The most advanced investment skill...

The most advanced investment skill... A big secret about Ben Graham... A new way to time the market ... Don't skip ahead – there's a quiz... And don't forget: the S&A Alliance deadline is tonight at midnight...

Think of today's Digest as a test. There's a quiz at the end. As I always say... there is no such thing as teaching, there is only learning. And there's a hugely valuable lesson – the most valuable secret of all – below.

Likewise, most people know he was a successful investment manager. That's all true, of course. But most people don't know how Graham got rich. Here's a big hint: It had nothing to do with his normal method of value investing. It had everything to do with insurance.

After the purchase, the Securities and Exchange Commission (SEC) decided investment partnerships like Graham's couldn't own a controlling interest in an insurance company. To get around the rules, Graham distributed the GEICO shares among the various investors in his partnership.

Graham never sold the shares he received from the distribution. By 1972, Graham's stake in GEICO was worth $400 million. He made more than 400 times his money in 25 years. It wasn't a lifetime of careful value investing that made Graham a wealthy man... It was an investment in GEICO. Graham made vastly more money in GEICO than he made in all of his other investments combined. About 10 years after buying GEICO, Graham had made so much money that he quit investing altogether and closed his fund.

He wrote up the stock for his clients in a report titled "The Security I Like Best." The next year, Buffett sold his position for a 50% gain or so. But the lessons Buffett learned from Davidson went on to guide Buffett's entire investing career. Buffett has said publicly many times that those four hours with Davidson changed his life.

The company lost $126 million in 1975 and looked as though it might go bankrupt. The board brought in a new CEO, Jack Byrne, who radically restructured the company. He fired 4,000 of GEICO's 7,000 employees, closed down 100 offices, and exited the Massachusetts and New Jersey markets. Byrne raised insurance rates by 40%. Incredibly, in less than a year, GEICO was back in the black. By 1977, GEICO was paying a dividend again.

He got to know the CEO. He knew he could personally provide the financing required. That's a much different situation than you or me buying shares of a cheap stock and hoping it goes back up.

Following a dinner with Byrne, Buffett began to buy huge blocks of GEICO shares. The first order was for 500,000 shares at $2.12. He later provided a huge amount of capital to the company – $75 million – through a convertible bond. His cost basis for the stock through this instrument was $1.31 per share.

Buffett's money helped save GEICO. By 1980, he owned one-third of the company. GEICO represented 31% of Berkshire Hathaway's equity portfolio at the time. Like his mentor Ben Graham, Buffett was now poised to make tremendous profits. He had allocated a huge portion of his net worth into the best business he had ever found.

By 1994, Berkshire had received $180 million in dividends from GEICO – seven times more money than Buffett spent on buying the stock. Finally, in 1995, Disney bought out ABC/Capital Cities, whose shares Berkshire held. The deal gave Buffett a huge $2 billion profit. Buffett used the cash to buy the remainder of GEICO that Berkshire didn't own for $2.3 billion. By that point, Buffett had earned 48 times his initial investment in the company.

Today, GEICO's float (the amount of insurance premiums it carries) is in excess of $16 billion – up from $3 billion in 1995. If GEICO was publicly traded, it would be worth something around $20 billion. Buffett's initial $25 million investment would now be worth at least $10 billion... 400 times his initial investment.

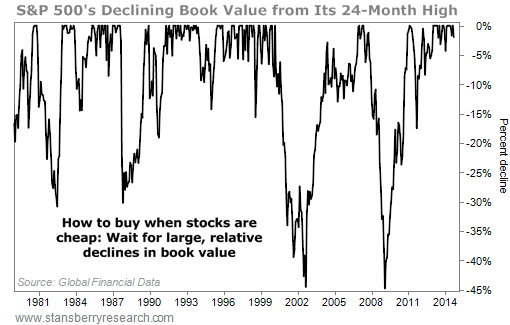

We have good data on the S&P 500's book-value ratio since 1978. This chart makes it clear when good opportunities to buy stocks existed. Longtime investors will surely be familiar with these years: 1981, 1987, 2002, and 2009...

