Old-School Data Centers Are Back

Editor's note: The AI boom is creating winners beyond the stocks grabbing headlines. According to Joel Litman, chief investment officer of our corporate affiliate Altimetry, "traditional" hardware titan Dell Technologies is turning into a force in AI infrastructure. And while the stock has already soared this year, Wall Street may still be underestimating the company's growth potential...

Dell Technologies (DELL) used to be easy to label...

For decades, most folks knew it as a personal-computer ("PC") company. It sold laptops, desktops, monitors, and the hardware that filled corporate IT closets. That business still exists... bringing in tens of billions of dollars in revenue each year.

But Dell's core business has shifted fast.

Today, it's a leader in building and running servers for AI companies. Since AI and data centers have exploded in popularity, this segment has overtaken the PC segment. And it keeps crushing expectations...

Dell previously expected about $140 billion in revenue for its current 2027 fiscal year (which ends in January). Now, management says revenue should reach about $167 billion, including $60 billion from AI servers.

Shares had already climbed more than 150% before management updated its guidance. After the new outlook, the stock surged as much as 35%, pushing the rally above 200% for the year.

That's a steep gain in such a short amount of time. And investors are now worried that the rally has gone too far.

But as we'll explain today, the market is actually underestimating Dell's long-term growth potential.

Companies that use AI need a ton of gear to run their models... like cooling systems, storage, server racks, and the servers themselves.

Dell supplies much of that infrastructure.

Companies rely on Dell's expertise to quickly set up full AI systems for them. And demand is huge...

Dell booked $24.4 billion in AI orders and $16.1 billion in AI server sales in its most recent quarter. It also ended the quarter with a $51.3 billion AI-server backlog.

Those are massive figures for a company the market still thinks of as an old-school hardware name.

And the latest earnings surprise came from a more traditional part of the business...

Dell's quarterly revenue jumped 88% to $43.8 billion, far ahead of the $35.5 billion analysts expected. AI servers drove a big part of that growth. But traditional servers also nearly doubled to $8.5 billion.

Graphics processing units ("GPUs") have been the star of the AI build-out. They're the powerful calculators used to train large models. However, central processing units ("CPUs") are the brains of everyday computing systems.

CPUs can handle a broader range of tasks. That's why traditional servers are built around them. And crucially, they can run many AI models once they're trained.

As more companies move from building AI models to using them every day, demand will shift to Dell's legacy server business.

This is a major reason why the stock is soaring... And yet, the market still isn't pricing Dell for AI domination.

