol.

Pricing an object is difficult, and it's something new participants in the art market should be aware of. I strongly suggest hiring a trusted, objective advisor who will take you through how the market works and help you determine what you should pay for a particular work of art.

An advisor can also be extremely helpful in understanding how the auction process works. There's a lot of nuance with auctions. In addition to price estimates for paintings, every estimate has a reserve price. That isn't published to the community.

That's something a wise advisor would be able to work out with the auction house, which won't disclose the reserve, but you can get a better sense of what kind of interest there is from other people. The advisor can help you set a price limit, because the "hammer price" (or sale price) is just a base number. Then you'll have to add in the buyer's premium.

On an object in the $150,000 range, the premium is going to be at least another $30,000 in commission. So you would wind up spending $180,000 or more if you bought it at $150,000.

Then you have shipping and other costs like lighting and insurance. There are a lot of other costs that go into collecting art that don't exist when you buy a stock or a bond. Art is obviously a tangible asset. Tangible assets are much more time-consuming and difficult to handle.

– Jeff Rabin

Editor's note: You can learn more about Artvest and the services it provides by clicking here.

The hidden costs of investing in art...

Jeff Rabin is principal and cofounder of Artvest Partners, a firm that offers investment advice for the art market, including custom strategies for acquiring and selling, financing, protecting art wealth, and passing it on to future generations.

In today's Digest Premium, he explains why investing in art is different than investing in stocks... and reveals some of the hidden costs in the art market...

To continue reading, scroll down or click here.

Stansberry & Associates Top 10 Open Recommendations

(Top 10 highest-returning open positions across all S&A portfolios)

As of 07/21/2014

| Stock | Symbol | Buy Date | Return | Publication | Editor |

| Prestige Brands | PBH | 05/13/09 | 411.6% | Extreme Value | Ferris |

| Enterprise | EPD | 10/15/08 | 316.2% | The 12% Letter | Dyson |

| Constellation Brands | STZ | 06/02/11 | 310.5% | Extreme Value | Ferris |

| Ultra Health Care | RXL | 03/17/11 | 268.2% | True Wealth | Sjuggerud |

| Ultra Health Care | RXL | 01/04/12 | 222.2% | True Wealth Sys | Sjuggerud |

| Altria | MO | 11/19/08 | 210.2% | The 12% Letter | Dyson |

| Targa Resources | TRGP | 12/13/12 | 187.6% | SIA | Stansberry |

| Blackstone Group | BX | 11/15/12 | 179.1% | True Wealth | Sjuggerud |

| McDonald's | MCD | 11/28/06 | 178.1% | The 12% Letter | Dyson |

| Automatic Data Proc | ADP | 10/09/08 | 158.2% | Extreme Value | Ferris |

Please note: Securities appearing in the Top 10 are not necessarily recommended buys at current prices. The list reflects the best-performing positions currently in the model portfolio of any S&A publication. The buy date reflects when the editor recommended the investment in the listed publication, and the return shows its performance since that date. To learn if a security is still a recommended buy today, you must be a subscriber to that publication and refer to the most recent portfolio.

| Top 10 Totals |

| 3 | Extreme Value | Ferris |

| 3 | The 12% Letter | Dyson |

| 2 | True Wealth | Sjuggerud |

| 1 | True Wealth Sys | Sjuggerud |

| 1 | SIA | Stansberry |