The first was in August 1998 when Russia defaulted. Many high-quality emerging-market stocks were trading for less than four times earnings.

The second was the end of the tech-stock bubble in 2002. My Investment Advisory subscribers can read the October 2002 issue to see how I described conditions at the time. (On the first page, I asked, "Is it the end of the world?") During this period, many high-quality technology-related businesses were trading for less than the cash on their balance sheets.

The biggest, best-known market correction of my career was in late 2008/2009, when even the world's highest-quality businesses were trading at decade-low valuations. I recall analyzing shares of jewelry company Tiffany in February 2009 and realizing that the stock was worth $24 per share, assuming you just sold the inventory and used the proceeds to buy back all of the stock and pay off all of the debts.

The stock was trading at $22. Tiffany was trading below liquidation value, implying that you could get the brand name, the operating profits, the future growth, and all of the real estate for free. I doubt you'll ever see an investment as good as Tiffany's trading cheaper than that. (As a side note, Tiffany shares trade for around $96 today. The company has paid $6.44 per share in dividends. By simply buying shares in February 2009, you would be up more than 360%.)

Again, these dates will be familiar to longtime investors: 1977, 1981, 1987, 1990, 1998, 2002, 2008, and 2011. Investors become euphoric after a period of gains. They become depressed after losses. It's human nature that's being expressed in these charts.

The 2011 correction saw the S&P 500 fall 19.4%, but the ratio only declined 17.5%. This was the least impressive opportunity in our study, but that's largely because stocks were coming from a super-depressed bottom two years earlier.

In contrast, a great opportunity to buy is after the S&P 500's book-value ratio declines 30% or more, like it did in 1981, 1987, 2002, and 2008. The 1990s – a roaring bull market inspired by falling interest rates – was the only decade in my lifetime that didn't offer a great opportunity to buy stocks.

Keep in mind that if the book-value ratio of America's 500 largest companies has declined by 30% or more, you will be able to find dozens (if not hundreds) of high-quality businesses where book-value ratio has declined 50% or more.

Steve Sjuggerud achieved some of the best results in our True Wealth newsletter. (He described them in an essay published yesterday in our e-letter DailyWealth.) That's in part because we started publishing True Wealth just after the terrorist attacks of 9/11. Stocks, in general, were cheap back then. Based on our calculations, we believe investors following True Wealth would have made more than double the comparable returns of index-fund investors during that period.

We will publish all of our findings when we've completed the project – probably in conjunction with our annual Report Card. But we have made one other interesting discovery...

Folks who read both Steve's work and mine know that we have very different approaches to investing. Steve looks at the market through a "top-down" lens, trying to get into the right sectors at the right time. I look for investments in a "bottom-up" fashion, simply trying to buy good individual businesses at a good price.

Steve's three best years as an investor match the three best years I produced for my Investment Advisory subscribers. Despite following different investing strategies... we made most of our gains during the same periods.

But I decided on a compromise. I'll tell you the meaning to these stories. But first, I'd like you to send me an e-mail telling me what you thought I was driving at by sharing these items today. Remember, I was trying to teach you the most advanced skill you can possess as an investor. What's that skill? What do these lessons reinforce?

The most advanced skill you can develop as an investor is simply the emotional discipline to be incredibly patient.

If you want to succeed in investing, you have to be other-worldly in your ability to wait until you get the rarest of opportunities – a chance to buy the businesses you've always wanted at the right price.

Buffett knew all about GEICO. He saw exactly how it enriched his mentor beyond belief. He knew it would certainly enrich him (assuming he bought it at the right price). As a young man, Buffett had foolishly advertised the opportunity and, even more foolishly, he sold the stock rather than simply continuing to buy more.

He then spent the next 34 years waiting for the right opportunity to buy the company. He waited and waited and waited and waited. Then he made 400 times his money.

There's no reason you can't do the same – even if you're older than 50. Don't forget: Graham bought GEICO when he was 54. And Buffett's best investment ever was in Coca-Cola. He started buying the blue-chip soda brand after the 1987 collapse. He was 57 years old when he made that investment.

