Another major warning about bonds... Why we're likely to see a bear market in stocks this fall... Why we shuttered our high-yield bond publication... Get the best investment ideas live in Las Vegas this October...

![]() In May 2013, I (Porter) gave my first warning.

In May 2013, I (Porter) gave my first warning.

I told subscribers this was "the single greatest threat to your wealth you will ever face." Longtime readers might recall I was warning about the bond markets. In particular, I was pointing to the part of the market that provides financing to smaller, faster-growing firms – bonds known as "high yield," or "junk."

![]() I know most of my subscribers don't buy bonds. Most don't really understand how bonds work – at least, not in any real detail. And when most readers think about interest rates, they probably focus on mortgage interest rates or muni-bond interest rates.

I know most of my subscribers don't buy bonds. Most don't really understand how bonds work – at least, not in any real detail. And when most readers think about interest rates, they probably focus on mortgage interest rates or muni-bond interest rates.

Here's the thing, though: If you want to see the next bear market in stocks coming ahead of time, you ought to focus on the corporate-bond market. The corporate-bond market shows how much most companies pay for the capital needed to grow. For some industries, access to such financing is vital. Without a healthy corporate-bond market, some companies would drop to zero almost overnight. And that makes the cost of capital a crucial variable...

![]() Another thing that most investors don't understand about the bond markets: Interest rates (set by the bond markets) influence how stocks are priced relative to their earnings, their "valuations." Starting in 2009, the Federal Reserve intervened in the bond markets, driving interest rates lower. That has pushed stock valuations higher, and it has been a powerful driver of this bull market. Higher interest rates, on the other hand, will drive valuations lower. I believe that's likely to cause our next bear market.

Another thing that most investors don't understand about the bond markets: Interest rates (set by the bond markets) influence how stocks are priced relative to their earnings, their "valuations." Starting in 2009, the Federal Reserve intervened in the bond markets, driving interest rates lower. That has pushed stock valuations higher, and it has been a powerful driver of this bull market. Higher interest rates, on the other hand, will drive valuations lower. I believe that's likely to cause our next bear market.

![]() Here's what I wrote back in May 2013...

Here's what I wrote back in May 2013...

|

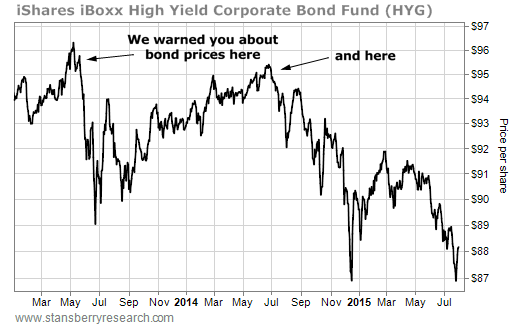

![]() One of the best ways to follow the corporate high-yield bond market is to watch the leading exchange-traded funds that buy huge amounts of corporate bonds, like the iShares iBoxx High Yield Corporate Bond Fund (HYG).

One of the best ways to follow the corporate high-yield bond market is to watch the leading exchange-traded funds that buy huge amounts of corporate bonds, like the iShares iBoxx High Yield Corporate Bond Fund (HYG).

Here's how HYG has performed since my warning in early May 2013...

As you can see, shortly after my warning, these bonds fell sharply. The funds' shares dropped from $95 to $89 in a matter of days. They rallied back, though, and roughly a year later (June 2014), they nearly hit a new high. We repeated our warnings in several Digests in 2014 (on May 29, June 4, and June 12).

Here's what we wrote in the May 29, 2014 Digest...

|

![]() That outlook led us to close our high-yield bond newsletter, True Income. There was nothing we wanted to recommend in the entire market.

That outlook led us to close our high-yield bond newsletter, True Income. There was nothing we wanted to recommend in the entire market.

Still, as interest rates raced for record lows and bond prices shot to record highs, investors decided they had to own junk bonds. While we were shuttering our high-yield bond research, the individual investor began buying junk bonds like never before... many for the first time ever. As former Digest editor Sean Goldsmith wisely noted, "Nobody ever heralded the individual investor for his timing."

![]() Today, high-yield bonds are trading near their lows of the last three years. HYG is trading around $88 a share. I still believe all the things I've written over the last two years: A collapse in the high-yield market will kill the current bull market and wipe out billions of dollars of investors' savings.

