A Secret About Oil You Won't Find Anywhere Else

Here's a secret about crude oil supply... What the bond market is telling us today (it's not good)... In the mailbag: What Stansberry Flex can do for you...

![]() Here's a view on the situation in crude oil I (Porter) think you'll find interesting... and you won't find anywhere else.

Here's a view on the situation in crude oil I (Porter) think you'll find interesting... and you won't find anywhere else.

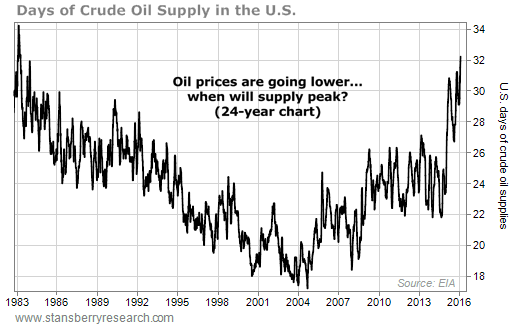

In early 1983 – the first week of February, to be precise – inventory of crude oil in the U.S. reached an all-time economic high. I say "economic high" because nominal supply of crude oil has since far surpassed its 1983 number. In fact, current U.S. crude oil inventory (504 million barrels) is the actual all-time high. Supply today is about 150 million barrels more than total supply in 1983.

Obviously, we have a lot more oil in storage than we've ever had before – about 40% more. But nominal supply numbers aren't as important as you might think. Demand for crude oil in our economy has grown a lot since 1983.

To make a bona fide "apples-to-apples" comparison to today's supply glut, we should measure the amount of supply relative to consumption. In 1983, the number of days' worth of supply in the U.S. hit a peak of 33.4. That's the largest amount of crude oil we've ever held in private storage, relative to demand. That's the all-time highest amount of "economic supply" – supply in relation to actual demand.

![]() Much like today's glut, the glut of oil from the mid-1980s was caused by a sustained increase in U.S. production. More oil was coming from Alaska's North Slope. The Trans-Alaska pipeline began operation in July 1977. It had an immediate effect on total U.S. supply.

Much like today's glut, the glut of oil from the mid-1980s was caused by a sustained increase in U.S. production. More oil was coming from Alaska's North Slope. The Trans-Alaska pipeline began operation in July 1977. It had an immediate effect on total U.S. supply.

U.S. oil production grew from 227 million barrels per month in 1977 to almost 270 million barrels per month in July 1986 – an increase in monthly production of 18.9% over nine years. As you might remember, gasoline prices fell to well below $1 per gallon... and we saw a commercial real estate and banking crisis in Texas. Houston real estate didn't recover for 20 years.

![]() In reviewing this history, it fascinated me that the peak of economic supply occurred so early in the production boom. Oil production continued to grow for another three and a half years after economic supply peaked. Why did production continue to grow so much despite the obvious glut? I'll answer that question in a minute. But first, let's consider our current boom...

In reviewing this history, it fascinated me that the peak of economic supply occurred so early in the production boom. Oil production continued to grow for another three and a half years after economic supply peaked. Why did production continue to grow so much despite the obvious glut? I'll answer that question in a minute. But first, let's consider our current boom...

Today's crude oil production boom begins back in 2005. Hurricane Katrina shut down most production in the Gulf of Mexico, resulting in U.S. crude oil production of only 120 million barrels in October 2005. Nearly 10 years later, in July 2015, U.S. production grew to 285 million barrels, an increase of 138%. In terms of nominal magnitude, our current crude oil production boom is vastly larger than the boom that triggered the 1980s glut.

But of course, consumption has also increased since 1983. Even with oil supply straining the industry's ability to store it, we are still below the record days' worth of consumption mark set in 1983 – but just barely. Currently, our supply of crude oil in private storage represents 32.2 days' worth of consumption...

Looking at supply relative to consumption, we see that we are still a long way from a bottom in crude oil prices. History shows that even after days' worth of supply peaks, oil production is likely to continue to increase for several years, pushing prices lower.

