A critical development in the credit markets...

A critical development in the credit markets... The 'canary in the coal mine'... Stress is spreading... These 'investment-grade' bonds could be next... Please don't wait...

Editor's note: Today, we're continuing our special holiday Digest series featuring some of the most popular essays we published in 2015. Each one covers an important idea or strategy we shared this year... and each one received a huge response from our readers.

Today's essay may be the most important we wrote all year. Originally published earlier this month, Porter shares his warnings about the credit markets... and recent signs that a real crisis is fast approaching...

![]() We begin today's Digest with a warning...It may be the most important sign yet that the credit-market problems we've been following are intensifying... and the credit-default cycle we've been predicting has begun.

We begin today's Digest with a warning...It may be the most important sign yet that the credit-market problems we've been following are intensifying... and the credit-default cycle we've been predicting has begun.

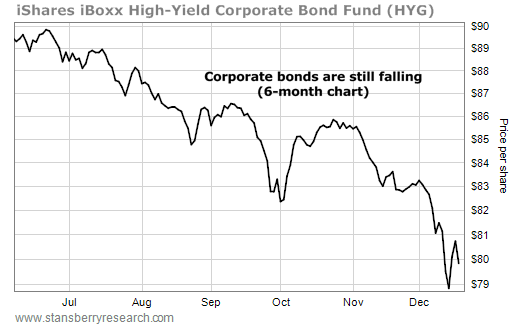

![]() As regular readers know, we've been keeping a close eye on the high-yield (or "junk") corporate-bond market.

As regular readers know, we've been keeping a close eye on the high-yield (or "junk") corporate-bond market.

Junk bonds – as represented by the iShares iBoxx High Yield Corporate Bond Fund (HYG) – have been plunging again. As you can see below, the chart of HYG is concerning...

In fact, HYG just hit a new four-year low today. But that doesn't tell the whole story...

![]() As you likely know, the corporate-bond market is divided into two large tiers by the three big credit-ratings agencies: "investment-grade" debt and "speculative-grade" (junk) debt.

As you likely know, the corporate-bond market is divided into two large tiers by the three big credit-ratings agencies: "investment-grade" debt and "speculative-grade" (junk) debt.

But each of these tiers is divided further, with each company or issuer given a rating based on its relative risk of default.

Standard & Poor's and Fitch rate investment-grade bonds from "AAA" (representing "extremely strong" capacity to service debt) through "BBB-" (representing "adequate" capacity to service debt). High-yield bonds are rated from "BB+" through "D" (representing issuers that have already defaulted). The third big credit-ratings agency – Moody's – uses a slightly different system ("Aaa" through "C"), but the idea is the same.

![]() In general, exchange-traded funds like HYG track the broad junk-bond market... representing the full spectrum of high-yield debt, ranging from the least risky to the most risky.

In general, exchange-traded funds like HYG track the broad junk-bond market... representing the full spectrum of high-yield debt, ranging from the least risky to the most risky.

But if we look at just the riskiest high-yield bonds – those rated "CCC" or lower – we can see just how critical the situation has become...

![]() While HYG has fallen to four-year lows, the riskiest high-yield debt has already plummeted to six-year lows... levels not seen since the last financial crisis.

While HYG has fallen to four-year lows, the riskiest high-yield debt has already plummeted to six-year lows... levels not seen since the last financial crisis.

Average yields for these bonds have jumped to nearly 17%, compared with "just" 8% for HYG. And as you can see in the following chart, "spreads" – the difference in yield between these bonds and U.S. Treasury securities – are skyrocketing...

.png)

This is important...

Consider this debt the "canary in the coal mine" for the corporate-bond market. These bonds are the most sensitive to problems in the credit markets, and the chart above indicates a severe amount of credit distress in the lowest-ranked bonds.

This is important because credit problems are "contagious." When companies funded with huge amounts of debt go bankrupt, it triggers a chain reaction. Stress can spread from the riskiest debt in unexpected ways. Institutions that would otherwise be sound can end up in default because they've invested in toxic debt.