Today, high-yield bonds are trading near their lows of the last three years. HYG is trading around $88 a share. I still believe all the things I've written over the last two years: A collapse in the high-yield market will kill the current bull market and wipe out billions of dollars of investors' savings.

It's interesting to note that the rising defaults and distress in the bond market are causing the decline in bond prices today, not inflation. In particular, the two fastest-growing parts of the high-yield market for the last decade have been bonds tied to oil and gas companies (some of which have already filed for bankruptcy, many of which are now distressed) and bonds tied to subprime auto lending (which now makes up roughly 25% of all car loans).

![]() I don't need to tell you that oil and gas prices are way down. As a result, a lot of the investments made into the oil patch over the last decade aren't going to produce anything like what was expected. As oil and gas companies' "hedges" expire this year, revenues at most of America's oil and gas companies are going to go way, way down. A lot of bonds will end up in default.

I don't need to tell you that oil and gas prices are way down. As a result, a lot of the investments made into the oil patch over the last decade aren't going to produce anything like what was expected. As oil and gas companies' "hedges" expire this year, revenues at most of America's oil and gas companies are going to go way, way down. A lot of bonds will end up in default.

![]() Likewise, the default rates on newly issued subprime auto loans have been setting new highs, rates much like those in 2008. Specifically, 8.4% of the subprime borrowers who bought a car in first-quarter 2014 missed at least one payment before the end of the year. The early default rate on subprime car loans last peaked in 2008 at 9%. Given that the job market remains strong, this suggest a huge problem in subprime auto underwriting and larger-than-expected losses in securitized auto loan bonds.

Likewise, the default rates on newly issued subprime auto loans have been setting new highs, rates much like those in 2008. Specifically, 8.4% of the subprime borrowers who bought a car in first-quarter 2014 missed at least one payment before the end of the year. The early default rate on subprime car loans last peaked in 2008 at 9%. Given that the job market remains strong, this suggest a huge problem in subprime auto underwriting and larger-than-expected losses in securitized auto loan bonds.

![]() Now... consider this. Outside of student loans, auto lending is the only form of consumer lending to grow in the U.S. since 2009. And something like 30% of all the jobs that have been created in the U.S. since 2010 are tied directly to the oil and gas industry. Take the credit weakness in these industries as a significant warning sign. Perhaps all the cars they sold in 2014 (a record for U.S. car sales) can't actually be paid for... And perhaps all of those oil wells they drilled can't, either. If that's the case... no matter how many bonds the Fed buys, defaults are likely going to rise... and bonds are going to fall.

Now... consider this. Outside of student loans, auto lending is the only form of consumer lending to grow in the U.S. since 2009. And something like 30% of all the jobs that have been created in the U.S. since 2010 are tied directly to the oil and gas industry. Take the credit weakness in these industries as a significant warning sign. Perhaps all the cars they sold in 2014 (a record for U.S. car sales) can't actually be paid for... And perhaps all of those oil wells they drilled can't, either. If that's the case... no matter how many bonds the Fed buys, defaults are likely going to rise... and bonds are going to fall.

![]() What should you do about this? First and foremost, check your accounts and make sure you don't own any high-yield bonds. As for other strategies... be aware that a bear market this fall is, in my opinion, likely. Watch your trailing stops. Consider shorting a stock or two as a hedge. And most of all, avoid companies that use large amounts of debt. Their costs are going up. My subscribers can read the August issue of my Investment Advisory – out next Friday – for additional advice.

What should you do about this? First and foremost, check your accounts and make sure you don't own any high-yield bonds. As for other strategies... be aware that a bear market this fall is, in my opinion, likely. Watch your trailing stops. Consider shorting a stock or two as a hedge. And most of all, avoid companies that use large amounts of debt. Their costs are going up. My subscribers can read the August issue of my Investment Advisory – out next Friday – for additional advice.

![]() One final note... We're hosting our first multi-day conference this October in Las Vegas. If I'm right about these debt troubles, October should be a fascinating time in the markets. What better moment to meet with hundreds of fellow investors and the staff of Stansberry Research? My colleague Jamison Miller, who has been organizing this conference, has more about the shindig below.