![]() So why do oil companies continue to produce oil even after prices have collapsed and oil can't be pumped profitably? Why did monthly production continue to increase for three and a half years after the last peak in days' worth of supply? There are two reasons.

So why do oil companies continue to produce oil even after prices have collapsed and oil can't be pumped profitably? Why did monthly production continue to increase for three and a half years after the last peak in days' worth of supply? There are two reasons.

First, even when oil prices don't support investments in additional supply, producing more oil may be necessary to generate cash flows to stave off bankruptcy. Operating at a loss is better than losing your oil company to creditors.

Second, most of the smaller and midsize oil companies have to hedge their production in order to qualify for their bank loans and lines of credit. According to market-research firm IHS Energy, small energy companies in the U.S. have hedged 47% of their production at prices that average $74 per barrel. Midsize firms are also relatively protected, with 43% of their oil production hedged at $60 per barrel on average. For companies that have hedged a significant amount of their production, there's still good reason to continue to produce as much oil as possible... at least, for now.

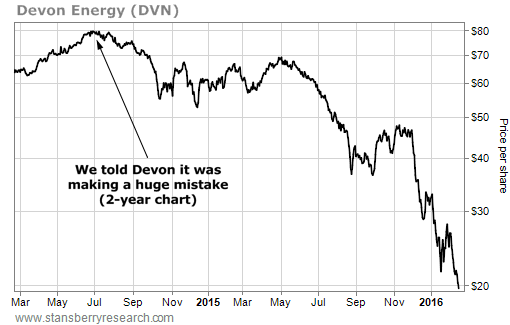

![]() Interestingly, it's the large energy firms that are most exposed to vastly lower oil prices. According to IHS, only 6% of large-company oil production is hedged. That's probably why big U.S. energy companies like Devon Energy (DVN), Pioneer Natural Resources (PXD), and Hess (HES) are being forced to raise cash through equity sales. Keep in mind, selling equity in the midst of a crisis is horrible for existing investors.

Interestingly, it's the large energy firms that are most exposed to vastly lower oil prices. According to IHS, only 6% of large-company oil production is hedged. That's probably why big U.S. energy companies like Devon Energy (DVN), Pioneer Natural Resources (PXD), and Hess (HES) are being forced to raise cash through equity sales. Keep in mind, selling equity in the midst of a crisis is horrible for existing investors.

Devon sold new shares equal to 15% of its outstanding shares at a 7.8% discount from its previous closing price. The company also announced it's cutting 20% of its workforce. The stock is now down more than 75% since we sent Devon's management an open letter (which we've "unlocked" for you right here) warning that crude prices would inevitably fall, causing huge losses on their huge investments into the Canadian oil sands...

![]() Looking at the continuing increases in supply and the industry's efforts to raise more capital (to continue pumping), we aren't close to the bottom in oil prices. So far, 48 North American energy firms have declared bankruptcy, leaving $17 billion in bad debt. I suspect the final tally of defaults will be far in excess of 10 times this number, with losses approaching the magnitude of last decade's mortgage crisis.

Looking at the continuing increases in supply and the industry's efforts to raise more capital (to continue pumping), we aren't close to the bottom in oil prices. So far, 48 North American energy firms have declared bankruptcy, leaving $17 billion in bad debt. I suspect the final tally of defaults will be far in excess of 10 times this number, with losses approaching the magnitude of last decade's mortgage crisis.

Few people have realized that the financial problems caused by low oil prices aren't going away. Everyone, it seems, expects that a quick reversal in oil production will lead to a quick drawdown in supply, and then higher oil prices. But as you can see, production isn't slowing. Supply is still growing. And supply is now at an all-time high, even when measured against consumption. This is going to be a far larger problem than Wall Street realizes.

![]() Of course, there will be a bottom in oil prices – eventually. And there will be a time to buy energy assets – eventually. But I wouldn't get near the sector until after there has been a "Lehman" moment. It's impossible to know who will end up holding the bag – Morgan Stanley? But they're still out there... holding on... hoping the tide doesn't go all the way out.

