The latest Einhorn short recommendation... A pain-free lesson in accounting... A far better way to invest in oil than buying oil stocks...

In today's Friday

Digest... a review of the biggest controversy on Wall Street this week, the brouhaha that followed David Einhorn's critique of Pioneer Natural Resources – a major shale-drilling firm with assets in the Permian Basin. I (Porter) picked this topic because it has been in the headlines. I thought you might be curious to learn what it's really all about.

And I have one more reason to tell you about this situation... it's a great opportunity to show you why the accounting Wall Street uses to value stocks is so misleading most of the time. Don't worry, though. I made a commitment to myself when I sat down to write this week's

Digest. I won't use any jargon. None. What follows below is all in plain English.

But remember, while a writer can make the reading easier, he can't make the learning easier. As we remind readers frequently: There's no such thing as teaching. There's only learning. So take a deep breath and get comfortable. I'll share a big secret below that will make you a much better investor.

If you were out of town this week, the annual Ira Sohn Investment Conference took place Monday. This Manhattan charity event has become the most renowned forum for rich and famous investors to show off their best research. Hedge-fund managers like to share their best ideas (after they've built their own investment positions). It's a form of marketing ("Look how smart I am"). And it's also a kind of competition. These hedge-fund guys have big egos. They are super-competitive. Each guy wants to be cleverer than the next guy. But they all come in second. Einhorn is

always the cleverest speaker, filling his presentations with wicked humor. The audience loves him.

David Einhorn manages a big ($10 billion) hedge fund called Greenlight Capital. It's called a "hedge" fund because he both buys stocks and sells them short. He's one of the few managers who doesn't use leverage. He doesn't borrow additional amounts of capital on top of the money people have given him to manage.

He launched his fund using his savings plus money he borrowed from his parents – about $900,000 – in 1996. Since then, he has done incredibly well – both for his investors (his average annual gain is 25%) and himself.

What Einhorn said about Pioneer Natural Resources wasn't flattering. He called the firm a "motherfracker" – which got a big laugh from the audience. He explained why his firm has been shorting the stock. According to Einhorn, the problem is simple:

Pioneer has spent more to develop its asset base and produce its oil than it's worth.

The math is simple.

Pioneer is getting $36 per barrel of energy they produce. That's a lot less than most investors realize. Even though the spot price of oil is around $60, Pioneer's production isn't all oil. There's 50% oil, 29% natural gas, and 21% natural gas liquids in each barrel of energy Pioneer produces. The natural gas components are worth a lot less than the oil in the U.S. market.

Meanwhile, Pioneer spends $20 per barrel for production expenses. That leaves a pretty slim gross profit margin ($16 per barrel).

These are the numbers Wall Street focuses on – the operating results. These are the "cash results" that a company can use to pay back borrowed money. But this kind of analysis has a flaw. It doesn't include all of the actual costs. The additional costs beyond the operating costs are known as capital expenditures. This is the money Pioneer needed to buy the land, heavy equipment, and buildings. And it's the money the company spent to drill and frack the wells.

Wall Street doesn't include all of these charges against Pioneer's annual results because these expenses are generally financed over several years. But they are real expenses.

Einhorn did some digging to put both sets of costs – operating and capital costs – together. First, Einhorn figured out the total amount of money Pioneer has spent so far on capital investments in the Permian Basin. Then, he divided that number by the total amount of oil and gas barrels of energy the company produced there. When you add the operating costs per barrel ($20) to the capital costs per barrel ($28) you end up with a figure ($48) that's substantially larger than the revenue per barrel ($36). Thus, Einhorn argues that the company is actually producing a negative return of $12 per barrel. Obviously, if this continues, the company will go bankrupt.

