What record buybacks mean... Is buying back stock a crime?... The market's biggest offenders... Dan Ferris and Meb Faber on buybacks... The largest pension fund drops hedge funds... Are hedge funds finished?...

Corporations are buying back stock at the fastest clip since the financial crisis...

Corporations are buying back stock at the fastest clip since the financial crisis...

The Wall Street Journal, citing data from market-research company Birinyi Associates, noted that "corporations bought back $338.3 billion of stock in the first half of the year, the most for any six-month period since 2007."

Some stats from the article:

"The growth in buybacks comes as overall stock-market volume has slumped, helping magnify the impact of repurchases. In mid-August, about 25% of nonelectronic trades executed at Goldman Sachs Group Inc., excluding the small, automated, rapid-fire trades that have come to dominate the market, involved companies buying back shares. That is more than twice the long-run trend, according to a person familiar with the matter...

Companies with the largest buyback programs by dollar value have outperformed the broader market by 20% since 2008, according to an analysis by Barclays PLC...

According to Barclays, companies in the second quarter spent 31% of their cash flow on buybacks, the most since 2008 and up from 14% at the end of 2009. At the end of the second quarter, nonfinancial companies in the S&P 500 index held $1.35 trillion of cash, down from a record of $1.41 trillion at the end of last year, according to FactSet."

When a company buys back shares, it reduces the number of shares outstanding... That increases the earnings attributable to each share. In other words, it's a way to goose earnings per share (EPS) without fundamental improvement in the business. It makes each share you own more valuable.

Skeptics say that's a bad thing... That share buybacks are driving the market upward. Some say it's the only reason stocks are rising today.

In an absurd op-ed in the New York Times, an economics professor from the University of Massachusetts Lowell said that stock buybacks "manipulate the stock market" and the Securities and Exchange Commission should change its rules so it can better prosecute these swashbucklers.

They're all ludicrous claims. Of course, regular buybacks over a sustained period of time are a good thing for investors. But many more things go into share-price movements than just a high volume of share repurchases. As with anything else in the market, attributing a single factor for being responsible for pushing the market higher is ignorant.

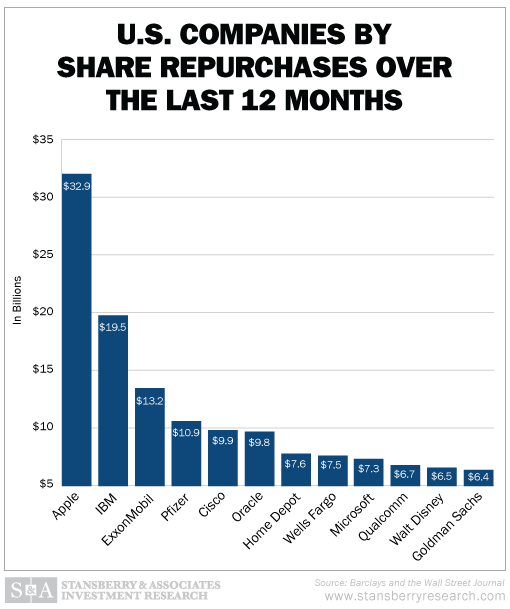

I spoke with Extreme Value editor Dan Ferris about share buybacks today. As you can see from the chart below, many of the largest share repurchasers are (or have been) in the Extreme Value model portfolio...

Dan noted the total market cap for the Wilshire 5,000 – an index of nearly all U.S.-traded stocks – is nearly $20 trillion...

Dan noted the total market cap for the Wilshire 5,000 – an index of nearly all U.S.-traded stocks – is nearly $20 trillion...

So $338 billion in buybacks isn't going to move the needle much. It's foolish to suggest that repurchasing less than 2% of the equity value over a six-month time frame will support the market or even cause it to move higher.

If a company bought back less than 2% of its shares in six months (or 4% annualized), we wouldn't expect much. We should view this about the same.

Of course, many 4% annual reductions in the outstanding share count can really add up. That's what you want to see with the individual stocks you buy. But a single 2% reduction in one six-month period doesn't seem like enough to support a $20 trillion, highly liquid market.

Dan also noted that according to data compiled by the nonprofit Investment Company Institute, annual mutual fund flows were negative every year from 2008 to 2012 (meaning more money went out than in), and only turned positive again last year. So while the market was soaring, individual investors were on the sidelines. But they've been buying for the past year and a half as the market has risen even higher.