Of course, there will be a bottom in oil prices – eventually. And there will be a time to buy energy assets – eventually. But I wouldn't get near the sector until after there has been a "Lehman" moment. It's impossible to know who will end up holding the bag – Morgan Stanley? But they're still out there... holding on... hoping the tide doesn't go all the way out.

![]() Take a look at our next chart. There are three lines on the chart below. They represent the market-clearing price of three types of bonds over the past two years...

Take a look at our next chart. There are three lines on the chart below. They represent the market-clearing price of three types of bonds over the past two years...

![]() The green line, which has gone up, especially in the last few weeks, is the iShares Barclays 7-10 Year Treasury Bond Fund (IEF), an exchange-traded fund of U.S. Treasury bonds with durations between seven and 10 years. These bonds are considered a "safe haven" for investors. In times of market stress and rising bankruptcy, investors will sell corporate bonds and buy these kinds of Treasury bonds just to make sure they don't end up with a bond that defaults.

The green line, which has gone up, especially in the last few weeks, is the iShares Barclays 7-10 Year Treasury Bond Fund (IEF), an exchange-traded fund of U.S. Treasury bonds with durations between seven and 10 years. These bonds are considered a "safe haven" for investors. In times of market stress and rising bankruptcy, investors will sell corporate bonds and buy these kinds of Treasury bonds just to make sure they don't end up with a bond that defaults.

The blue line, which has gone down almost 20% over the past two years, represents the market-clearing price of a group of non-investment-grade corporate debt – the iShares iBoxx High Yield Corporate Bond Fund (HYG). Many of these issuers are small and medium oil and gas firms. The value of their bonds has been plummeting.

I've been using this fund as an indicator for several years and I've pointed it out again and again in the Digest. It's the best gauge of the actual cost of capital for most U.S. companies. These bonds are now yielding almost 10% on average, which is an indication of how expensive capital has become for most U.S. companies. I suspect that yields in this category of corporate debt will eventually reach 15% or more over the next year or two. I don't expect any sustained rally in the stock market until conditions improve in this area of the bond market.

The black line is a basket of investment-grade corporate borrowers. These are the largest, most stable, and best-financed companies in America. These bonds – as represented by the iShares iBoxx Investment Grade Corporate Bond Fund (LQD) – have fallen about 6% over the last year, a surprising decline in what is normally a very, very safe asset class.

Recently, the "spread" between Treasury bonds and investment-grade corporate bonds widened to an extent we haven't seen since the last financial crisis. This large of a divergence between the performance of Treasury bonds and investment-grade corporate bonds means that more and more big investors are becoming concerned about credit quality – even in America's best companies.

![]() Longtime readers know I've been watching the bond market for several years for signs of where stocks might be heading. The collapse in the junk-bond market last year was my No. 1 warning sign that a bear market was coming.

Longtime readers know I've been watching the bond market for several years for signs of where stocks might be heading. The collapse in the junk-bond market last year was my No. 1 warning sign that a bear market was coming.

I hope you'll keep watching the bond market and the other "lions" I've been warning you about for great insights into what's driving the equity markets lower. And I hope you've learned something this week about why it's far too early to expect a bottom in oil prices.

![]() As I frequently tell you, there's no such thing as teaching, there's only learning. About a month ago, I realized most of my subscribers simply had no idea how to manage their portfolios during a bear market. So I started to offer a very affordable ($29 per week) course that promises to teach everything I know about how to survive and prosper during bear markets.

As I frequently tell you, there's no such thing as teaching, there's only learning. About a month ago, I realized most of my subscribers simply had no idea how to manage their portfolios during a bear market. So I started to offer a very affordable ($29 per week) course that promises to teach everything I know about how to survive and prosper during bear markets.

Some of you, I would wager, didn't realize how bad the market would be in January. Some of you, I would wager, expect things will turn around shortly. I hope so... But I don't expect it, given what is happening in the bond markets (which dwarf the stock market in size).

This week's Bear Market Survival Program report is all about short-selling – something most of you will never, ever try. But you should. Shorting even 5% or 10% of your portfolio can greatly reduce volatility in your portfolio's value during a bear market by providing a hedge against downward moves. There's only one way to learn.

