Why Investors Are Making a Horrible Mistake

'Wrong, wrong, wrong'... Why investors are making a horrible mistake... How to avoid falling into the latest market rally trap... And the best way to maximize your portfolio allocation today...

![]() In today's Friday Digest, I (Porter) want to start out by giving you a few numbers to consider.

In today's Friday Digest, I (Porter) want to start out by giving you a few numbers to consider.

I'm not going to tell you where these numbers come from until the end of today's Digest. Be patient. Don't cheat. Don't look ahead. There's a method to my "madness."

OK. Here are the numbers...

![]() One portfolio, which was launched in April, has earned substantial profits on every position taken (16 in all). There hasn't been a single losing investment. On average, the positions are up 61%. Adjusted for the different positions sizes, the "weighted" return is just shy of 50% in just more than three months. And one or two big outliers didn't produce these gains. Nine of the 16 investments in this portfolio have made more than 50%. Five of these investments have returned more than 70%.

One portfolio, which was launched in April, has earned substantial profits on every position taken (16 in all). There hasn't been a single losing investment. On average, the positions are up 61%. Adjusted for the different positions sizes, the "weighted" return is just shy of 50% in just more than three months. And one or two big outliers didn't produce these gains. Nine of the 16 investments in this portfolio have made more than 50%. Five of these investments have returned more than 70%.

![]() Another portfolio only recommended fixed-income investments. Fixed income is normally a "boring" asset class, with most of the profits being created by regular "coupon" payments between 6% and 8% a year. Lately, due to central bank manipulation, these coupon payments have fallen to less than 4% for virtually all types of fixed income. That has made fixed income a difficult space for investors to earn substantial returns.

Another portfolio only recommended fixed-income investments. Fixed income is normally a "boring" asset class, with most of the profits being created by regular "coupon" payments between 6% and 8% a year. Lately, due to central bank manipulation, these coupon payments have fallen to less than 4% for virtually all types of fixed income. That has made fixed income a difficult space for investors to earn substantial returns.

But this portfolio, which is less than a year old, has seen equity-like gains in every position and hasn't experienced a single loss. Investments were selected during periods of stress in the corporate bond market, allowing investors to buy bonds at a significant discount from par. This increased the average yields and allowed for capital gains.

Additionally, in some investments, a small amount of stock was built into the position, much like a convertible bond would normally be structured. All seven recommendations have earned more than 20%, producing annualized gains of 56%, without a single losing position. Can you imagine earning more than 50% in a year on the bonds in your portfolio? That's exactly what is happening here.

![]() Using a "leveraged" approach to investing in options, a third portfolio makes somewhat risky bets on stocks. This portfolio would normally experience a lot of volatility, ideally with a few really big winners offsetting a larger number of small losers. Historically, this strategy has performed very well... But lately, it has simply gone bananas.

Using a "leveraged" approach to investing in options, a third portfolio makes somewhat risky bets on stocks. This portfolio would normally experience a lot of volatility, ideally with a few really big winners offsetting a larger number of small losers. Historically, this strategy has performed very well... But lately, it has simply gone bananas.

Currently, there are 11 winning positions (out of 14). The average return across this portfolio is almost 40% on margin, with an average holding period of nearly eight months, implying investors are making more than 60% on margin annually right now with this strategy.

![]() And... in our last example... a "plain vanilla" portfolio of large-cap stocks. This portfolio holds conservative, long-term investments in high-quality operating companies across multiple sectors. This strategy, in many ways, mimics the kind of investment portfolios most people are looking for when they buy a mutual fund or a diversified exchange-traded fund.

And... in our last example... a "plain vanilla" portfolio of large-cap stocks. This portfolio holds conservative, long-term investments in high-quality operating companies across multiple sectors. This strategy, in many ways, mimics the kind of investment portfolios most people are looking for when they buy a mutual fund or a diversified exchange-traded fund.