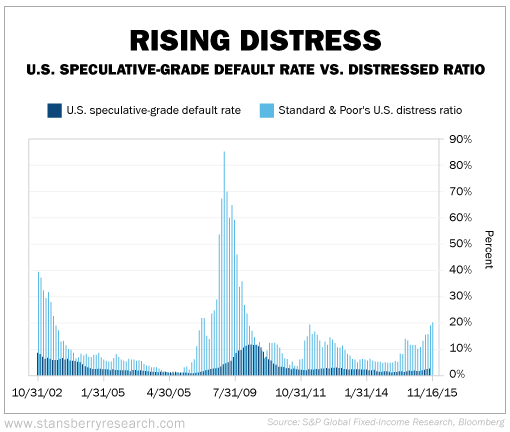

![]() And as we noted last week, the chain reaction may have already started...

And as we noted last week, the chain reaction may have already started...

According to Standard & Poor's, the firm's "distress ratio" – the percentage of high-yield bonds trading at distressed levels – has reached 20.1%. This is its highest level since 2009, when it peaked at 23.2%, and suggests the credit-default cycle has begun.

The following graphic (which uses data from Bloomberg) shows how rising credit stress precedes rising defaults...

![]() But credit "contagion" is unlikely to be contained to just the junk-bond market. Many bonds rated "investment grade" today could also be at risk...

But credit "contagion" is unlikely to be contained to just the junk-bond market. Many bonds rated "investment grade" today could also be at risk...

There has been an incredible increase in the amount of "BBB" corporate debt outstanding in recent years. As we noted earlier, this is technically investment grade. But it's the lowest tier of investment-grade debt – just one tier above "junk."

According to Jim Grant of the excellent Grant's Interest Rate Observer advisory, BBB-rated debt has grown from 14.4% of the total investment-grade market in 2008 to 30.3% this year. And this was before Bank of America, Citigroup, Goldman Sachs, and Morgan Stanley were downgraded to "BBB" last week.

![]() This is dangerous because, as a whole, investment-grade debt isn't what it used to be... It's far less resilient to economic risks. It also means that during the next credit-default cycle (which we believe has already begun) far more investment-grade debt will be downgraded to junk.

This is dangerous because, as a whole, investment-grade debt isn't what it used to be... It's far less resilient to economic risks. It also means that during the next credit-default cycle (which we believe has already begun) far more investment-grade debt will be downgraded to junk.

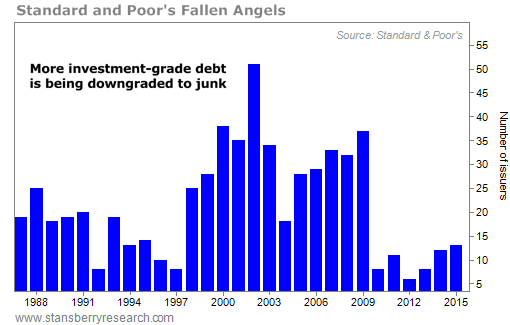

The following chart shows how many formerly investment-grade companies have already been downgraded to junk – so-called "fallen angels" – through the first eight months of 2015.

As you can see, we've already reached the highest number since 2009... and we wouldn't be surprised to see a new all-time record before this cycle ends.

This is a massive problem...

Most institutions are not allowed to own junk bonds. Thus, when some (or most) of these bonds eventually are downgraded to junk status during the next cycle, there will be a massive liquidity problem, as there are not nearly enough qualified distressed-debt investors to absorb all of the resulting "forced" selling.

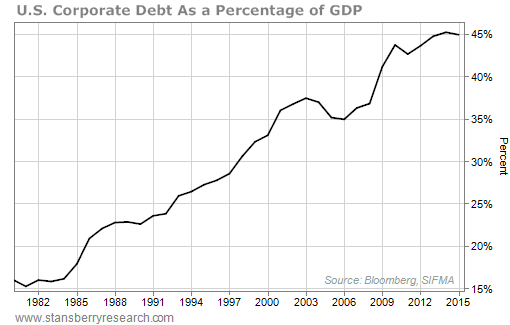

![]() To make matters worse, this fragile bond market is also the largest bond market we've ever had. The next credit-default cycle will occur in an environment of record levels of U.S. corporate indebtedness, relative to the size of our economy...

To make matters worse, this fragile bond market is also the largest bond market we've ever had. The next credit-default cycle will occur in an environment of record levels of U.S. corporate indebtedness, relative to the size of our economy...

![]() Trust me when I tell you that there's no way your stockbroker, your financial adviser, or your buddies who you talk about stocks with will be able to help you navigate this dangerous credit market.

