Masters Series: The 'Lions' Are Feasting

Editor's note: Are you ready for a market crash?

Have you followed our warnings and taken steps to protect your portfolio?

If not, you should... and soon. In today's Masters Series essay – adapted from the January 29 Digest – Porter details the "domino effect" that will soon devastate the U.S. economy and wipe out unprepared investors...

The 'Lions' Are Feasting

In today's Digest, I'm going to try something we haven't done yet... something I doubt you've seen anywhere, ever before. I'm going to show you the entire "domino effect" of declining profit margins, deteriorating credit, mounting losses, and financial panic that's spreading right now across the U.S. economy.

To do this will require multiple stock charts, so I apologize in advance if you're reading this message on a device that doesn't allow you to see charts easily. (I'll describe the moves in writing so that you can still follow along.)

If you're in a hurry and you don't have time to read this entire message, I'll give you the conclusion in advance: The commodity-led global boom that was created by central bankers... nurtured by China's huge investments in fixed assets... and propelled by student loans and car loans in the U.S... is coming to a crashing halt.

The idea that still more accommodation from central banks will halt the declines in commodity prices and credit quality seems dubious. There was an epic boom. There will now be an epic bust. And you can watch it unfold, if you know where to look.

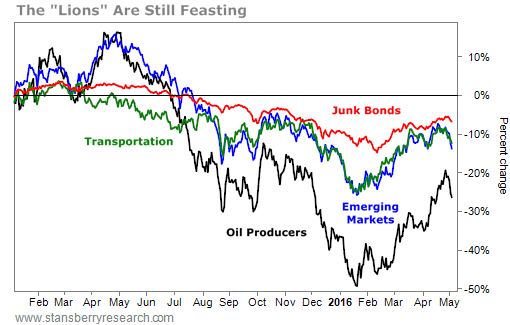

Let's start with the "lions" we've been writing about for months and months...

That's U.S. onshore oil and gas firms, emerging-market stocks sensitive to commodity prices, economically sensitive U.S. transportation stocks, and credit-quality-sensitive corporate bonds.

The onshore oil and gas firms are represented by the VanEck Vectors Unconventional Oil & Gas Fund (FRAK). The emerging-market stocks are represented by the iShares MSCI Emerging Markets Fund (EEM).

The economically sensitive U.S. transportation stocks are represented by the Dow Jones Transportation Average (^DJT). And the credit-quality-sensitive corporate bonds are represented by the iShares iBoxx High Yield Corporate Bond Fund (HYG).

Here's how the lions have performed since 2015:

As you can see, oil and gas firms are still down 25%, despite a big rally since February. The others have rallied also. Was January the bottom? I doubt it.

The current rally is backed by a belief that Russian President Vladimir Putin and the Saudis will cooperate to cut production. Just think about that for a minute. Folks buying oil today are putting their faith in Putin and the House of Saud? Good luck with that.

Meanwhile, there are still more than 400 active drilling rigs in U.S. onshore oil fields. That's right, friends... Despite oil priced at just more than $40 per barrel, there is still drilling in many Texas fields, where production costs can be as low as $12 per barrel. (Take that, you Peak Oil imbeciles.)

Here's another "fun" fact... despite a 55% reduction in drilling rigs over the last year... U.S. oil production is only 8% lower than it was a year ago (May 2015). It's still higher than it was in August 2014 when oil prices were $100 a barrel.

In other words, the productivity of U.S. onshore oil and gas firms continues to soar. Looking over the long term, total U.S. oil supply bottomed out in February 2001 at 824 million barrels. That was the nadir of a decade-long decline in supply. Despite all of the Peak Oil nonsense, the U.S. supply of crude oil has actually been increasing since then. According to the most recent data, total supplies have grown by roughly 15% since January 2015, from 1 billion barrels to 1.24 billion barrels. It's hard to imagine that oil prices will increase in any meaningful way as long as both U.S. production and supply continue to grow.

Lower energy prices are great news for our currency, economy, and country in the long term. But in the short term, the amazing and radical restructuring of the world's most important commodity (energy) continues to wreak havoc across the world's markets. These changes will be especially hard on countries ill-equipped to handle the most powerful force in economics – creative destruction.

Think about what kinds of governments and cultures aren't so good at managing fast-moving change. How about authoritarian states like Russia? How about theocratic dictatorships like Saudi Arabia? These are the places oil traders think will help limit growth in supply. Yeah, right. So let's take a closer look at what much lower oil prices mean for the world today.

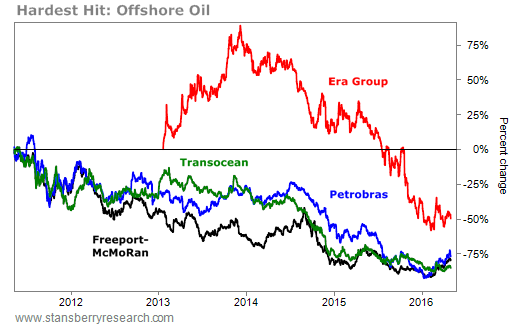

The first and most obvious impact of new, cheaper supplies of oil is that other, higher-cost forms of oil have suffered. Not widely discussed has been the complete destruction of the entire offshore U.S. oil industry. Resource giant Freeport-McMoRan (FCX) – which had invested tens of billions of dollars in offshore assets and drilling – announced recently that it's halting all of its Gulf of Mexico exploration. Its stock is now down 77% over the last five years. Likewise, Brazil's state-owned Petrobras (PBR), whose primary oil assets are in the deep (sub-salt) waters of Brazil, has fallen 79%.