Currently, this portfolio has 26 open positions recommended between 2012 and 2016, and two longer-term recommendations from 2006 and 2007. Across the entire portfolio of 28 stocks, only two positions are down more than 10%. Virtually every other investment is in the black. The current average return in this portfolio is more than 50%. But as many of these investments have been long-lived, the annualized return is "only" 27.6%.

![]() As many longtime subscribers have reminded me lately, I've been "wrong, wrong, wrong" about the stock market for some time. Since 2013, I've been warning that a combination of growing corporate defaults, declining earnings, and vastly overpriced bonds would – sooner or later – create historical carnage in the world's stock, bond, and currency markets.

As many longtime subscribers have reminded me lately, I've been "wrong, wrong, wrong" about the stock market for some time. Since 2013, I've been warning that a combination of growing corporate defaults, declining earnings, and vastly overpriced bonds would – sooner or later – create historical carnage in the world's stock, bond, and currency markets.

I've also been warning since 2010 that the U.S. federal government is on an insane path of total financial chaos, as our ability to even service our national debt will be wiped out when interest rates rise to "normalized" levels. Only our special status as the world's leading reserve currency (and the associated ability to legally print U.S. dollars) is keeping our government afloat.

Nothing that has happened over the last several years has changed my opinion about these matters in the slightest. Here's an update of a few of the key data points...

![]() In regards to my "End of America" forecast – that sooner or later, our government's enormous debts will become impossible to finance, resulting in a crash of the dollar and the end of the world's paper currency regime...

In regards to my "End of America" forecast – that sooner or later, our government's enormous debts will become impossible to finance, resulting in a crash of the dollar and the end of the world's paper currency regime...

- The U.S. national debt (federal) is now $20 trillion. That's more than twice as much debt we faced when Obama took office.

- Another way of looking at the debt is to compare the debt owed by the number of taxpayers. Current total is $160,000 per tax filer. Ask yourself how many of your neighbors could easily finance an additional $160,000 in debt.

- Currently, the U.S. government is spending almost $45,000 per year, per taxpayer. Can you think of anyone getting any value from the government at this price?

- Government spending in the U.S. (local, state, and federal) is now $7 trillion a year, making up 38% of the total economy. If you include all medical spending (virtually all of which is either directly or indirectly financed by governments), the amount of government spending as a percentage of our economy is well over 50%.

![]() Can you find any example in history where a government-led economy produced sustained increases to wealth or prosperity? We don't just have a debt problem... We have a government problem. Nothing is limiting the growth of the government. It has the unique ability to print money to pay for all of its debts. It's like a family that never receives its credit-card bill... so it keeps spending forever. Until one day, of course, the bill comes due.

Can you find any example in history where a government-led economy produced sustained increases to wealth or prosperity? We don't just have a debt problem... We have a government problem. Nothing is limiting the growth of the government. It has the unique ability to print money to pay for all of its debts. It's like a family that never receives its credit-card bill... so it keeps spending forever. Until one day, of course, the bill comes due.

![]() Even worse... America's dependence on debt isn't simply a government problem. Americans, who have a little more than $20 trillion in liquid savings, now privately owe a total of $17.5 trillion primarily in the form of mortgages ($14 trillion), credit cards ($1.5 trillion), and student loans ($1.4 trillion). In other words, even if the government could increase taxes substantially, you cannot get blood from a stone. America is broke... Our creditors just don't realize it yet.

Even worse... America's dependence on debt isn't simply a government problem. Americans, who have a little more than $20 trillion in liquid savings, now privately owe a total of $17.5 trillion primarily in the form of mortgages ($14 trillion), credit cards ($1.5 trillion), and student loans ($1.4 trillion). In other words, even if the government could increase taxes substantially, you cannot get blood from a stone. America is broke... Our creditors just don't realize it yet.

And of course... these figures only include the debts that exist today, where interest must be paid. The so-called "unfunded" liabilities of the U.S. government dwarf all of our existing obligations – they tally well over $100 trillion. In short, there's no way we can afford to pay for the retirement and the health care of every U.S. citizen. It cannot possibly happen.