One final note... We're hosting our first multi-day conference this October in Las Vegas. If I'm right about these debt troubles, October should be a fascinating time in the markets. What better moment to meet with hundreds of fellow investors and the staff of Stansberry Research? My colleague Jamison Miller, who has been organizing this conference, has more about the shindig below.

![]() I (Jamison) wanted to take a moment to tell you about our upcoming Stansberry Conference Series Las Vegas event. I have been to many conferences over the years, and frankly, most are not worth the price of admission. You have the same speakers from the "circuit" repeating the speech they gave two months prior at another conference. We don't want to put on a conference to recycle old ideas.

I (Jamison) wanted to take a moment to tell you about our upcoming Stansberry Conference Series Las Vegas event. I have been to many conferences over the years, and frankly, most are not worth the price of admission. You have the same speakers from the "circuit" repeating the speech they gave two months prior at another conference. We don't want to put on a conference to recycle old ideas.

That's why Porter and I have hand-picked speakers who will give short, concise presentations filled with brilliant ideas and investment advice that can truly change your life. With our lineup in Vegas, you will see world-class presentations from more than 25 speakers, including a few Stansberry Research analysts who will give presentations you won't see anywhere else.

![]() Let me show you examples of some of the presenters and what you can expect from them...

Let me show you examples of some of the presenters and what you can expect from them...

As many of you know by now, Dr. Ron Paul is our keynote speaker. He will be updating attendees on the "crisis" that could ultimately cripple the U.S. economy. By now, most of you know his grim outlook on U.S. monetary policy as we pile up debt that will be passed down to our grandchildren and their grandchildren.

Dr. Paul will be appearing on stage to have a conversation about politics, finance, and the economy with his longtime friend Mark Spitznagel, who shares Dr. Paul's passion for free markets and economics. Mark is serving as Rand Paul's senior economic advisor for his 2016 presidential campaign. He's also qualified to discuss finance... His Universa Investments hedge fund manages $6 billion in assets and specializes in protecting investors against "black swan" events in the market.

We've also invited the person we hired to run Stansberry Asset Management, Erez Kalir. Erez has worked for some of the greatest minds on Wall Street. He's presenting in Vegas to share an investment idea and will explain one of the best and safest ways to allocate your portfolio.

You'll also hear from Cannell Capital hedge-fund founder Carlo Cannell. He started his fund with a $600,000 investment and today manages more than $500 million in assets. If you attended our conference in Nashville last October, you know Carlo presented attendees with six investment ideas – three long and three short. Three of these are up more than 40% in less than a year. Carlo's contrarian views on the "efficient-market hypothesis" forms the premise of his investment philosophy. He believes that inefficient markets provide bigger potential for returns. And you'll hear some of his latest picks in Vegas.

![]() Of course, it isn't all investment advice. We hope to inspire and motivate you with presenters like Mick Ebeling and Josh Foer. Mick is the CEO of the Not Impossible Foundation, an organization of thinkers and doers who don't like to be told something is impossible. They created a product called the EyeWriter – a low-cost device that enables paralyzed individuals to communicate and create art using their eye movements. He and his team recently traveled to Sudan to 3-D print prosthetic limbs and fit them for children there. He'll share his stories and explain why he doesn't take no for an answer.

Of course, it isn't all investment advice. We hope to inspire and motivate you with presenters like Mick Ebeling and Josh Foer. Mick is the CEO of the Not Impossible Foundation, an organization of thinkers and doers who don't like to be told something is impossible. They created a product called the EyeWriter – a low-cost device that enables paralyzed individuals to communicate and create art using their eye movements. He and his team recently traveled to Sudan to 3-D print prosthetic limbs and fit them for children there. He'll share his stories and explain why he doesn't take no for an answer.

Josh Foer is a fascinating person with an unusual story. As an investigative journalist covering the U.S.A. Memory Championship in 2005, he became so fascinated that he trained, entered, and won the event in 2006.

![]() And we can't end without mentioning the Stansberry Research editors who will be giving presentations you won't find anywhere else. You'll hear from Steve Sjuggerud, Dr. David "Doc" Eifrig, Dan Ferris, and Porter. These presentations are for conference attendees only. You won't hear them anywhere else.

