How long will you sit idle?... The global monetary system is unraveling… European banks plummet… Japan's central bank can't create inflation, no matter how hard it tries… 'Quantitative easing only works when you're the only country doing it'… A bull market in gold the likes of which the world has never experienced…

![]() Today, we continue our thankless crusade to spur you to action...

Today, we continue our thankless crusade to spur you to action...

Longtime subscribers know our mission with the Stansberry Digest (and everything we publish) is to give you the information we'd want to know if our roles were reversed.

And dear reader, trust us when we tell you, you only need to know one thing today: The monetary collapse we've been warning about for years is here.

![]() But before we begin today's piece, here's a question for you...

But before we begin today's piece, here's a question for you...

How long will you sit idle while the global monetary system unravels before your eyes?

Unfortunately, despite our repeated warnings, we doubt most of you will take action until it's far, far too late. Like the frog slowly getting boiled alive, you'll think you're enjoying a warm bath, until you suddenly discover you're in boiling water.

And why would you worry? Stocks are rising today. Nothing, it seems, can hold equities back.

But the water is heating up. And the currency destruction we are seeing this year will roil global markets.

![]() Last month, the U.K. voted to leave the European Union. As we said at the time, it was "the first major domino to fall in the shell game of fiat currency."

Last month, the U.K. voted to leave the European Union. As we said at the time, it was "the first major domino to fall in the shell game of fiat currency."

The pound sterling immediately sold off from $1.50 to $1.36 – one of the largest drops for a major currency in history.

And while stocks may have recovered, the pound has not. It has continued falling to $1.29 Thursday, a new 31-year low. But we doubt the selloff is even close to finished.

Fiat money is a confidence game. And as we've repeatedly warned, when society loses faith in its money, pain follows.

Already, six fund managers have halted redemptions from their U.K. property funds. More than half of the funds committed by retail investors in the sector (around $17 billion) are now locked up.

Investors are panicking. And they're trying to dump U.K. assets.

The fear is that sellers will overwhelm the market, forcing fire sales of U.K. property... That causes a negative feedback loop.

![]() The same thing happened in the high-yield market last year. There's a huge liquidity mismatch today due to the widespread adoption of exchange-traded funds.

The same thing happened in the high-yield market last year. There's a huge liquidity mismatch today due to the widespread adoption of exchange-traded funds.

As we wrote in the September 29 Digest:

If you own any high-yield bonds through mutual funds or exchange-traded funds (ETFs), sell right now. Do not wait.

There's going to be a massive crisis because the liquidity profiles of ETFs and mutual funds don't match their underlying assets. It can take weeks or even months to sell a bond that's under distress. Meanwhile, these funds must provide daily liquidity to their investors. (Redemptions must be paid within seven days.)

Where's that money going to come from? The Wall Street Journal recently conducted a simple survey of several major bond funds run by institutional investors like BlackRock, Dodge & Cox, and Vanguard. It found plenty of examples of these funds holding bonds that would take nearly a year to sell – and even some bonds that nobody can sell right now.

![]() One U.K.-based fund, Aberdeen Asset Management, is taking a different approach. It's allowing investors to redeem their cash from the 3.4 billion-pound U.K.-property fund with just one catch: You take a 17% haircut.

One U.K.-based fund, Aberdeen Asset Management, is taking a different approach. It's allowing investors to redeem their cash from the 3.4 billion-pound U.K.-property fund with just one catch: You take a 17% haircut.

This is what happens when people lose faith in paper money... The value of your money, and all assets priced in that currency, can plummet – literally overnight.

And you no longer have to take our word for it. We just saw it happen in one of the world's leading economies.

![]() The Financial Times says analysts believe the conditions in the U.K. real estate market today are different from 2008 because banks are better capitalized and made better loans this time around.

The Financial Times says analysts believe the conditions in the U.K. real estate market today are different from 2008 because banks are better capitalized and made better loans this time around.

Digest readers know our feelings on the U.S. commercial property market. As Porter wrote in the April 29 Digest:

The U.S. consumer has been powering the global economy (thanks to a strong dollar and strong credit growth). Those trends are going to reverse, significantly, as our economy goes into recession. That will hurt the retail sector and, indirectly, commercial real estate, which always gets hammered during recessions and will get hammered doubly hard this time.