![]() What about my more immediate concerns about a huge bubble forming in the corporate bond market? Didn't I begin warning investors in 2014 that a huge bubble had formed? Didn't I say that between 2016 and 2019 defaults would soar and lead to the "greatest legal transfer of wealth in history"?

What about my more immediate concerns about a huge bubble forming in the corporate bond market? Didn't I begin warning investors in 2014 that a huge bubble had formed? Didn't I say that between 2016 and 2019 defaults would soar and lead to the "greatest legal transfer of wealth in history"?

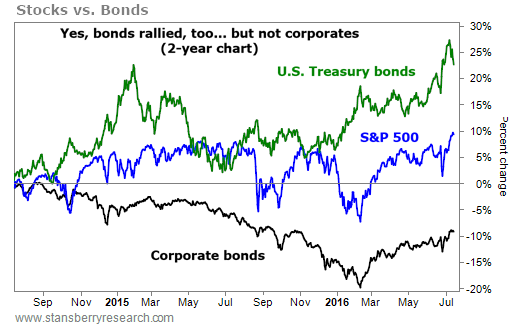

Yes, I did. And you can see in the following chart that corporate bonds (as measured by the high-yield corporate bond fund HYG) haven't made new highs, despite the rally in the stock market. Instead, government bonds are rallying, which suggests a worrisome outlook for our economy. Investors tend to buy U.S. Treasury bonds (and gold) when they're afraid to buy stocks or corporate bonds...

![]() What about my prediction about the economy slowing and a bear market beginning in June? Have you seen corporate earnings lately? As Investopedia explains...

What about my prediction about the economy slowing and a bear market beginning in June? Have you seen corporate earnings lately? As Investopedia explains...

The first quarter of 2016 marks the fourth consecutive quarter of earnings declines for the S&P 500, and earnings estimates as of June 10, 2016 are calling for Q2 2016 to make it five in a row. Since 1937, there have been 17 instances when the S&P 500's earnings declined for at least three consecutive quarters. Fourteen of those streaks were followed by a bear market within three months.

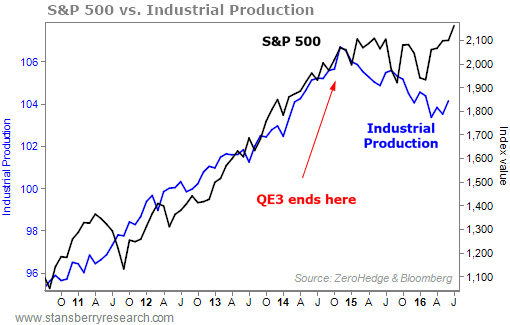

![]() Other warning signs... In the second quarter (ended June 30), industrial production in the U.S. declined at a 1% annual rate. That's the third consecutive decline in industrial production.

Other warning signs... In the second quarter (ended June 30), industrial production in the U.S. declined at a 1% annual rate. That's the third consecutive decline in industrial production.

The only thing keeping manufacturing afloat in the U.S. is automotive manufacturing, which, as you probably know from reading the Digest, is completely a function of growth in subprime auto lending (i.e. it's unsustainable).

Outside of auto, every other major category of durable materials recorded decreasing production...

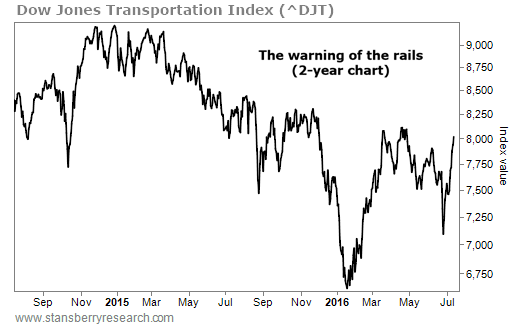

![]() One more clear economic warning: Look at the Dow Jones Transportation Average (^DJT). With less manufacturing, less stuff is being shipped around the U.S.

One more clear economic warning: Look at the Dow Jones Transportation Average (^DJT). With less manufacturing, less stuff is being shipped around the U.S.

