More of the same in 2015... The slowdown in China and Europe continues... Draghi teases QE again... Euro hits its lowest level since 2010... The dollar's huge year... Emerging market troubles... Jeff Clark is long gold stocks...

We're starting 2015 with slowing global growth and the promise of more quantitative easing... a story we're all familiar with by now.

We're starting 2015 with slowing global growth and the promise of more quantitative easing... a story we're all familiar with by now.

China's Purchasing Managers Index (PMI ) – a measure of manufacturing health – fell from 50.3 in November to 50.1 in December. (A reading of less than 50 means the economy is contracting.) The PMI in the European currency union fell from 50.8 in November to 50.6 in December.

In Europe, Italy's

In another surprise move, Spain's PMI fell from 54.7 in November to 53.8 in December. Economists had expected it to rise to 54.9. Still, Spain's reading is the best of the "big four" European currency union economies (Spain, France, Italy, and Germany).

This is nothing new for European Central Bank (ECB) President Mario Draghi, who has been teasing the world with more stimulus in Europe for the past year. And he began this year with more of the same...

In an interview with German financial newspaper Handelsblatt, Draghi once again said he stands ready to act... without actually doing anything.

|

Again, Draghi said that buying European currency union government bonds was on the table (quantitative easing). Inflation currently sits at 0.03%... well shy of the ECB's 2% goal.

As we've noted in the past, Germany (the continent's economic engine) is against quantitative easing. It would punish the fiscally conservative Germans to bail out the lax PIGS nations (Portugal, Italy, Greece, and Spain).

And today, Michael Fuchs, a senior member of German Chancellor Angela Merkel's party, reminded Draghi of his nation's wishes, telling Deutschlandfunk radio...

|

But the market is siding with Draghi. The euro hit 1.2026 versus the dollar, its weakest level since June 2010. That's following its worst annual loss since 2005.

And bond yields across the European currency union are falling on hopes that Draghi will intervene...

Ten-year yields on Italian bonds have fallen to 1.8%. Spanish bond yields hit 1.5%. And Portugal's 10-year yield dropped 2.5%.

As we noted in yesterday's Digest, these low yields relative to Treasurys is another reason for strength in Treasurys this year.

The dollar's strength continues into the new year. The greenback strengthened against all major currencies in 2014 for the first time since 2000. The euro and yen both weakened 12% against the dollar. Norway's krone was the worst performer against the dollar, weakening 19%.

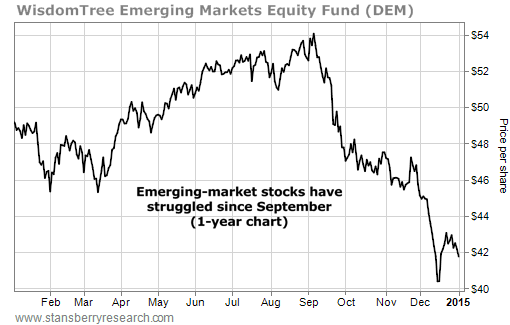

As we've explained before, a stronger dollar is one reason for the rout in commodities we're experiencing. But it's also a reason for the selloff in emerging-market stocks...

Emerging markets hold more than $6 trillion of dollar-denominated debt. In 2014, emerging-market companies issued a record $276 billion of dollar-denominated bonds.

Emerging markets hold more than $6 trillion of dollar-denominated debt. In 2014, emerging-market companies issued a record $276 billion of dollar-denominated bonds.

And as the dollar strengthens, bond payments on that debt cost more. It also costs more to pay the money back when the bond matures.

The dollar's strength is hurting corporate margins... And we'll likely see weaker players get squeezed out.

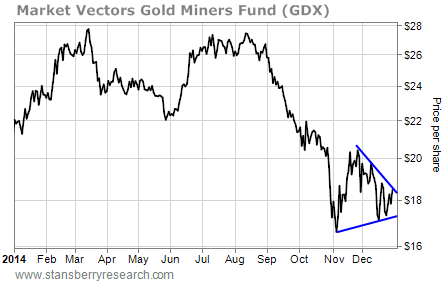

And while the stronger dollar has weighed on gold prices – sending gold down 1.5% in 2014 – Stansberry Short Report editor Jeff Clark thinks we're due for a bounce in gold stocks. As he wrote in today's Growth Stock Wire...

|

Regards,

Sean Goldsmith

January 2, 2015