Think about the amount of empty mall space. It's great that Amazon's (AMZN) earnings are soaring, but what that also means is malls are dying. Sooner or later, all of this empty commercial space will begin to hurt commercial real estate in general. Those malls are going to end up as office complexes and apartments... something nobody has figured out yet.

And the U.K. is no better. According to investment bank JPMorgan, Royal Bank of Scotland (RBS) lent about 25 billion pounds to the commercial sector and Lloyds Banking Group lent 15 billion pounds.

Applying Aberdeen's 17% "haircut" to these banks' loan books means they've lost 4.25 billion pounds and 2.5 billion pounds, respectively, just in commercial real estate loans.

But the reality is much worse.

![]() Take a look at RBS' stock price. It has fallen nearly 45% since the "Brexit." And Lloyds (LLOY.L) has struggled, too...

Take a look at RBS' stock price. It has fallen nearly 45% since the "Brexit." And Lloyds (LLOY.L) has struggled, too...

.png)

![]() But the problem is much bigger than just the U.K. and its banks...

But the problem is much bigger than just the U.K. and its banks...

Since the start of the year, 20 of the world's biggest banks have lost one-quarter of their market value, nearly $500 billion.

Banks are the growth engine of an economy. They make loans to fund new businesses, construction, and consumer spending. And they collect the "spread" between what the short-term rates pay to borrow and the long-term rates they earn when they lend. But spreads are tightening... and banks are struggling to make money in a negative interest rate environment.

Said another way, banks help fuel asset bubbles. And the market is taking some air out of them today.

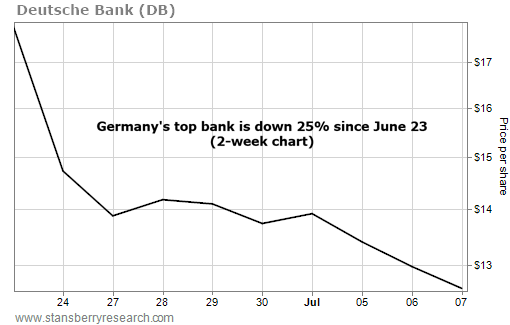

![]() It's the same across Europe. Just look at shares of Germany's premier bank, Deutsche Bank (DB):

It's the same across Europe. Just look at shares of Germany's premier bank, Deutsche Bank (DB):

![]() But it's worst in Italy. As we wrote in the July 5 Digest:

But it's worst in Italy. As we wrote in the July 5 Digest:

One of the worst is Italy's third-largest lender, Banca Monte dei Paschi di Siena. More than 30% of the bank's loans have already gone bad, and the European Central Bank has asked the bank to slash these nonperforming loans by 40% over the next three years.

The situation is so dire that the Italian government is looking to bail it out for the third time since the financial crisis. But there's a catch...

A new EU bailout rule, which took effect this year, officially requires a "bail in" – where the bank's bondholders and shareholders would shoulder losses first – before it can be bailed out with taxpayer funds. The Italian government wants to use an emergency "loophole" for the rule, but it isn't clear if the EU will grant an exception.

![]() Remember, we've been writing about Italy's collapsing banking system since March 2010. We told you about UniCredit and its roots back to Oesterreichische Kredit-Anstalt, the largest bank in Eastern Europe before World War I. The bank has received multiple bailouts (with another undoubtedly on the way) and announced losses amounting to tens of billions of dollars.

Remember, we've been writing about Italy's collapsing banking system since March 2010. We told you about UniCredit and its roots back to Oesterreichische Kredit-Anstalt, the largest bank in Eastern Europe before World War I. The bank has received multiple bailouts (with another undoubtedly on the way) and announced losses amounting to tens of billions of dollars.

For a good summary of UniCredit, click here... (Paid-up subscribers to Stansberry's Investment Advisory can also read the March 2010 issue.)

![]() That's the thing about monetary collapse...

That's the thing about monetary collapse...

It takes a long time to play out. When we first wrote about UniCredit in 2010, the problems with the bank were obvious. And we knew it would end in disaster. But central banks were determined to prop up the world's markets. And they did a good job. But central bankers are running out of ammo today.

The 10-year government bonds of Germany, Japan, France, Australia, the U.K., and the U.S. all hit record lows this week.

Treasurys are at 1.38%. Japanese 10-years are yielding negative 0.29%.

How much lower can these yields go?

Of course, that doesn't mean central banks won't try more quantitative easing. In fact, we expect it... There's no other choice.