Trust me when I tell you that there's no way your stockbroker, your financial adviser, or your buddies who you talk about stocks with will be able to help you navigate this dangerous credit market.

For most investors, the coming credit-default cycle will be a period of profound financial risk and loss. Hundreds of billions (or even trillions) of dollars will change hands.

Most of the money will be lost as bond prices crash following ratings downgrades, which will turn institutions of all stripes into forced sellers. For example, mutual funds, which hold 20% of all outstanding corporate bonds, are not prepared or set up to hold until maturity. They will not be able to ride out the crisis because their shareholders will sell – demanding liquidity in seven days from a bond market where trading will be frozen.

If you can recall the Russian default in 1998, when the bond market shut down for weeks, or the failure of Lehman Brothers in 2008, when it shut down for months, then you have an idea of what's about to happen. Only this time, it's going to be worse – simply because there's far more debt outstanding and more of it is lower-rated.

![]() In the coming default cycle (which I've called "the greatest legal transfer of wealth in history"), you will see acute distress all over the place.

In the coming default cycle (which I've called "the greatest legal transfer of wealth in history"), you will see acute distress all over the place.

That includes: student-loan securitizations, subprime-auto securitizations, commodity-related corporate bonds, retail-related corporate bonds (thanks to the "Amazon Effect," more shoppers headed to their computers on Black Friday this year than went to retail stores for the first time ever), financial firms (like Texas banks, which have far too much exposure to oil and gas firms), and emerging-market sovereign debt, as large numbers of countries devalue their currencies and default on their foreign debts.

![]() If you don't know what's happening and you don't know what to do about it, you will almost surely be a victim in this coming crisis.

If you don't know what's happening and you don't know what to do about it, you will almost surely be a victim in this coming crisis.

On the other hand... if you have access to our comprehensive research on the bond market (our analysis starts with almost 40,000 separate issues), there's no doubt in my mind that you will see the greatest investment opportunities of your life unfold. You'll be able to earn annual yields of between 10% and 25% AND make substantial capital gains of 15% to 50% (or more).

![]() If you've been following our work over the last month, you know the basics...

If you've been following our work over the last month, you know the basics...

Bonds are binary. If you can avoid default, your returns can be massive. There are also ways to build convertible-like positions where you can capitalize on both the bonds and the stock. And perhaps best of all, bonds rarely go to zero.

While we don't look to invest in bonds that default, it's inevitable that some of our ideas won't work out. When they don't, buying bonds (as opposed to stocks) generally means far less risk. If more investors understood the bond market (like we do), they would never buy stocks again.

![]() Please don't wait. Don't go into 2016 without knowing what's happening in the bond market. The risks are too high. And the opportunities are too valuable.

Please don't wait. Don't go into 2016 without knowing what's happening in the bond market. The risks are too high. And the opportunities are too valuable.

Regards,

Porter Stansberry

Editor's note: Because we want to give every reader an opportunity to take advantage of our research, we're doing something we've never done before... For an extremely limited time, we're reopening our distressed-debt service to new subscribers.

Until this Thursday, December 31 at 2 p.m. Eastern time, you have one last chance to become a charter member of Stansberry's Credit Opportunities. But please note... This is it. There will be no more extensions. This is the last time we will be offering charter subscriptions to this service.

Claim your charter subscription to Stansberry's Credit Opportunities (without having to watch a long promotional video) by clicking here.

But that's not all... Porter is also offering a select group of his best subscribers the chance to "upgrade" their subscriptions... and receive everything he and his analysts publish for life.

Subscribers who join The Porter Group today will receive LIFETIME subscriptions to Stansberry's Credit Opportunities, Stansberry Alpha, Stansberry Venture, Stansberry Data, Stansberry Radio Premium, Stansberry International, and Stansberry's Investment Advisory – plus a full list of other "goodies" – all for less than it would cost to subscribe to each of these publications for just ONE YEAR.

Even better, he'll even let you deduct every single penny you've spent on any Stansberry Research product this year from your subscription cost. And as always, this offer comes with our standard 30-day, "no-hassle" guarantee. If you change your mind for any reason, we'll issue you a full refund for every penny you paid.

If you're a serious investor, you owe it to yourself to learn more about The Porter Group now. Click here for the details.

Again, both of these offers close permanently this Thursday, December 31, at 2 p.m. Eastern time. If you're interested, please don't delay.

|