In short, no single group can be credited with making the market go up. Corporate buyers have been known to buy more at the top, so they seem to make it fall more reliably than anything else. Individual buyers aren't pushing the market higher while they're pulling money out, as they did from 2008 to 2012.

And in June, people started taking money out of stocks again. The S&P 500 hit an all-time high three months later in September. As we've noted in the Digest, nobody has ever accused "mom and pop" of being good market timers.

I also spoke with Mebane Faber, cofounder and chief investment officer of asset-management firm Cambria Investment Management, about share buybacks.

Meb literally wrote the book on share buybacks... He wrote a book called Shareholder Yield: A Better Approach to Dividend Investing.

Shareholder yield is the total yield a company is paying investors, including both dividends and share buybacks. (Total shareholder yield also considers other ways a company can allocate capital like paying down debt or mergers and acquisitions.)

Cambria also launched the Cambria Shareholder Yield Fund (SYLD) to profit from the strategy of owning companies with high shareholder yield. Steve Sjuggerud told his True Wealth subscribers to buy shares back in May 2013. They're up 24% as of yesterday's close.

Meb told me...

|

Regarding Meb's comment about ignoring the price of a stock... Dividends are typically constant. Companies pay them out every quarter. Companies have more autonomy with buybacks. They can buy back shares when shares are expensive (which often destroys value) or when they're cheap (which often creates value).

Meb admitted CEOs as a whole are generally bad at timing buybacks. And buybacks typically follow the market cycle – meaning there are more buybacks toward market tops than bottoms – the same way mergers and acquisitions activity tracks the cycle. They're highly correlated.

That's why you should look for dirt-cheap, high-quality companies that are repurchasing shares.

You can still find plenty of reasonably priced companies buying back stock. For example, look at the biggest purchaser of stock in the market – consumer-products giant Apple – which trades for less than 17 times earnings.

Meb also noted the buyback yield for the top buyback stocks is much higher than the dividend yield right now for the S&P 500 – 5%-6% versus just 1.9%. But investors are paying a premium for dividend yield... For the first time in history, the highest dividend-yielding stocks are trading at a premium to the S&P 500 (signaling the market's desperate thirst for yield).

The important thing to remember when discussing buybacks is the opportunity cost of that capital. What's the best use of that capital today? Is it better to make an acquisition at all-time highs? Probably not... Should companies pay down the debt they just refinanced at record-low interest rates? Probably not...

We like stocks today... As billionaire hedge-fund manager Leon Cooperman says, stocks are still "the best house in the financial-asset neighborhood."

And if you look at the above infographic from the Wall Street Journal's data, the biggest share repurchasers are reasonably valued (and most have dividends much larger than the yield on 10-year Treasurys).

The other interesting story today is from one of the largest investors in the U.S. – the California Public Employees' Retirement System ("Calpers").

Calpers is a $298 billion pension fund... And it's pulling its entire $4 billion stake invested with various hedge funds and funds of funds.

In the fiscal year ended June 30, Calpers earned 7.1% in hedge funds. The S&P 500 returned 22% over the same time frame. As you can see from the following chart, hedge-fund underperformance isn't exactly a new phenomenon...

Calpers paid $135 million in fees for the privilege of that underperformance.

We've long been skeptical of the typical hedge-fund model of charging "2 and 20," or 2% of assets under management and 20% of performance. As the cost of capital has fallen over the past 40 years, it has been easy to make big gains... You borrow short-term money and buy a higher-yielding, longer-term asset. It's called a carry trade... And with a declining cost of capital, more liquidity was almost always there if you got in trouble.

But the trade got crowded... There are more than 10,000 hedge funds today controlling a record $2.8 trillion in assets.

And the game is more difficult with yields at record lows across the board.

That's why some of the greatest hedge-fund managers in history – like Stanley Druckenmiller – closed up shop... They just didn't see opportunity. Baupost Group billionaire hedge-fund manager Seth Klarman has been returning some of his firm's $25 billion in client money as opportunities wane.

The great hedge funds will survive... They have brilliant management, decades of experience, and massive pools of assets. But the peripheral players are doomed.

Guys like Meb are eating their lunch. Meb and other fund managers are getting more sophisticated. They offer hedge-fund-type strategies for a fraction of the cost.