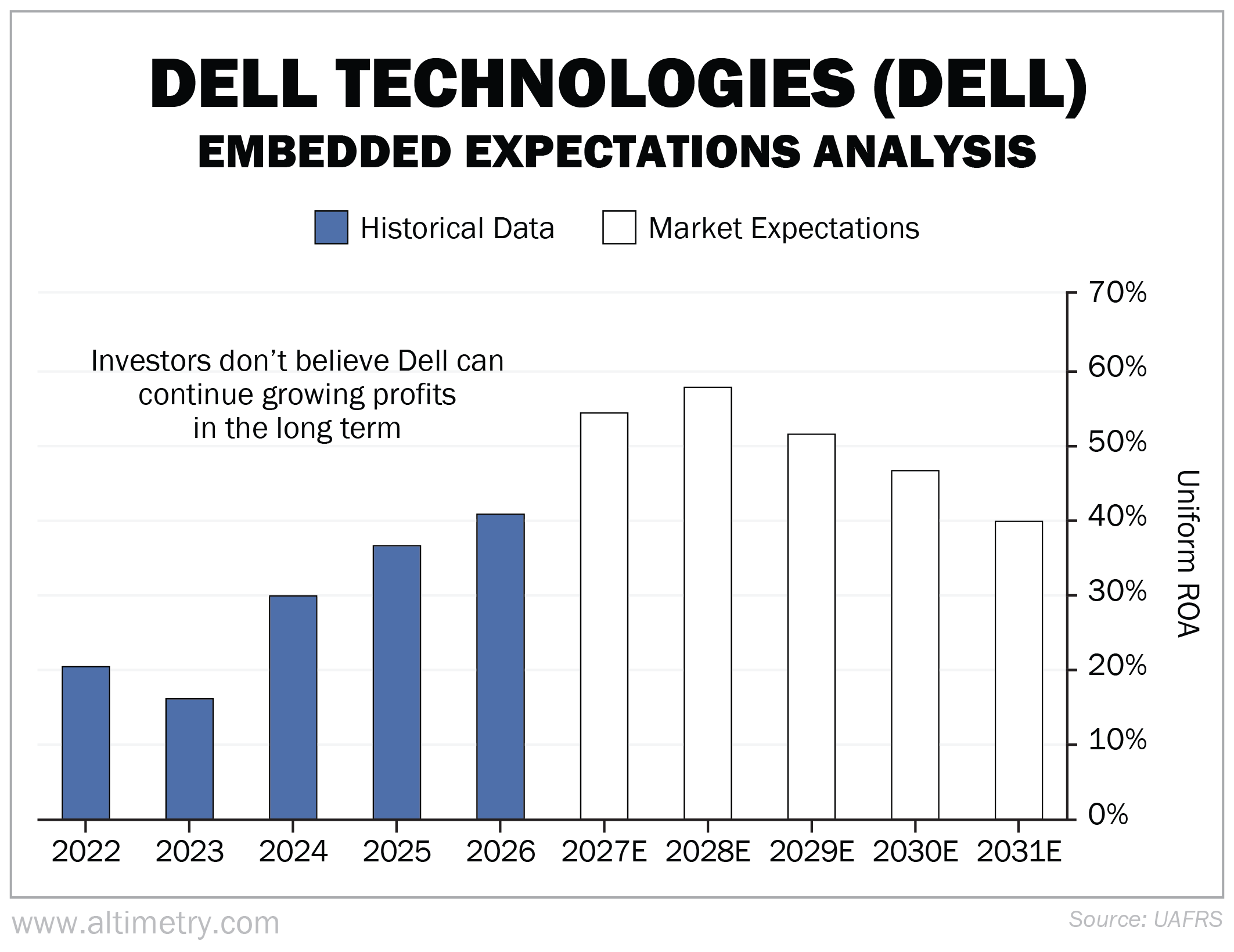

We can see this through our Embedded Expectations Analysis ("EEA") framework.

The EEA starts by looking at a company's current stock price. From there, we can calculate what the market expects from the company's future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Dell's Uniform return on assets ("ROA") has soared in recent years, reaching 40% in the 2026 fiscal year. At Altimetry, we analyze earnings with Uniform Accounting to avoid the distortions of traditional accounting methods.

Wall Street expects Dell's Uniform ROA to keep rising to 57% over the next two fiscal years as both AI servers and traditional servers keep gaining momentum.

But the market expects returns to drop back down to 40% by 2031. Check it out...

Dell beat profit expectations by a wide margin last quarter, earning $4.86 per share versus the $2.99 analysts expected. This company keeps outrunning estimates.

So the market's outlook seems much too pessimistic. And investors are still catching up to the new Dell...

Many today still view it as just a PC maker. But it sells AI servers into the hottest part of the market. And its traditional CPU-based server business is getting pulled into the next wave of demand.

The stock has already made a huge move. While sharp gains can create volatility, Dell's latest quarterly earnings show that the company is firing on all cylinders.

Overall, the market's expectations still look too muted for a company scaling this quickly. If you're looking for a way to play the AI boom, Dell still has far more room to run than the market is giving it credit for.

Regards,

Joel Litman

Editor's note: A bottleneck inside the AI boom is becoming too big to ignore. Data centers are straining America's power grid... And some experts warn that the fallout could threaten trillions of dollars in market value. That's why companies like Tesla, OpenAI, and Nvidia are racing toward a breakthrough technology that could power the next era of AI – and potentially create an entirely new class of market winners.

Further Reading

Successful long-term investing requires thinking beyond today's headlines and market swings. The real opportunity often lies in identifying companies building valuable assets and future cash flow long before the market rewards them for it.

Many of today's biggest technology breakthroughs start out messy... before becoming inevitable. Tesla's infamous "production hell" nearly broke the company. But it also helped pioneer the next generation of AI-powered automation spreading across the global economy.