How it all ends...

How it all ends... Capitalism without the cost of capital... A clear warning from Buffett... An ETF that's about to collapse...

Perhaps more than just about any other research firm in the world, we've long warned that there will be serious consequences for the decisions we've been making lately.

But credit bubbles feel so good as they're being blown up that it's easy to forget what's really happening behind the curtains to create the faux prosperity we've been enjoying for the last few years. So this week, here's a gentle reminder about what's really behind the soaring stock market and our growing economy...

In the U.S., our central bank now owns a pile of bonds equal to 20% of U.S. gross domestic product (GDP). Japan's central bank's pile of debt is equal to 40% of its GDP. At its peak, Europe's central bank owned bonds worth nearly $4 trillion, or more than 25% of its GDP.

Consider the U.S. 10-year Treasury bond, for example. There is no more important financial benchmark in the world. It is hardly an exaggeration to claim that everything tradable in the world is priced off U.S. sovereign 10-year bonds. This is the globe's benchmark cost of risk-free capital. It is from this price that all other forms of capital are priced.

Currently, there is about $150 billion worth of 10- to 15-year bonds outstanding. Out of the total $150 billion in circulation, the U.S. central bank owns more than half. Likewise, at the "long" end of the curve, the Fed owns nearly half of all Treasury bonds dated 20 years and beyond.

In June, with benchmark high-yield rates in the U.S. at a staggering 4.77%, low-quality corporate borrowers added $30 billion in debt to their balance sheets – an all-time single-month record.

And it's also clear by looking at the colossal bubble that has formed in emerging-market debt. A brilliant New York hedge-fund manager pointed out that between 2009 and 2012, nearly $400 billion flowed into emerging-market credit markets – about four times more than average rates over the previous 10 years.

It doesn't, of course. We should see vast misallocations of capital and a tremendous surge in speculation. To see both of those trends in action, just consider the amount of casino construction around the world over the past five years. This is the way credit bubbles work. But it won't go on for long...

|

The United Kingdom, for example, owes foreign creditors $10 trillion... more than 400% of its GDP. Spain owes foreign creditors $2.3 trillion – 167% of its GDP. Italy owes foreign creditors $2.6 trillion – more than 100% of its GDP.

Central banks have proven adept at keeping these ridiculous credit structures in place. But there is a cost. And sooner or later, something will break... because capitalism doesn't work when there's no cost of capital.

Today, that's the U.S. dollar. For more than 40 years, the U.S. has recorded large (and growing) current account deficits with the rest of the world. This flooded the world with dollars, typically held in the form of U.S. Treasury bonds. These bonds are the heart of the world's banking systems, making up more than 60% of all reserves.

Now, thanks mostly to the surge in domestic oil production, the U.S. current account deficit has slid from more than 6% of GDP down to around 2%. At the same time, the Fed has been buying back tons of U.S. Treasury bonds. The unintended consequence of these combined actions is a huge decrease in global liquidity.

Turkey owes foreign investors $386 billion – roughly half of its GDP. About $160 billion of these debts come due over the next 12 months. And unlike the U.S. or Japan or Europe, Turkey can't simply print away these obligations.

So will the big central banks begin buying emerging-market bonds, too? Anything is possible... But I don't expect Turkey to do that. These defaults, which will definitely happen, will cause big problems in terms of political stability, currency values, and will inflict damage on banking systems across the world.

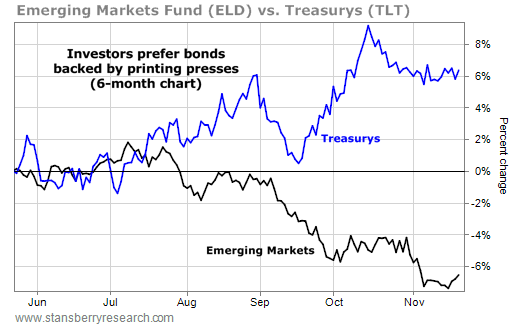

But during periods of stress – like late 2011 – TLT rallies while ELD declines. Since June, these two critical measures of the world's credit markets have sharply diverged. I believe that's a sign of things to come. I believe we're in the early stages of the "end game" where the giant paper charade of the last five years unravels...

And there is an abundance of signs of greed all around the market... from electric-car maker Tesla's share price to the nominal yield on junk bonds. Make sure you don't get swept up in the euphoria. Remember how fragile the world's banking system is... And make sure to buy a little physical gold this year.

I'm also happy to tell you that I was able to purchase razor No. 001 and razor No. 003. I'm hopeful that we will be able to offer our new shaving system to the public in a few weeks. If you're interested in keeping up with the latest developments at OneBlade, you can join our mailing list right here.

Editor in Chief Brian Hunt comment: Thanks for the question... and thanks for the chuckle...

A subscription to True Wealth is the single greatest deal in the investment newsletter business. For less than a nice dinner for two, you get the insight from one of the world's best investors... with one of the world's best long-term track records. You hear about a constant stream of investments that have huge upside... and little downside. You get "inside" Steve Sjuggerud's incredible network of contacts and experts.

True Wealth goes out to tens of thousands of readers. It's Steve's life's work. Do you really think Steve would "hold back" his best ideas, include "so-so" ideas, and end up looking like an ass in front of an audience this large? Steve is one of my best friends... and I can tell you with 100% certainty that he would not. He has a commitment to quality that you rarely see in this world.

True Wealth is read by some of the world's most successful professional investors, but it's written for individual investors. It boils down complicated ideas into their simple essentials. It features conservative recommendations. And for most people, that's all you need.

True Wealth Systems is Steve's more aggressive trading service. It typically recommends leveraged investments that exhibit more volatility than conventional stocks and bonds. It's not for everybody. It's more appropriate for people with plenty of investment experience who can handle higher-than-normal volatility.

But it's laughable to think that anyone who takes as much pride in his work – like Steve does – would "hold back" great recommendations from a massive audience. I'm still chuckling...

Regards,

Porter Stansberry

Baltimore, Maryland

November 21, 2014