The Specter of Inflation Is Stirring

This exclusive presentation comes down tonight... The specter of inflation is stirring... The latest on a Fed rate hike... The record M&A boom continues... What the election will do to the stock market...

We begin today with a reminder...

We begin today with a reminder...

Your opportunity to watch the exclusive presentation from technology expert Jeff Brown is almost over...

As we mentioned last week, Jeff's talk was recorded live at our private Stansberry Alliance meeting in Las Vegas last month. Typically, this information is reserved only for our elite lifetime subscribers... folks who have paid as much as $15,000 for access.

But because we believe this information is so important and potentially valuable, we arranged full access for all interested Stansberry Research readers.

However, there was one caveat: We had to promise to restrict access to this video to just a few days only... which means we must take it offline promptly at midnight Eastern time tonight.

If you haven't had a chance to watch it, we urge you to do so now.

Again, this short video is free to all Stansberry Research readers... and comes with absolutely no obligation to subscribe to Jeff's excellent research (though he is offering a substantial discount for folks who are interested).

You'll hear a short introduction from our colleague Jared Kelly, followed immediately by Jeff's complete Alliance presentation, recorded live last month.

But again, if you're interested, you must act now... This presentation will be gone in just a few hours. Simply click here to view it now.

The specter of inflation is stirring...

On Friday, the government reported the U.S. personal consumption expenditures (or "PCE") price index – the Federal Reserve's preferred measure of inflation – rose 0.2% in September, and 1.2% year over year. So-called "core prices" – which exclude more volatile food and energy prices – rose 1.7% from a year earlier.

While these measures remain below the Fed's official target of 2%, it's worth noting that they have been slowly trending up. They're now at their highest levels in nearly two years, according to the Wall Street Journal.

Meanwhile, wages may be starting to accelerate to the upside as well. Government data showed wages were up 2.4% year over year in the third quarter, the fastest pace since 2009.

It's still early, but after years of deflationary fears, it appears inflation could be stirring again.

Of course, this doesn't mean the Federal Reserve will "tighten" anytime soon. Whether or not it approves another small rate increase this year, the Fed has hinted it will let the economy "run hot" before it tightens to any significant degree.

As we've discussed, this could be terrible news for bonds... particularly those with longer-dated maturities. But it could mean trouble for stocks as well...

Stocks and bonds have been rallying together as of late. According to strategists at JPMorgan Cazenove, this is because the unprecedented rally in bonds (in addition to record-low yields) has made stocks relatively more attractive.

But they note this positive correlation could also work in reverse... and cause stocks to plunge as bond yields rise.

The chance of a December rate hike continues to grow...

Speaking of the Fed, it will announce its latest interest-rate decision following its November policy meeting this Wednesday.

While Fed fund futures – as tracked by CME Group's FedWatch Tool – show virtually no chance of Fed hikes this month, they continue to show a growing chance of a year-end move. According to CME Group, the probability of a December rate increase has now risen to nearly 78%, up from 74% since Friday.

As regular readers know, we think the fuss about the Fed's next move is largely a waste of time. As our colleagues Steve Sjuggerud and Dr. David "Doc" Eifrig have explained, history shows rising short-term rates aren't necessarily bearish for stocks or bonds.

In other words, there are plenty of reasons to be concerned about today's lofty stock and bond markets... But a tiny, 0.25 percentage-point increase in short-term interest rates is nowhere near the top of the list.

Another day, another deal...

The record-breaking merger and acquisition boom continues...

On Friday, we mentioned General Electric (GE) was reportedly considering a merger with oil-services provider Baker Hughes (BHI). By this morning, the deal was done.

The Wall Street Journal reports GE will combine its oil-and-gas business with Baker Hughes to create a new publicly traded company that will be 62.5% owned by GE and 37.5% owned by Baker Hughes shareholders. GE will also pay a special one-time cash dividend of $17.50 for each BHI share.

As we've discussed, many recent deals have faced tough scrutiny by regulators. In fact, the government rejected a previous merger agreement between Baker Hughes and fellow oil-services firm Halliburton (HAL) earlier this year. But that may not be the case this time...

The new company would have roughly $32 billion in revenue, and would add another major competitor to the oil-services industry.

Our colleague Matt Badiali, editor of the Stansberry Research Resource Report, agrees. He sent us his thoughts in a private e-mail this morning...

I love the push GE is making into oil and gas. This is an area that GE has historically been in... and it's a good time for it to expand further. The new company will be great competition for Halliburton and Schlumberger (SLB).

What the election will do to the stock market...

Finally, we know many folks are concerned about the upcoming presidential election, so we wanted to be sure you saw the latest research from our colleague Steve Sjuggerud.

Steve believes stocks could struggle for up to two years following next week's election. But you may be surprised that his reasoning has nothing to do with which candidate wins, or which party is in power. As he explained in this morning's edition of our free DailyWealth e-letter…

It turns out that the most important factor around presidents and stock prices isn't which party is in office, but what point we are at in a given president's term.

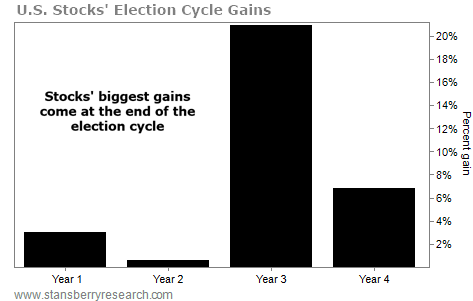

We call this powerful idea the "election-cycle indicator." The conclusion from this indicator is: Stocks tend to perform best at the end of a president's four-year term... regardless of which party is in power.

The table below shows how extreme this phenomenon has been, going back to 1950. Take a look...

As Steve noted, the chart clearly shows the biggest gains occur during the third and fourth years of the cycle. And his research shows this is the case regardless of which party is in office.

Now, we should note that these are average historical gains… and these data have varied significantly over the years. For example, while the first year has shown average gains of less than 4%, stocks have rallied as much as 43% and fallen as much as 28% in some cases.

As always, we don't recommend making investment decisions based on any single indicator. But this could be another stiff headwind for the market going forward.

|

New 52-week highs (as of 10/28/16): Alliance Holdings GP (AHGP), short position in General Growth Properties (GGP), and Nuveen Floating Rate Income Opportunity Fund (JRO).

In today's mailbag, several readers respond to confused subscriber Erica. Send your notes to feedback@stansberryresearch.com.

"Hahahaha, great response to Erica's message in Friday's Digest... there's nothing quite like a confused, hypocritical Marxist!" – Paid-up subscriber Julia

"Sounds to me like this reader may be a Groucho Marxist. Happy weekend, y'all." – Paid-up subscriber Chris K.

"Please send me instructions on how I can send gift subscriptions to 'well known Marxists' who despise you guys. I am willing to do my part to annoy any communist! I say this having studied all the great Marxist masters, Groucho, Harpo, Zeppo, etc." – Paid-up subscriber Charlie L.

Regards,

Justin Brill

Baltimore, Maryland

October 31, 2016