Einhorn uses these figures and this logic to warn investors that the fracking boom isn't sustainable and that oil-fracking stocks are woefully overvalued. He also showed the conference attendees that even if oil were trading at a higher price ($68), and even if Pioneer could reduce some of its costs going forward (by 20%), it would still end up losing money on each barrel of oil produced. If Einhorn is right, the U.S. onshore oil producers are in big trouble and their investors are going to get wiped out. But... don't panic yet.

It's not easy to debunk Einhorn. He's an incredibly smart guy. I've met him. We've exchanged e-mails about business valuation and accounting. I'd estimate his IQ is north of 130. And he has a team of smart analysts working for him – all the brains money can buy. For the last 20 years, his hedge fund has been one of the best all-around performers. He has made lots of famously good (and tough) investment decisions – like shorting Lehman Brothers when it was still one of the most powerful investment banks in the world.

But nobody knows everything. I think Einhorn is making one significant mistake in his analysis. It's a big one.

At the beginning of the presentation, Einhorn told the audience that he'd found another stock that was analogous to his famous short sell of St. Joe's – a big land holding company in northwest Florida. St. Joe's was spending more in capital investments to develop each lot than it could earn selling them.

Oil wells, however, are a lot different than residential development lots. The biggest difference? You can only sell a lot once. With an oil well, production doesn't stop for a long time. You can keep selling the oil year after year after year.

Einhorn's analysis takes the company's cash accounting over a 10-year period and then subtracts 100% of the capital investments that have been made over the period. On this basis, it looks like the company has spent a huge amount of money to produce 30 million barrels of additional proven reserves and 472 million barrels of oil.

But Einhorn's analysis ignores the fact that these wells continue to produce oil and will continue to produce for a long time. That's not a logical assumption. We know for certain that these wells will continue to produce oil for a long time – likely decades. These additional cash flows will require little additional capital spending. Thus, through time, as the amount of oil produced from these investments grows, the per-barrel capital cost of each barrel will decline.

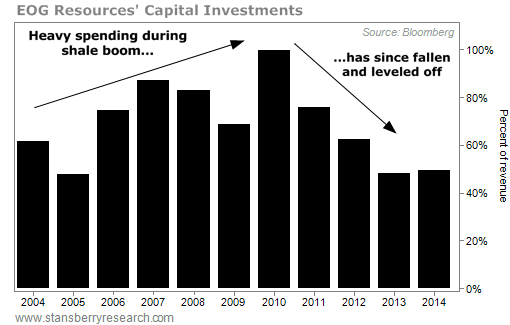

Here's a chart that shows you what I'm talking about. EOG Resources is an independent energy producer, like Pioneer. This chart shows you how much, as a percentage of revenue, EOG is spending on capital investments. At the beginning of the shale boom (2010), EOG had to spend heavily to buy land in the best shale fields. It spent heavily on drilling equipment and fracking. But... as its development pace leveled out... and as its revenues from oil wells continued to grow, the amount of capital spending as a percentage of revenues began to fall sharply. This trend will continue, across the industry.

We are generally critical of accounting rules and conventions. Instead of focusing on the numbers produced by Generally Accepted Accounting Principles (GAAP accounting)... I tell my analysts to look at the actual cash accounting and the capital expenditures and come up with our estimate of the real "owner's earnings." What we find, most of the time, is that GAAP accounting severely

underestimates the real profitability of high-quality businesses because growth in brand value (goodwill) is completely ignored. And in capital-efficient companies, depreciation charges are generally exaggerated.

That's one of the major reasons we prefer to own highly capital-efficient companies. Wall Street tends to undervalue their true earnings potential.

Resource companies, however, are not capital-efficient. The more gold, oil, coal, or copper that they pull out of the ground, the more capital they must spend to rebuild their reserve base. As a result, for these kinds of companies, it is very important to understand the GAAP accounting figures. The accounting in these firms is critical to understanding if they're earning more on their operations than they're "spending" in terms of the depletion of their balance sheet.

But strangely, Einhorn didn't use the GAAP accounting figures. He used their cash accounting figures to do his analysis. I think that's a mistake – and could be misleading if you don't know the difference. Let me show you why.