![]() As we noted at the time of the Brexit, central banks around the world stood united to flood the world with more capital.

As we noted at the time of the Brexit, central banks around the world stood united to flood the world with more capital.

After that panicked, group press release, we've gotten more color in the situation.

Bank of England Governor Mark Carney said the Brexit will require "some monetary policy easing" from the central bank as the financial risks "have begun to crystalize." He said the BoE will do everything in its power to ensure banks continue lending.

![]() And the European Central Bank warned at their last meeting that the Brexit would have serious, negative repercussions for the countries in the European currency union. A Brexit vote could generate "significant, although difficult to anticipate, negative spillovers to the euro area via a number of channels, including trade and the financial markets," according to minutes from their Vienna meeting last month.

And the European Central Bank warned at their last meeting that the Brexit would have serious, negative repercussions for the countries in the European currency union. A Brexit vote could generate "significant, although difficult to anticipate, negative spillovers to the euro area via a number of channels, including trade and the financial markets," according to minutes from their Vienna meeting last month.

Even the Federal Reserve took a dovish tone in a meeting before the Brexit fallout... It voted unanimously to keep rates on hold (the first unanimous vote since January) due to weak economic growth.

After the meeting, James Bullard, the St. Louis Fed president, said he expects the U.S. central bank will keep rates near their current level through 2018.

![]() The private sector is also catching on.

The private sector is also catching on.

Credit-ratings agency Fitch Ratings has downgraded a record 14 sovereign nations so far this year, including the U.K.

"The short-term economic impact of the Brexit referendum will be decidedly negative in the U.K.," said James McCormack, Fitch's global head of sovereign ratings... And he believes the economic impact will be far-reaching.

![]() Meanwhile, the pound is plunging... The euro and yuan will follow.

Meanwhile, the pound is plunging... The euro and yuan will follow.

Rules of capitalism no longer apply today. And Japan will be forced to further ease to compete with weakening currencies around the world. The situation in Japan is especially bleak...

Despite its best efforts (including printing nearly 300 trillion yen – or $3 trillion – since 2012), the Bank of Japan (BoJ) can't create inflation. And its currency is actually getting stronger.

.png)

![]() The BoJ already owns the majority of Japanese government bonds (JGBs), and it's a top-10 shareholder in 90% of Japanese blue-chip stocks. So what's next? We wouldn't be surprised to the see the BoJ start buying Treasurys and U.S. stocks. Treasurys, despite record-low yields, are still much more attractive than negative-yielding JGBs.

The BoJ already owns the majority of Japanese government bonds (JGBs), and it's a top-10 shareholder in 90% of Japanese blue-chip stocks. So what's next? We wouldn't be surprised to the see the BoJ start buying Treasurys and U.S. stocks. Treasurys, despite record-low yields, are still much more attractive than negative-yielding JGBs.

![]() If you've managed to read this far, you should understand what's coming next for the global economy.

If you've managed to read this far, you should understand what's coming next for the global economy.

But before we wrap up, here are two more points.

First, consider this from billionaire hedge-fund manager Kyle Bass, who made his fortune during the subprime crisis...

In an interview with Real Vision TV, he recounted a private, closed-door meeting with "one of the world's top central bankers," who told him: "You know Kyle, quantitative easing only works when you're the only country doing it."

![]() That's where we are today. It's a global race to the bottom. And one of the world's worst monetary offenders, Japan, can't weaken its currency despite its best efforts. But it will continue to try.

That's where we are today. It's a global race to the bottom. And one of the world's worst monetary offenders, Japan, can't weaken its currency despite its best efforts. But it will continue to try.

And Japan will soon have one of the world's great money printers to help in its battle to inflate.

According to Reuters, former Fed Chairman Ben Bernanke will meet with Japan's Prime Minister, Shinzo Abe, in Tokyo next week.

From Reuters:

Bernanke, who led the Fed through the global financial crisis in 2008, will be in Japan next week. It has been arranged for him to meet officials including Abe and Bank of Japan Governor Haruhiko Kuroda, according to a government official speaking on condition of anonymity.

Bernanke is expected to discuss Brexit and the BOJ's negative interest rate policy with Abe and Kuroda, the official said.

![]() "Helicopter Ben" is on his way to Tokyo to share the secrets of the printing press. We should soon see money falling from the sky.

"Helicopter Ben" is on his way to Tokyo to share the secrets of the printing press. We should soon see money falling from the sky.