And we can't end without mentioning the Stansberry Research editors who will be giving presentations you won't find anywhere else. You'll hear from Steve Sjuggerud, Dr. David "Doc" Eifrig, Dan Ferris, and Porter. These presentations are for conference attendees only. You won't hear them anywhere else.

I hope you can see the time and effort we've put into hosting this world-class event. To get your ticket to this limited-capacity event for just $799, click here.

![]() New 52-week highs (as of 7/30/15): American Financial Group (AFG), Becton Dickinson (BDX), Chubb (CB), and iShares U.S. Insurance Fund (IAK).

New 52-week highs (as of 7/30/15): American Financial Group (AFG), Becton Dickinson (BDX), Chubb (CB), and iShares U.S. Insurance Fund (IAK).

![]() In the mailbag, a question about how gold stocks will perform in a market crash. What's on your mind? Let us know at feedback@stansberryresearch.com.

In the mailbag, a question about how gold stocks will perform in a market crash. What's on your mind? Let us know at feedback@stansberryresearch.com.

![]() "Porter, just finished your 7-24 Stansberry Digest and what you wrote makes sense to me, but I am puzzled. You say you expect US stocks in general to decline substantially within the next few months, yet you think that gold stocks will rise substantially over the next several years. In my experience, there is a certain bias in these markets: gold stocks can get crushed while the stock market as a whole is on a tear, because after all they are gold related and don't benefit from general stock market trends.

"Porter, just finished your 7-24 Stansberry Digest and what you wrote makes sense to me, but I am puzzled. You say you expect US stocks in general to decline substantially within the next few months, yet you think that gold stocks will rise substantially over the next several years. In my experience, there is a certain bias in these markets: gold stocks can get crushed while the stock market as a whole is on a tear, because after all they are gold related and don't benefit from general stock market trends.

"On the other hand, when stock markets get crushed, so do gold stocks, because, after all, they are stocks and get sold along with the rest by panicked investors to raise cash. I am thinking of the 2008-9 stock market, when gold stocks tumbled along with everything else, just because they were stocks. I imagined that if the debt money financial system was in danger of imploding, that gold and gold stocks might have been seen by investors as a safe haven, but they weren't. Has there ever been a time when gold stocks bucked the general stock market trend and actually did provide a safe haven from a stock bear market?"

Porter comment: Yes, there are plenty of examples in history when gold stocks (and other resource stocks) were safe havens. Look up the history of Homestake Mining during the Great Depression, for one example.

Gold plays a unique role in the modern economy. All of our fiat currency and the entire global financial system is a huge complex web of interconnected IOUs. Anyone who says he really understands the implications of a major bank or insurance company failure in our current system is lying. That's why the Fed panicked in late 2008. It had no idea what would happen if Lehman's failure led to a run on its European creditors. It had no idea what would happen if AIG failed and took Goldman (AIG's main trading partner) down with it.

I believe in the next down credit cycle, we will witness losses in the corporate-bond market in excess of $1.5 trillion (with a T). I believe this because I've studied the history of these down cycles and I've spoken with Marty Fridson (the world's leading corporate bond market analyst) about it. The Fed's actions from 2009 to 2014 "short-circuited" the normal market clearing process, which means there's far more "dodgy" debt out there than normal. There's a huge overhang of credit excess just waiting to be written-off. This vast overhang of debt is largely responsible for the weak economic rebound we've experienced – the excesses of the last cycle were never really expunged.

The big question, then, is when the Fed will allow the U.S. economy to write down these bad debts (and the associated inflated asset price levels)? I don't know the answer to that question. My bet is that they'll continue to try fighting "the last war" until there's some kind of epic collapse unlike any we've ever seen in modern times... or until there's a sea change in U.S. politics (unlikely, in my view).

In any case, when the time comes that either the U.S. begins printing huge sums of money to fight deflation (and to avoid writing down bad debts), or there's a growing uncertainty about the reliability of counter parties in the global financial system, you'll see gold prices (and gold stocks) soar. Gold is the only universally accepted financial asset that isn't someone else's liability. That's a unique trait in a world that has gone mad for debt. And I'm certain that quality will be appreciated at some point again.

Regards,

Porter Stansberry

Baltimore, Maryland

July 31, 2015

|