The logic of the accounting rules are easy to understand. Just think about how the railroads were built. Nearly all of modern financial accounting goes back to the needs of the railroads and their massive expansion across the country 150 years ago. If you were going to build a railroad and you needed a lot of expensive tunnels and big bridges – stuff that's going to last for years and years – how would you account for those expenses? One idea was to estimate how many years they'd last and then "pay for them" in your accounting by charging for them a little bit each year. And that's what happens now using GAAP accounting.

Shale-oil drillers make major investments and then, each year, their earnings are charged for depletion (as their oil reserves are used up) and depreciation (as the value of the land, frack job, and the other capital assets are used up). The critical thing for investors to monitor is how much money are these companies earning after all of these noncash charges? That's the real measure of their profitability.

Pioneer's net profit margin (which includes depletion and depreciation charges) has averaged 15% each year over the last decade. EOG's profit margin has averaged 17% over the last decade. Contrary to Einhorn's presentation, these firms have been consistently and substantially profitable.

Now, let's say that you're not comfortable with all of the GAAP accounting assumptions. You'd rather see whether or not these firms are actually making money on a cash basis. Fine.

The proper way to measure this isn't to assume that these oil wells will never produce another drop of oil, but instead to take the cash accounting and then subtract that year's depletion and depreciation expense. Doing this analysis shows both Pioneer and EOG earning profits of around 30% of revenues. These are healthy businesses. That's why their GAAP accounting shows annual returns on equity in the double-digits – 10% for Pioneer and 15% for EOG.

If you think oil prices are going to be much lower than $60 a barrel for a long time into the future, then it's likely that producers that generate their production primarily from fracking will see their share prices fall. At that price, many of them won't be able to earn a good return (or any return) on the investments they've made in land.

But if that's the case, the companies producing energy from oil sands ("oil mud" producers, as we call them) are in even bigger trouble. We took the operating figures for the major publicly traded oil-sands firms and put them together to compare with EOG and Pioneer. The oil-sands producers have much less revenue growth... much lower gross margins... much lower operating margins... much more leverage (debt)... and much higher operating costs.

If oil remains at less than $60 a barrel, I think the entire oil-sands industry will go bankrupt. The shale producers, meanwhile, will simply stop fracking new wells and only produce their lowest cost wells. They have a lot more financial flexibility.

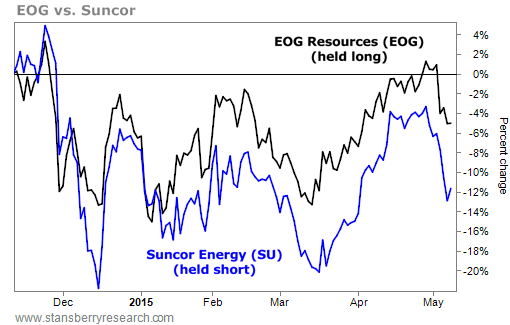

That's why, rather than simply buying EOG during the big dip in oil prices, we instead recommended buying EOG and selling short shares of the biggest oil-sands company, Suncor. This allows us to profit as the advantages of the shale-drilling model are proven during a period of volatile oil prices. As long as oil trades for less than $100 a barrel, I'm confident that the high-quality shale producers (EOG is the best) will outperform the oil-sands operators by a wide margin. And that's what's happening so far. Here's what that trade looks like over the past six months:

Now... let's assume you don't want to become an expert on oil-field accounting or the critical differences between oil-sands and oil-shale production. No problem. Here's a wonderful secret for you to learn...

You don't have to buy resource companies to do well as an investor. You can easily earn a substantial return on your investment portfolio without ever owning a commodity-based business – and I'd recommend doing so if you don't want to become a resource expert. Making money in commodities is hard because their prices are volatile and it's impossible to build a brand. These companies require huge amount of capital.