My advice? Study how we've been successful with our short-selling strategy and then try it. Start small. Try shorting one share and see how it goes. There's no good reason to ignore this advice, but most of you will. At $29 per report, this is the best value we've ever offered. I genuinely want to help you survive the coming bear market. Click here to get immediate access to the Bear Market Survival Program.

![]() New 52-week highs (as of 2/18/16): Franco-Nevada (FNV), Kaminak Gold (KAM.V), NovaGold Resources (NG), OceanaGold (OGC.TO), Sturm, Ruger (RGR), SEMAFO (SMF.TO), and Sysco (SYY).

New 52-week highs (as of 2/18/16): Franco-Nevada (FNV), Kaminak Gold (KAM.V), NovaGold Resources (NG), OceanaGold (OGC.TO), Sturm, Ruger (RGR), SEMAFO (SMF.TO), and Sysco (SYY).

![]() So... what kind of person are you? Are you going to put what you've learned about the markets to work for you... to protect your portfolio? Or... are you just going to watch it happen, just like it did last time a bear market wiped you out? What's it going to be? Let me know at feedback@stansberryresearch.com.

So... what kind of person are you? Are you going to put what you've learned about the markets to work for you... to protect your portfolio? Or... are you just going to watch it happen, just like it did last time a bear market wiped you out? What's it going to be? Let me know at feedback@stansberryresearch.com.

![]() In the mailbag... lots of praise for our Stansberry Flex subscription program, which allows you to get a "flexible" lifetime subscription to any five of our products. You can change your subscription elections as the market changes. It's our best lifetime offer – and we're closing it to new subscribers forever in March.

In the mailbag... lots of praise for our Stansberry Flex subscription program, which allows you to get a "flexible" lifetime subscription to any five of our products. You can change your subscription elections as the market changes. It's our best lifetime offer – and we're closing it to new subscribers forever in March.

![]() "Porter, as a member of [Stansberry] Flex, I believe it is the best value available in investing advice and training... I firmly believe that without the knowledge I have gained from your products, I would not have reached the state of financial security that I have today." – Paid-up Stansberry Flex subscriber Art B.

"Porter, as a member of [Stansberry] Flex, I believe it is the best value available in investing advice and training... I firmly believe that without the knowledge I have gained from your products, I would not have reached the state of financial security that I have today." – Paid-up Stansberry Flex subscriber Art B.

![]() "I continue to be thrilled to have a life-time subscription to anything, especially to something as valuable as your products. With the exception of my pension (I spent 17 years to earn), I can't think of anything else financially related that I'll continually receive the rest of my life!" – Paid-up Stansberry Flex subscriber Jim K.

"I continue to be thrilled to have a life-time subscription to anything, especially to something as valuable as your products. With the exception of my pension (I spent 17 years to earn), I can't think of anything else financially related that I'll continually receive the rest of my life!" – Paid-up Stansberry Flex subscriber Jim K.

![]() "This has become more lengthy than I thought... my apologies for my long-windedness. Dear Porter and the entire Stansberry Research Staff... Before she died, President Andrew Jackson's mother wrote to him: 'To forget an obligation or be ungrateful for a kindness is a base crime – not merely a fault or a sin, but an actual crime. Men guilty of it sooner or later must suffer the penalty.' I, too, am guilty of a similar offense, the same of which I shall now reconcile, lest that penalty befall me. I have forgotten a kindness and simultaneously, a failure to offer proper and sufficient thanks.

"This has become more lengthy than I thought... my apologies for my long-windedness. Dear Porter and the entire Stansberry Research Staff... Before she died, President Andrew Jackson's mother wrote to him: 'To forget an obligation or be ungrateful for a kindness is a base crime – not merely a fault or a sin, but an actual crime. Men guilty of it sooner or later must suffer the penalty.' I, too, am guilty of a similar offense, the same of which I shall now reconcile, lest that penalty befall me. I have forgotten a kindness and simultaneously, a failure to offer proper and sufficient thanks.