That's a big red flag for economic growth. Unlike the major indexes, The DJT hasn't broken out to a new high yet – or even out of the downtrend it began in late 2014. (I've warned about the DJT before.) Until the shippers turn around, you can't trust the new highs we're seeing in the major indexes...

![]() For longtime subscribers who have seen these cycles before, my warnings make sense. They don't expect me to get the month the bear market will begin exactly right. They're happy to wait patiently for better investment opportunities to arise, as they know they will come.

For longtime subscribers who have seen these cycles before, my warnings make sense. They don't expect me to get the month the bear market will begin exactly right. They're happy to wait patiently for better investment opportunities to arise, as they know they will come.

But for most subscribers – and virtually all new subscribers – the fact that stocks have hit new highs after I said they would begin falling? The calls for my resignation have begun. The critics are chirping as loudly as I've ever heard in my entire career. With genuine anger and vitriol, subscribers are demanding to know how I could have gotten my market forecast so wrong.

![]() It's simple, really. Financial-research firm FactSet explains exactly what's driving this market forward, despite all of the economic warning signs. So far this year, 41 different companies have spent more than $1 billion buying back their own shares. So far this year, U.S. corporations have spent a total of $166 billion on share buybacks. That's a 15% increase over last year... and sets a new record annual pace for share buybacks.

It's simple, really. Financial-research firm FactSet explains exactly what's driving this market forward, despite all of the economic warning signs. So far this year, 41 different companies have spent more than $1 billion buying back their own shares. So far this year, U.S. corporations have spent a total of $166 billion on share buybacks. That's a 15% increase over last year... and sets a new record annual pace for share buybacks.

There are two problems with this buyback data.

First, it would be great if the stock market could be propelled like this for years. But it won't happen. Right now, the 12-month trailing buyback total is $603 billion, a figure that equals 73% of all corporate net income.

It should be obvious to everyone that if earnings keep falling (they're down about 7% year over year), buybacks can't keep growing. It should also be obvious to anyone who has ever owned or managed a business that spending more than 70% of your earnings on your shares isn't sustainable.

Second, corporate managers are terrible investors. There's a long and well-proven correlation between peaks in buyback amounts and peaks in the stock market. You'll notice that the same managers eagerly spending the corporation's cash on buying stock almost never buy the shares with their own savings.

![]() In summary... Did stocks hit a new high? Yes, the major indexes did. Does that mean that my bear market warning is wrong? No. I don't see anything that changes my mind about the HUGE risks to this market. My bet is this technical new high is going to sucker a lot of people into buying stocks at exactly the wrong the time. Don't be one of them.

In summary... Did stocks hit a new high? Yes, the major indexes did. Does that mean that my bear market warning is wrong? No. I don't see anything that changes my mind about the HUGE risks to this market. My bet is this technical new high is going to sucker a lot of people into buying stocks at exactly the wrong the time. Don't be one of them.

![]() OK, so what were all of those numbers that I reviewed at the beginning of today's Digest?

OK, so what were all of those numbers that I reviewed at the beginning of today's Digest?

Those numbers were for all of the numbskulls who have been urging me to resign (or be fired).

Those four portfolios are all of my investment recommendations. They include the recommendations I've made in Stansberry Gold Investor, which was launched in April. They include the recommendations I've made in Stansberry's Credit Opportunities, which we launched last November. They include the leveraged options recommendations I've made in Stansberry Alpha. And they include all of the open recommendations I've made in my core newsletter portfolio, Stansberry's Investment Advisory.

There's no doubt in my mind that our investment performance over the last year (and since 2014, for that matter) has been world-class in every way. In fact, there has never been a better or more lucrative time for subscribers to follow our recommendations – all of them, without any exceptions.

Our portfolios have been producing stupendous amounts of wealth for our subscribers. We've done so well because our cautious outlook led us to the right strategies and the right investment ideas for this market. As I've told you before, you can't let fears about what might happen in the markets paralyze you as an investor, because it's during times of crisis that the best opportunities emerge. Just look at what we've done over the last year for our subscribers. And when the next big opportunities emerge, don't hesitate.

