My recent interview; The Riskiest Bets in the Stock Market Are the Most Popular; Would-be home buyers may be forced to rent the American dream, rather than buy it; Your Worst One Percent

1) I recently did a 51-minute interview with an alternative investing platform called Prometheus. Here's a summary:

Today, we're joined by author, philanthropist, former hedge fund manager, and current investment newsletter publisher Whitney Tilson.

During our fascinating conversation, Whitney describes his childhood in Tanzania and Nicaragua, his relatively late start to investing, his long friendship with investment titan Bill Ackman, and forming his own hedge fund, Kase Capital.

At Kase, Whitney predicted and navigated both the dot-com and housing bubbles, beat the market in his first 12 years, and grew assets under management from $1 million to $200 million.

Soon after winding Kase down in 2017, Whitney pivoted and poured his considerable insights into Empire Financial Research. While subscribers to the company's eight newsletters include investment whales, most of their subscribers are average investors.

Whitney talks to us about the common mental mistakes people make with managing money, the characteristics of a good stock picker, and the "Spidey sense" he developed after more than two decades in the investing world.

You can listen to it on Apple Podcasts here or Spotify here.

2) This is madness: The Riskiest Bets in the Stock Market Are the Most Popular. Excerpt:

The ProShares UltraPro QQQ has become the most actively traded exchange-traded product this year, according to FactSet data. More than 119 million shares have changed hands on an average day this year, up 65% from last year and one of the highest levels of the past decade. Assets in the fund, known as TQQQ, have surged by 58% over the past year to about $18 billion as of Thursday. The fund has tumbled 32% in 2022, compared with the Nasdaq 100 Index's 9.6% decline...

Three of the other 10 most actively traded exchange-traded products also offer leverage or inverse exposure to the market, allowing investors to magnify their investments or bet on a fall. Assets under management in funds that provide such inverse exposure to stocks have jumped to $11.5 billion this year, up 42% from last year and the highest level since 2011, according to Morningstar Direct data as of the end of February.

I'm a fan of certain exchange-traded funds ("ETFs") – for example, the SPDR S&P 500 Fund (SPY) is by far the largest position in my personal account. But triple-levered ETFs are purely trading instruments – meaning they should only be held for a day or two – because they are virtually guaranteed to lose money over time due mainly to the high cost of the underlying options they use.

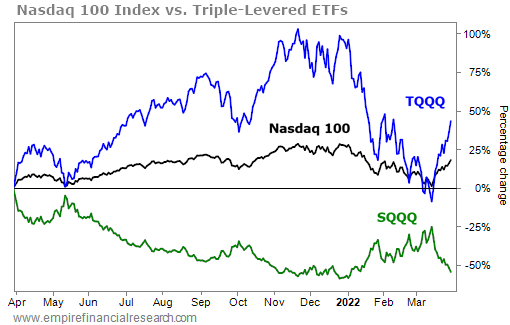

To see what I mean, take a look at this one-year chart of the Nasdaq 100 – tracked by the Invesco QQQ Trust (QQQ) – versus two triple-levered ETFs that track it, one bullish – the ProShares UltraPro QQQ Fund (TQQQ) – and one bearish – the ProShares UltraPro Short QQQ Fund (SQQQ)... meaning that if the Nasdaq 100 is up 1% on a particular day, TQQQ is designed to be up 3% and SQQQ down 3%:

Given that they're designed to be the inverse of one another, you might think that if you bought equal amounts of TQQQ and SQQQ, you'd just about break even, minus the ETFs' management fees. And at first glance at the chart, it appears that TQQQ and SQQQ are, in fact, mirror images of each other.

But upon closer examination you can see the underperformance: TQQQ is only up 40%, nowhere near triple the 18% return of the Nasdaq 100... whereas SQQQ is down 55%, capturing all of the expected downside.

In summary, my advice is not to engage in rank speculation at all, but if you insist on doing so, at least understand that these triple-levered ETFs can only be traded, not held for long periods of time.

3) This insightful story by 60 Minutes shows how owning a home, which historically has been the main way average Americans have been able to build wealth, is increasingly unaffordable, due in part to corporate buyers who rent out the houses to folks who would have preferred to buy in many cases: Would-be home buyers may be forced to rent the American dream, rather than buy it (transcript and video). Excerpt:

Every American is feeling the bite of inflation. Groceries cost more, gas costs more, everything seems to cost more. This past week, the Federal Reserve raised interest rates in an effort to tame the highest inflation in 40 years.

The cost of rent is really through the roof. Residential rents across the country went up an average of 15% last year – nearly twice the overall inflation rate. That's particularly painful for tenants, because according to Census Bureau data, they now often have to spend as much as half their total income on rent.

Why are rents rising so much? Well, it turns out that big Wall Street firms are playing a role, but we found the fundamental problem was years in the making... and will take years to fix...

With something as essential as housing in such short supply, you'd have to figure that Wall Street would see an opportunity, buying modest, single-family houses, the kind you'd see on any middle class suburban street, and then renting them out.

In places like Jacksonville, Atlanta, Charlotte, investors are buying almost 30% of the homes that are available for regular home buyers.

Here's a related segment by comedian Trevor Noah: The Housing Crisis – If You Don't Know, Now You Know.

4) I've shared this before, but it's worth sharing again...

Will Smith's "slap heard 'round the world" at the Academy Awards on Sunday night was so public and so shocking that I think it's likely that this incident – just a few seconds long – will be the main thing most people will ever remember Smith for. (NBA Hall of Famer Kareem Abdul-Jabbar had the best commentary I've read about what happened: Will Smith Did a Bad, Bad Thing.)

It would be hard to find a better case study for what I discuss in my book, The Art of Playing Defense: "You aren't judged for the way you behave 90% or even 95% of the time, but rather on your worst 1% or even 0.01%." Here's the full excerpt:

It's important to understand that you aren't judged for the way you behave 90% or even 95% of the time, but rather on your worst 1% or even 0.01%.

To my knowledge, David Sokol had never done anything unethical in his long career before his fateful purchase of Lubrizol's stock ruined him. That's all it took.

In my two decades as a hedge fund manager, I made thousands of trades. To my knowledge, all were ethical and proper, but if even one hadn't been, I could have been ruined as well.

One misjudgment is all it takes, so avoid gray areas. Never go near the line. Be ultraconservative when it comes to your integrity and reputation.

This applies to every area of life. You can be a kind and generous person almost all of the time, but if you make one blatantly racist or sexist remark (even if you're not racist or sexist), that's what you will be remembered for.

Even if you've been faithful to your spouse for decades, if you go to Vegas one weekend, get drunk, and have a one-night stand, you've likely permanently ruined your marriage.

The implications of the worst-one-percent reality are sobering. Everyone makes mistakes, but in some areas, you simply can't afford to make any.

There are many things you can do to avoid this kind of calamity. First, mistakes are far more likely if you're sleep-deprived or under physical, mental, or financial duress, so, if at all possible, avoid taking important actions or making big decisions under these conditions.

Be careful who you associate with, both personally and professionally. Their behavior and reputation will rub off on you and vice versa.

And never assume that something is private or off the record. Other than perhaps the most intimate conversations with your closest friends and family, assume that everything you write and say is being recorded and could be made public. Emails, in particular, live forever, so it's best to assume that someday they will be read by a hostile journalist, regulator, investigator, or lawyer. It's happened to me a few times, and it's no fun.

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.