Your best opportunities may or may not arrive on schedule. Right now, I'm getting ready to recommend a new stock to my subscribers that I believe could exceed the returns I've delivered via my recommendation of Hershey – a stock I've said would be the best recommendation of my career.

The company I'm tracking today has collapsed this year. It's down 50%. It produces annual returns on equity in excess of 30%. It has been in business since the 1940s. It has had the same leadership since the 1980s. It's one of the best-managed companies in the world. And it markets an incredibly high-margin product.

Bought at today's prices, I'm extremely confident this business will compound our wealth at more than 15% a year, for decades and decades. You don't find investments like this every day... or every week, or even every year. Great opportunities are rare. You have to wait for them.

We filmed this presentation at my home. I meant every word I said in that video. I believe – without any reservation or hesitation – that joining with us in this unique kind of partnership is, by far, the smartest (and cheapest) way to do business with us over the long term. Having a partnership relationship as opposed to a client/publisher relationship allows us to do an even better job at giving you the information we would want if our roles were reversed.

Some people might cynically believe that these "deadlines" are merely a gimmick. I assure you that's not the case. The fact is, we have been planning to make radical changes to our partners offer – what we call the S&A Alliance. We are going to greatly increase the value of the offer next year. Likewise, the price of joining our partnership will increase significantly next year... probably to more than $25,000.

Those of you who have followed this program have seen us continue to create value for these partners and have seen the price to join move from less than $3,000 to more than $15,000. The next big leap forward in value is being planned for next year. Therefore, if you received one of these rare invitations... I urge you to take it.

Ultimately, my goal as a businessman is to restrict access to our research so that only partners can receive it. We aren't there just yet... But that's where we're heading. So please, join us now if you can.

Regards,

Porter Stansberry

Baltimore, Maryland

October 31, 2014

Why a combined top-down and bottom-up approach to investing works...

Editor's note: This week, we've featured commentary from Stansberry International editor Brett Aitken. In today's Digest Premium, Brett explains how his approach gives subscribers an advantage over other investors... and why buying individual stocks is the best way to profit from a bull market...

As I (Brett Aitken) have mentioned this week, we monitor almost 50 different countries to determine which ones offer the best value and opportunities for our investment capital. We also use a number of valuation metrics to tell us which countries are cheap and have potential catalysts to send stocks higher.

Consider Greece, for example. It currently sits atop our chart for the cheapest market value and highest real interest rates. During the last market boom in Greece between 2003 and 2007, if you had bought the overall Athens Stock Exchange index, you would have made 265%. That's impressive. But if you had been more selective and bought a basket of six to eight of the highest-quality Greek stocks, you would have more than doubled that.

One company in the Stansberry International portfolio is industrial conglomerate Mytilineos (MYTIL: AT). Between 2003 and 2007, investors made 2,300%... almost 10 times more than the broader index.

We aren't saying we're going to make 2,300% this time around. But we did recommend the stock when it was trading at similar levels to 2003 based on price-to-book value. We got it for cheaper than it was in 2003 based on price-to-sales and price-to-cash flow, too. Plus, a recent pullback has given interested investors the chance to buy shares for less than our maximum buy price.

Other stocks in the Stansberry International portfolio also far outpaced the Greek stock index from 2003 to 2007. This gives us an idea of the upside potential we have by finding the best individual stocks in a cheap market.

– Brett Aitken

Editor's note: Most online brokers allow investors to buy international stocks with the single click of a mouse. If you're still nervous about investing internationally, Brett created a special report, titled "How to Open a Brokerage Account to Buy Shares on International Exchanges." The report covers everything you need to know to open an account for international investing and lists reputable brokers.

To learn more about international investing – and to claim your four-month, risk-free trial to Stansberry International – click here.

Why a combined top-down and bottom-up approach to investing works...

This week, we've featured commentary from Stansberry International editor Brett Aitken.

In today's Digest Premium, Brett explains how his approach gives subscribers an advantage over other investors... and why buying individual stocks is the best way to profit from a bull market...

To continue reading, scroll down or click here.