![]() What should you do right now? Yesterday, a talented, well-known hedge-fund manager called me. He told me that the new highs had worried him... He felt "out of sync" with the markets. He worried that his heavy cash position was going to drag down his performance going forward if stocks rally strongly from here. He asked if I had any idea how he could get more invested now, after stocks had rallied so much.

What should you do right now? Yesterday, a talented, well-known hedge-fund manager called me. He told me that the new highs had worried him... He felt "out of sync" with the markets. He worried that his heavy cash position was going to drag down his performance going forward if stocks rally strongly from here. He asked if I had any idea how he could get more invested now, after stocks had rallied so much.

Here's what I told him...

Take a look at the All-Weather portfolio from hedge fund Bridgewater. Since 1996, this fund has produced the world's best risk-adjusted returns. It earns about 9% a year (unleveraged) but has little volatility. The maximum drawdown was less than 15% – meaning it almost never went down, not even during the financial crisis of 2008-2009. These super-safe results allow Bridgewater to "lever up" the portfolio for basically as much return as a client wants. Earning 20% a year in this fund isn't difficult and will still produce far less volatility than the S&P 500.

This kind of "risk parity" investing is the most interesting and sophisticated thing in money management. It has allowed Bridgewater to become by far the largest hedge fund in the world, managing more than $150 billion.

You can do something similar with your portfolio, if you understand the basic asset allocation model that Bridgewater uses. It keeps roughly 50% in bonds, 20% in stocks, and 20% in gold/commodities. The remaining balance is in cash.

If you're underinvested right now and afraid the market is going to rally away from you, look at your current allocation compared with Bridgewater's. Its model works in all types of markets – it doesn't require any guesswork as to what might happen tomorrow. Do you own enough bonds? Probably not. Do you own enough gold? Probably not. Do you own far too many stocks? Probably.

Again, if you feel like you're not allocated in the way you want, try making adjustments based on the Bridgewater model. You don't have to go "all the way," of course, but making small changes now to get back toward a "market neutral" position could help you in the months to come.

![]() P.S. I'm not resigning. Hope that's OK with you. And if it is, I hope you'll join us in Las Vegas this September.

P.S. I'm not resigning. Hope that's OK with you. And if it is, I hope you'll join us in Las Vegas this September.

We're excited to hear from presenters like Steve Eisman, who was the main subject of The Big Short... and Andrew Left, an activist investor who made a fortune shorting Valeant Pharmaceuticals (VRTX). We'll also hear from our friend Meb Faber and more than 30 other experts in precious metals, natural resources, entertainment, and more.

Like last year, renowned humorist and Digest contributing editor P.J. O'Rourke will be there, too. Whether you attend in person or choose to watch online, we hope you'll join us. But don't delay... our "early bird" tickets are going fast... and we're raising the prices soon. Click here for more information.

![]() New 52-week highs (as of 7/14/16): Automatic Data Processing (ADP), Aflac (AFL), First Majestic Silver (AG), Becton Dickinson (BDX), Bristol-Myers Squibb (BMY), CME Group (CME), Cisco (CSCO), Western Asset Emerging Markets Debt Fund (ESD), Fidelity Select Medical Equipment and Systems Fund (FSMEX), Cedar Fair (FUN), Johnson & Johnson (JNJ), ProShares Ultra Telecommunications Fund (LTL), Mead Johnson (MJN), 3M (MMM), Newmont Mining (NEM), Nvidia (NVDA), Pan American Silver (PAAS), PowerShares High-Yield Equity Dividend Achievers Fund (PEY), Regions Financial – Series B (RF-PB), Gibraltar Industries (ROCK), VanEck Vectors Russia Fund (RSX), Spectra Energy (SE), VanEck Vectors Steel Fund (SLX), ProShares Ultra S&P 500 Fund (SSO), and ProShares Ultra Semiconductor Fund (USD).