"In that regard, Porter, I am writing to express my deepest gratitude for your generosity and your concern for the many, many people who you have never met, but to whom your influence is stolidly felt. Indeed, to tell those people, myself included, that which you would want told to you, were the roles reversed. I am a bit older nowadays and many of my younger years' income was consumed by meeting the basic needs of raising a family. I threw money into mutual funds and hoped for the best. The best did not materialize. I depended on the fund manager to do my work for me. As a Public School Teacher, I was too busy with work fighting the income-to-aggravation ratio.

"Fast-forward many years and much more lucrative employment: Only 4 years ago, there was no way I was getting into the market, considering the recent massacre. Through a colleague, who was speaking one day of graphene, I learned about Stansberry Research. He showed me some excerpts from a couple of newsletters from two guys named Porter Stansberry and Dan Ferris. Hmm... never heard of 'em. My interest was immediately piqued. Still... there had been a massacre!

"I am an information junkie and love to learn, but the information must come from a reputable and knowledgeable source. I signed up for all I could get of your 'free stuff,' and even from that, I could tell I was on to something. I signed up for the Stansberry Digest and DailyWealth Trader with my preciously scant money. Here was knowledge. Understandable concepts. Learning. Consuming every principle, technique, strategy, and nuance on how to wisely invest with information from an organization unclouded by the lure of managing money. 'You just offer information? You don't manage money? How can this be?' I said. Therein, to me, Sir, lies your credibility. You profit from sharing the inestimable value of your hard work and knowledge and you have succeeded and profited on your own merit. You're paid based on what you're worth.

"Eventually, I committed the money for a Stansberry Flex membership and it has changed my life. Working from the remnants of a portfolio, I was the Manager now. I set to work – and with your guidance and armed with the resources I now had available in the Stansberry Research Education Center, Jeff Clark's technical analysis methods, Doc Eifrig's options tutorials, and Steve Sjuggerud's 'cheap, hated, and in an uptrend' mandates – I posted a 28% gain the first year. (By the rule of 72, I can double my money in only 2.57 years? Give me more of that!)

"Now, I knew not only how to research, size my positions, REMOVE emotion, strengthen discipline, limit losses, buy and sell options, but also the 'power of doing nothing,' one of the most valuable strategies I now have. I did not mean to leave out [your other analysts], but you 3 guys were the sources of my learning and new unbridled enthusiasm. I never imagined loving to learn about investing as much as I do now. Market downturn? Bah! Bid the ruffians enter!

"I do not know where you get it, but your info is months ahead of the talking heads. All newsletters are full of the minutest detail, almost to a fault, but not quite. I love reading it all. Let the non-hackers read the Cliff's notes and garner the fractionally equivalent returns.

"There is nothing better than a quiet Saturday morning, a quiet tent (see later), a cup of coffee, and a newly published newsletter. I imagine that while I am reading, you are writing yet another article. I watch the talking heads and read reports or articles on Yahoo! Finance (purely for entertainment) and feel sorry for the guys who will only be there for the after-party. I have even anticipated some stop-out recommendations for lucrative pre-emptive strikes. I used to track my own stops, but now am a 'paid up' Lifetime Member of TradeStops, where something exciting is happening every day, and I can get a complete picture of everything I have, everything I want, and everything I need to be wary of, in a couple of clicks.

"How could I ever thank all of you enough? How could any of we subscribers thank all of you enough? You help us succeed. You help us learn. You help us thrive! To your staff: On the occasions that I have needed to contact Stansberry via email, or by phone, the customer service team (I deploy to the Middle East on a regular basis) has always been top notch and offers solutions, not excuses. As stated, I deploy a lot to the Middle East and East Africa and have always had a positive experience, feeling as if my issue was the only one on their plate, receiving full attention. Stansberry Research is certainly a first-rate outfit and you all reflect great credit upon yourselves. For all these things you have my profound gratitude. I think Andrew Jackson's mother would approve." – Paid-up Stansberry Flex subscriber Neal M.

Regards,

Porter Stansberry

Baltimore, Maryland

February 19, 2016

|