Meanwhile, a huge industry supports offshore drilling. Transocean (RIG), which spent a decade buying up more than half the world's supply of offshore drilling equipment, has seen its stock fall 85%.

And it's not just the oil companies and the drilling firms. An entire industry is built around supplying these offshore cities... maintaining them... powering them... insuring them. Era Group (ERA) operates a huge fleet of helicopters that ferry men and supplies to rigs in the Gulf of Mexico. Rigs that are being turned off, one by one. Its shares are down 50% since the company went public and down 68% over the last two years.

The destruction is most obvious in the offshore oil fields. But these declines also presage huge, future opportunities for strong hands – people with permanent capital. The same technologies that have lowered production costs in onshore fields will eventually be put to work in offshore fields.

At some point in the next decade, these rigs will start up again. But a lot of debt has to be written off first. Investors who can buy these assets for pennies on the dollar and hold them on debt-free balance sheets will reap windfalls. Remember, the cure for low prices is low prices. Cheap energy will create lots of new demand for that energy.

In the meantime, the restructuring of the global energy complex has battered firms that are involved in the transportation of energy. Over the last two years, the boom that once propelled these firms has suddenly reversed course.

Tenaris (TS), whose steel pipes are designed to facilitate oil recovery from offshore rigs, has declined 44%. Union Pacific (UNP), whose rail cars were recently packed with oil coming from shale fields and whose shares soared on that demand, is now down 9%. And a personal favorite, Cheniere Energy (LNG) – whose balance sheet is stuffed with debt and whose facilities are designed to transport expensive, liquefied natural gas – has dropped 38%. These firms represent the first domino along a much longer chain. And that's why the Dow Jones Transportation Average has been such a valuable leading indicator of this bear market.

![]()

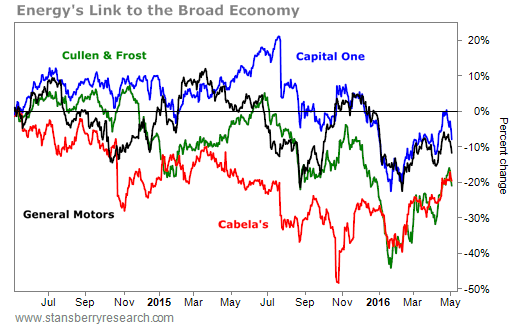

The next leg of the chain is the thousands of firms around the country that sell into the broader supply chain of the oil and gas industry and serve all of its employees. I'm talking about the banks that finance oil and gas development, like Cullen/Frost Bankers (CFR), whose shares are down 22% over the last two years.

And I'm talking about the retailers who sell to the men of these industries – the roughnecks who love to hunt. Cabela's (CAB), one of the country's leading outdoor outfitters, has seen its stock plummet 20%. Trust me, that's not because these guys are suddenly buying their guns and ammo from Amazon. Cabela's profits are derived almost completely from its store credit card, where losses are now mounting.

Likewise, a lot of the employees of the greater energy/transportation complex have a credit card or a car loan with Capital One Financial (COF). Losses are mounting there, too, and its shares are down 9% over the last two years. Finally... what do all of these oil workers drive? A truck, of course. And who makes most of the trucks in the U.S.? General Motors (GM), whose shares are down 13% over the last two years.

The next big "bust" in our economy is going to come from the financial side. Somewhere out there, right now, there's a firm that's been speculating on energy prices. No one suspects it's in trouble today because it has been hiding the losses... doubling down... praying for a bounce in energy so that it can escape. I don't know which firm it is... but I know it's out there somewhere.

The losses might come in the form of a huge write-off. For example, I don't think anyone has yet figured out how massive the energy-related losses at Berkshire Hathaway are going to be. Warren Buffett has huge exposure to energy, both directly through Suncor Energy (SU) – down 32% over the past two years – and Chicago Bridge & Iron (CBI) – down 53% over the past two years.

He also took big losses on ConocoPhillips (COP) – down 43% over the past two years – before moving into that company's spinoff, Phillips 66 (PSX). Buffett has said he lost more money on ConocoPhillips than any other stock in his career.

Buffett also has lots of indirect exposure through IBM (which has all of the big energy companies as clients), GM (whose trucks the roughnecks buy), and American Express (which provides financial services to millions of oil industry executives and small business owners). These positions are down 25%, 13%, and 26%, respectively, over the past two years. Imagine if these losses lead to another downgrade of the company's credit rating...

The point is, these problems are going to be transmitted through financial firms, through cross holdings, and through credit ratings and losses. This isn't a mere correction to stock prices. Stock prices weren't that inflated.

This is creative destruction on a massive scale. And it's hitting a world economy that's more brittle than ever, thanks to huge concentrations of wealth and the accumulation of more debt than the world has ever seen. It's not going to be pretty. And it's not going to be over in a few months. This will last a few years... or maybe even most of the next decade.

What should you do? I'm spelling it all out, step by step, in a seven-part educational series. To learn how to sign up, click here.

Regards,

Porter Stansberry

Editor's note: As we explained yesterday, if you want to protect yourself and even prosper from the crisis that's about to unfold, the Bear Market Survival Program is the only thing you need. And right now, we're offering this seven-part educational series at an almost 15% discount off its regular price. Get started here.