New 52-week highs (as of 7/14/16): Automatic Data Processing (ADP), Aflac (AFL), First Majestic Silver (AG), Becton Dickinson (BDX), Bristol-Myers Squibb (BMY), CME Group (CME), Cisco (CSCO), Western Asset Emerging Markets Debt Fund (ESD), Fidelity Select Medical Equipment and Systems Fund (FSMEX), Cedar Fair (FUN), Johnson & Johnson (JNJ), ProShares Ultra Telecommunications Fund (LTL), Mead Johnson (MJN), 3M (MMM), Newmont Mining (NEM), Nvidia (NVDA), Pan American Silver (PAAS), PowerShares High-Yield Equity Dividend Achievers Fund (PEY), Regions Financial – Series B (RF-PB), Gibraltar Industries (ROCK), VanEck Vectors Russia Fund (RSX), Spectra Energy (SE), VanEck Vectors Steel Fund (SLX), ProShares Ultra S&P 500 Fund (SSO), and ProShares Ultra Semiconductor Fund (USD).

![]() In the mailbag, at least three of our readers want me to be fired or resign. What about the rest of you? Let me know at feedback@stansberryresearch.com.

In the mailbag, at least three of our readers want me to be fired or resign. What about the rest of you? Let me know at feedback@stansberryresearch.com.

![]() "Hi Porter, yes, indeed, I think you should be fired. You have predicted everything – the best and the worst – and therefore you can always claim you were right. But it doesn't help your subscribers. Please resign." – Paid-up subscriber Gottfried Bach

"Hi Porter, yes, indeed, I think you should be fired. You have predicted everything – the best and the worst – and therefore you can always claim you were right. But it doesn't help your subscribers. Please resign." – Paid-up subscriber Gottfried Bach

![]() "I am not sure if Porter should be fired, since I do not know what his employer has asked him to do. Having said this, Porter (IMHO) is dangerous. I believe he says things for shock value and to get people to read what he says, bad news sells. An analogy would be someone saying you will die to obtain attention, of course 1 day I will die and that person will be correct. That is Porter. It is really irresponsible. You folks should disperse your information in a more professional manner. See Doc Eifrig. Sell or trade Porter to TMZ. Be well." – Paid-up subscriber F.T.

"I am not sure if Porter should be fired, since I do not know what his employer has asked him to do. Having said this, Porter (IMHO) is dangerous. I believe he says things for shock value and to get people to read what he says, bad news sells. An analogy would be someone saying you will die to obtain attention, of course 1 day I will die and that person will be correct. That is Porter. It is really irresponsible. You folks should disperse your information in a more professional manner. See Doc Eifrig. Sell or trade Porter to TMZ. Be well." – Paid-up subscriber F.T.

![]() "I wrote an earlier call for his resignation and I am more convinced after reading his latest summary rant. If he feels it's his responsibility to report these indicators of doom and gloom then why in other areas is he bullish and why do his top two advisers believe the opposite? Should the 'Two Docs' be fired then? And what value does an advisory service have when it operates like a roulette table with an equal stack of chips on each number?

"I wrote an earlier call for his resignation and I am more convinced after reading his latest summary rant. If he feels it's his responsibility to report these indicators of doom and gloom then why in other areas is he bullish and why do his top two advisers believe the opposite? Should the 'Two Docs' be fired then? And what value does an advisory service have when it operates like a roulette table with an equal stack of chips on each number?

"Fortunately for Porter he has a few good advisers for someone like me to rely on and profit from. Fact is I think I understand the Stansberry System. The sensationalizing bomb throwing carnival barker, Porter puts out one of his end-of-the-world terror predictions which suck frightened investors in and eventually they work their way through the light weights until they discover the Two Docs and start to relax, enjoy their steady, well-orchestraded earnings, and delete Porter's blathering remarks as soon as they appear." – Paid-up subscriber Thomas N.

Good investing,

Porter Stansberry

Baltimore, Maryland

July 15, 2016

|