We don't know exactly how this will play out. We're truly in uncharted waters. We can be sure the world is losing faith in paper money and its guardians, the central bankers.

And we believe we're embarking upon a bull market in gold the likes of which the world has never experienced. Early investors into this trend will make a fortune... possibly the biggest profits in their investment careers.

This is why we launched Stansberry Gold Investor a few months ago... and why Porter put his name on a gold-research product for the first time in his career. As longtime readers know, when Porter decides to do something, he makes sure it's great... And he wanted his subscribers to have access to the best gold and precious-metals research available anywhere.

Already, our results have been outstanding. The weighted model portfolio has returned 47% since April.

And this is just the beginning. We'll see some of these positions rally hundreds, likely thousands, of percent.

![]() We'll leave you where we began... The monetary collapse is here. And gold will skyrocket as a result.

We'll leave you where we began... The monetary collapse is here. And gold will skyrocket as a result.

If you don't have a solid portfolio of gold and gold stocks today, you're making the biggest mistake of your life. And Stansberry Gold Investor is the absolute best way to allocate money to gold.

You can learn more here...

![]() New 52-week highs (as of 7/7/16): Automatic Data Processing (ADP), Becton Dickinson (BDX), Ciner Resources (CINR), Cross Timbers Royalty Trust (CRT), Western Asset Emerging Markets Debt Fund (ESD), Fidelity Select Medical Equipment and Systems Fund (FSMEX), Nuveen Preferred Securities Income Fund (JPS), Medtronic (MDT), Nuveen AMT-Free Municipal Income Fund (NEA), Nuveen Premium Income Municipal Fund 2 (NPM), Nuveen Municipal Value Fund (NUV), ETFS Physical Platinum Shares Fund (PPLT), Constellation Brands (STZ), Wells Fargo – Series W (WFC-PW), and PIMCO 25+ Year Zero Coupon U.S. Treasury Index Fund (ZROZ).

New 52-week highs (as of 7/7/16): Automatic Data Processing (ADP), Becton Dickinson (BDX), Ciner Resources (CINR), Cross Timbers Royalty Trust (CRT), Western Asset Emerging Markets Debt Fund (ESD), Fidelity Select Medical Equipment and Systems Fund (FSMEX), Nuveen Preferred Securities Income Fund (JPS), Medtronic (MDT), Nuveen AMT-Free Municipal Income Fund (NEA), Nuveen Premium Income Municipal Fund 2 (NPM), Nuveen Municipal Value Fund (NUV), ETFS Physical Platinum Shares Fund (PPLT), Constellation Brands (STZ), Wells Fargo – Series W (WFC-PW), and PIMCO 25+ Year Zero Coupon U.S. Treasury Index Fund (ZROZ).

![]() Have you taken part in the early days of gold's bull market? Tell us your story at feedback@stansberryresearch.com.

Have you taken part in the early days of gold's bull market? Tell us your story at feedback@stansberryresearch.com.

![]() "I'm doing well with gold and gold related investments, thanks for that... So one of the reasons gold is rising is due to currencies around the world being devalued. One of those currencies is the one I'm making my gold investments in. I guess if you're making it faster than the devalue, it's good. But this will have to be addressed at some point down the road, I would imagine. And once again, can't say it enough, thanks a lot for everything you do. This service is, in one word, awesome." – Paid-up subscriber Rob W.

"I'm doing well with gold and gold related investments, thanks for that... So one of the reasons gold is rising is due to currencies around the world being devalued. One of those currencies is the one I'm making my gold investments in. I guess if you're making it faster than the devalue, it's good. But this will have to be addressed at some point down the road, I would imagine. And once again, can't say it enough, thanks a lot for everything you do. This service is, in one word, awesome." – Paid-up subscriber Rob W.

Goldsmith comment: That's why we're recommending that folks own gold... because paper currencies around the world are being devalued. And you can swap those currencies for gold. Plus, more than a third of developed-nation sovereign debt around the world sports a negative yield today. And that makes gold's zero yield much more attractive.

The dollar is outperforming other currencies right now. It's the best house in a bad neighborhood. But soon enough, economics will catch up.

Be happy to hold gold today. It has stood the test of time as a currency. And it will only get stronger as central banks around the world destroy their currencies.

Regards,

Sean Goldsmith

Baltimore, Maryland

July 8, 2016

|