While most hedge funds charge "2 and 20," Meb's Cambria Shareholder Yield Fund charges just 0.59%. That's less than one-third of a hedge fund's typical flat fees... and you'll pay no performance fee on your gains.

Changing gears... One of our highest-profile guests ever is appearing on The James Altucher Show on Stansberry Radio today.

PayPal founder Peter Thiel is speaking with James... They're discussing Peter's new book, Zero to One, which James says is the best business book he has read in a long time.

They'll also discuss where the next major technological innovation will be... Uber's prospects... and what Peter initially saw in Facebook founder Mark Zuckerberg when he became one of the company's earliest investors. You can listen to the interview on iTunes by clicking here.

Next week, we're airing interviews with investor and author Nassim Taleb (his excellent books include The Black Swan and Antifragile) and former U.S. Congressman and presidential candidate Ron Paul. We'll share more details when those shows are available.

If you're interested in seeing Ron Paul speak live, I hope you'll join us in Nashville on October 18 for our next Stansberry Conference.

Paul is appearing as our keynote speaker. You'll also hear from financial expert Jim Rickards, Stansberry Research founder Porter Stansberry, DailyWealth Trader editor Amber Lee Mason, and many more.

And you can still get our lowest "early bird" pricing for the event... But not for much longer. For full details, click here.

New 52-week highs (as of 9/15/14): Altria Group (MO), short position in Washington Prime Group (WPG), and W.R. Berkley (WRB).

In today's mailbag, subscribers continue the discussion of the impact of raising the minimum wage. Send your thoughts to feedback@stansberryresearch.com.

"It was with interest when I read the comments of Ken McGaha regarding the minimum wage. A few months ago this subject was being discussed in Illinois and someone brought up a similar situation from a few years ago. In a fast food restaurant, remember when the order taker asked for your drink order. Many times that order was filled by an employee. Minimum wage then takes a slight boost and now the order taker hands you a cup and you take it from there. One less position on the payroll. Ken's comments are spot on." – Paid-up subscriber Mike Kelly

"In response to raising the minimum wage, if the wage goes up to $15.00 an hour, one would think that prices will also rise so that it will be comparable to today's prices and what you can and can't buy at the minimum wage. I lived in New Zealand where the minimum wage is about $13.00 an hour (NZ dollars). But everything is just so expensive, that the people there making minimum wage are screaming for a wage increase. I imagine it's like that in every other non, third world country. I was making $65k a year, and had just enough money to make ends meet with minimal savings." – Paid-up subscriber Gary Alvarez

New 52-week highs (as of 9/15/14): Altria Group (MO), short position in Washington Prime Group (WPG), and W.R. Berkley (WRB).

In today's mailbag, subscribers continue the discussion of the impact of raising the minimum wage. Send your thoughts to feedback@stansberryresearch.com.

"It was with interest when I read the comments of Ken McGaha regarding the minimum wage. A few months ago this subject was being discussed in Illinois and someone brought up a similar situation from a few years ago. In a fast food restaurant, remember when the order taker asked for your drink order. Many times that order was filled by an employee. Minimum wage then takes a slight boost and now the order taker hands you a cup and you take it from there. One less position on the payroll. Ken's comments are spot on." – Paid-up subscriber Mike Kelly

"In response to raising the minimum wage, if the wage goes up to $15.00 an hour, one would think that prices will also rise so that it will be comparable to today's prices and what you can and can't buy at the minimum wage. I lived in New Zealand where the minimum wage is about $13.00 an hour (NZ dollars). But everything is just so expensive, that the people there making minimum wage are screaming for a wage increase. I imagine it's like that in every other non, third world country. I was making $65k a year, and had just enough money to make ends meet with minimal savings." – Paid-up subscriber Gary Alvarez

Regards,

Sean Goldsmith

September 16, 2014

Why you should mark April 29 on your calendar immediately...

True Wealth editor Steve Sjuggerud says that April 29, 2015 is when "the end" arrives.

In today's Digest Premium, he explains what will happen on this date... and predicts what it will mean for the stock market...

To subscribe to Digest Premium and receive a free hardback copy of Jim Rogers' latest book, click here.

Why you should mark April 29 on your calendar immediately...

Editor's note: True Wealth editor Steve Sjuggerud says that April 29, 2015 is when "the end" arrives. In today's Digest Premium, he explains what will happen on this date... and predicts what it will mean for the stock market...