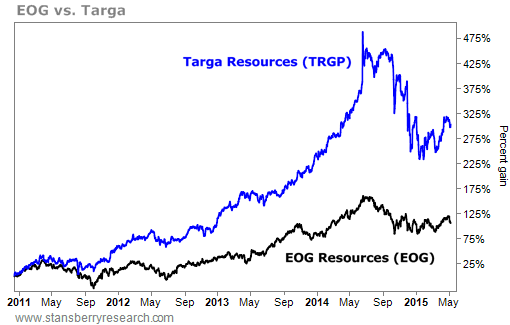

So if you want protection from hyperinflation, but you don't want to be a resource investor... what should you do? Focus on the royalty companies that will pay you more as oil production goes up. Their claims on the assets can't be lost in bankruptcy. Focus on the pipeline companies that will get paid regardless of the commodity price or oil producer. And focus on the service providers – some of which are well-run, capital-efficient businesses. You'll find that we recommend companies like these far more often in our newsletters than the actual producers. They're far better investments.

Here's a chart showing the relative performance of one of our recommended energy transportation companies (Targa Resources) versus the shares of EOG during the shale boom over the last five years:

I hope that helps you understand the big controversy on Wall Street this week. Have a wonderful Mother's Day weekend.

New 52-week highs (as of 5/7/2015): Activision Blizzard (ATVI), AXIS Capital (AXS), and CDK Global (CDK).

"I enjoyed your discussion on the decline of capitalism. I've also seen the flat wages chart but interpret it differently. Since the '80s, inflation has been basically negligible, and can hardly be the cause of stagnating wages. Globalism and 'Trickle-down' economics also originated about then and seem far more likely the culprits. As the rich and powerful get more control of the wealth, consumption, jobs and relative wages decrease and bubbles abound. Perhaps Freddie Gray would not have died a heroin dealer if there were good jobs for blacks in America.

"I'm no Marxist, having enjoyed the benefits of this capitalist society and made good money in the process, but this seems very much like the crisis described in Das Kapital. Perhaps there is something to learn there. And with respect to Ron Paul and his obvious dislike for the interventionist Roosevelt legacy, I find it curious that no one acknowledges that those were the most prosperous years since the Great Depression." – Paid-up subscriber David D.

Porter comment: How much do you know about math?

The purchasing power of the dollar fell by 50% during Greenspan's term. Study the power of compounding, where even small, almost negligible inflation will have a woeful impact upon a currency over 20 years (1987-2006).

Your knowledge of history is also... there's not a nice word for it.

Globalism first emerged in the 1880s with the advent of the steamship. Back then, currencies and trade were settled in gold. The result was a stunning rise in wealth and the standard of living for all wage-earners around the world. The 1880s were the single greatest years for annual growth in real, per-capita income in U.S. history. This was a dramatic period of wealth creation because for the first time ever, there was a global talent pool, enabling radical specialization of labor and trade.

Trade is one of the only win-win deals in human action because of comparative advantage. Look it up. Or try growing bananas in Iceland. Even Paul Krugman admits there is no logical argument against free trade.

Trickle-down economics is just another phrase for class warfare. It has no actual meaning. What it's really is a euphemism for the nonsense idea that my wealth was taken from others who deserved it more than me. Those who deserve wealth are happy to earn it, through labor, innovation, investment, and trade – because those means also benefit others. Those who do not deserve wealth take it through coercion, which is where all "trickle down" arguments lead.

Freddie Gray was qualified for dozens of jobs. But he didn't have a job and, as far as we know, never held one in 25 years of life. For many people in his neighborhood, working an honest day is for "chumps." I'd invite you to come spend a day with me while I attempt to hire anyone at the corner of North Avenue where the riots occurred. With all due respect, you must acknowledge that you know precious little about math, history, economics, or the culture of the inner city. But I'd bet you vote.

Regards,

Porter Stansberry

Baltimore, Maryland

May 8, 2015