In the July issue of True Wealth, I (Steve Sjuggerud) told my subscribers that April 29, 2015 will be when "the end" arrives. Two things can happen on this date. One is that it could be the first time the Federal Reserve will have raised interest rates since 2006. The other is that it could be the day that the massive potential gains from the election cycle end.

The election-cycle indicator is an incredibly important concept. We're about to enter year three of the election-cycle indicator on October 1. That's a bullish signal for the markets.

Those are the two big things that could lead to incredible gains in stocks. Between now and April 29 is the eighth inning of this bull market. The eighth and ninth innings are where the big gains come. The Nasdaq soared about 80% in the last five months before peaking in March 2000.

How did I come up with April 29? The Federal Reserve has a meeting that day. The Fed has been trying to tell us that it's going to wait longer and keep rates low for a long time. But I don't think that's going to happen. I think it's going to come sooner than that.

But what happens after April 29, after the Fed raises rates? Interest rates will go up and everybody will think that's the end of the game... the Bernanke Asset Bubble is over and we can't make money in stocks or real estate. The reality is, that's not true.

The last time the Fed raised interest rates, they went from about 1% to about 5% – a dramatic rise. Over that time, stocks moved 50% higher. And that's not a one-off occurrence. The fact that the Fed raises rates doesn't mean the boom has to end. In fact, history shows that it can continue and has continued in the past.

I'm sure you've heard a lot of talk about how stocks are expensive. But in our office, we think stocks are actually cheap. I think we can see bubble-like proportions in these valuations before we're done. That's what happens in the eighth and ninth innings. And it's not just stocks that can do well when the Fed starts hiking rates.

So just because the Fed will start to hike interest rates some time in 2015 – possibly as early as April – does not mean that you have to sell everything and run for the hills. That will mark the start of the ninth inning, which could run through the end of 2015.

I'm not a clairvoyant. This is just our working script, which is subject to change. But after that, you'll want to get conservative and hold cash, real assets, and precious metals.

– Steve Sjuggerud

Editor's note: Steve Sjuggerud was one of several Stansberry Research analysts to present at our Stansberry Conference event in Los Angeles. Our final event of the year will be held in Nashville on October 18. We're thrilled with the lineup, which features some of our biggest names yet... including experts on natural resources, finance, and politics. To secure your seat at a 50% discount to our normal prices, click here.

Why you should mark April 29 on your calendar immediately...

True Wealth editor Steve Sjuggerud says that April 29, 2015 is when "the end" arrives.

In today's Digest Premium, he explains what will happen on this date... and predicts what it will mean for the stock market...

To continue reading, scroll down or click here.

Stansberry & Associates Top 10 Open Recommendations

(Top 10 highest-returning open positions across all S&A portfolios)

As of 07/21/2014

| Stock | Symbol | Buy Date | Return | Publication | Editor |

| Prestige Brands | PBH | 05/13/09 | 411.6% | Extreme Value | Ferris |

| Enterprise | EPD | 10/15/08 | 316.2% | The 12% Letter | Dyson |

| Constellation Brands | STZ | 06/02/11 | 310.5% | Extreme Value | Ferris |

| Ultra Health Care | RXL | 03/17/11 | 268.2% | True Wealth | Sjuggerud |

| Ultra Health Care | RXL | 01/04/12 | 222.2% | True Wealth Sys | Sjuggerud |

| Altria | MO | 11/19/08 | 210.2% | The 12% Letter | Dyson |

| Targa Resources | TRGP | 12/13/12 | 187.6% | SIA | Stansberry |

| Blackstone Group | BX | 11/15/12 | 179.1% | True Wealth | Sjuggerud |

| McDonald's | MCD | 11/28/06 | 178.1% | The 12% Letter | Dyson |

| Automatic Data Proc | ADP | 10/09/08 | 158.2% | Extreme Value | Ferris |

Please note: Securities appearing in the Top 10 are not necessarily recommended buys at current prices. The list reflects the best-performing positions currently in the model portfolio of any S&A publication. The buy date reflects when the editor recommended the investment in the listed publication, and the return shows its performance since that date. To learn if a security is still a recommended buy today, you must be a subscriber to that publication and refer to the most recent portfolio.

| Top 10 Totals |

| 3 | Extreme Value | Ferris |

| 3 | The 12% Letter | Dyson |

| 2 | True Wealth | Sjuggerud |

| 1 | True Wealth Sys | Sjuggerud |

| 1 | SIA | Stansberry |