The most important downgrade in the world…

The most important downgrade in the world... Hug a banker... Buffett's debacle... Students aren't paying... Credit distress continues to build... Next week's big 'reveal'... The only Christmas gift you'll want...

![]() We start today's Friday Digest with... bankers.

We start today's Friday Digest with... bankers.

If you know a Wall Street banker, call him. He deserves hearty congratulations. According to financial-software firm Dealogic, bankers around the world this year produced the largest amount of "M&A" activity on record. That's "mergers and acquisitions" – or, in plain English, that's when one company buys another, usually after borrowing a lot of money. This year, bankers organized almost $5 trillion worth of deals. That's even more than the last peak in M&A activity (2007), when a little more than $4 trillion was "inked."

![]() Interestingly, this tally doesn't include recent massive increases to "internal M&A." That's when bankers convince companies to borrow massive sums of money to buy their own stock. Since 2009, $2.3 trillion has been spent on share buybacks... and not all of this money was spent wisely. On the other hand, most of it was borrowed. As a result, the amount of corporate borrowing as a percentage of our economy is at a new all-time high, almost 50% of GDP.

Interestingly, this tally doesn't include recent massive increases to "internal M&A." That's when bankers convince companies to borrow massive sums of money to buy their own stock. Since 2009, $2.3 trillion has been spent on share buybacks... and not all of this money was spent wisely. On the other hand, most of it was borrowed. As a result, the amount of corporate borrowing as a percentage of our economy is at a new all-time high, almost 50% of GDP.

![]() Bankers are also having a field day in the auto industry. In the second quarter of this year, 86% of new vehicles and 56% of used vehicles were purchased with loans. The length of these loans reached 67 months and 62 months, respectively. Auto lending has soared over the last five years, with loan totals outstanding growing by 44% to more than $1 trillion. For the first time ever, Americans collectively hold more auto loans than mortgages.

Bankers are also having a field day in the auto industry. In the second quarter of this year, 86% of new vehicles and 56% of used vehicles were purchased with loans. The length of these loans reached 67 months and 62 months, respectively. Auto lending has soared over the last five years, with loan totals outstanding growing by 44% to more than $1 trillion. For the first time ever, Americans collectively hold more auto loans than mortgages.

Who is borrowing all of this money? Anyone who can fog a mirror. More than $110 billion worth of "subprime" auto loans were underwritten in the last six months, with $70 billion of that amount going to "deep" subprime borrowers. That means 40% of all car loans being made this year are to subprime borrowers. These loans typically have interest rates as high as 20% annually.

What kind of a person borrows money at 20% annually for more than five years to pay for a used car? Someone who has no incentive to repay the loan. Calling that deal a "loan" is a misnomer. It's a lease with zero residual value. The borrower will never have any equity – nothing is at stake for him. He doesn't even have to return the car... they'll send a tow truck.

![]() And so... less than 10 years after we lent $600 billion to subprime homeowners (and nearly destroyed the world's economy), we're doing exactly the same thing with auto loans that contain zero equity. What could possibly go wrong? Shareholders of Santander Consumer USA (SC) – one of the largest subprime auto lenders – are about to find out.

And so... less than 10 years after we lent $600 billion to subprime homeowners (and nearly destroyed the world's economy), we're doing exactly the same thing with auto loans that contain zero equity. What could possibly go wrong? Shareholders of Santander Consumer USA (SC) – one of the largest subprime auto lenders – are about to find out.

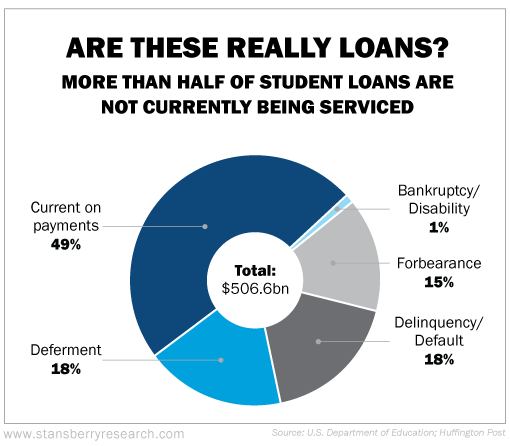

![]() The situation in auto loans is dangerous. But the situation developing in student loans is much worse. Here, loan totals have grown enormously – with wild abandon – over the past decade. The total amount of student loans has doubled since 2009, to more than $1.3 trillion. And why shouldn't students borrow money like mad? Much like subprime car buyers, they have no intention to ever pay it back.

The situation in auto loans is dangerous. But the situation developing in student loans is much worse. Here, loan totals have grown enormously – with wild abandon – over the past decade. The total amount of student loans has doubled since 2009, to more than $1.3 trillion. And why shouldn't students borrow money like mad? Much like subprime car buyers, they have no intention to ever pay it back.

As you can see in the following chart (based on one recently published by the Huffington Post), the U.S. Department of Education reports that 51% of students are currently not servicing their debts. That's from data compiled last year. Since then, the number of students getting deferments has soared, thanks to aggressive marketing of Obama's various college-loan programs. Not surprisingly, students who take deferments are much more likely to eventually default.

![]() Yes... times have rarely been better for bankers. In total, household borrowing has climbed back to $12.1 trillion − the highest level in five years − with balances growing across the credit spectrum once again, including mortgages and credit cards. Happy days.

Yes... times have rarely been better for bankers. In total, household borrowing has climbed back to $12.1 trillion − the highest level in five years − with balances growing across the credit spectrum once again, including mortgages and credit cards. Happy days.

On the other hand... if you know a big-shot hedge-fund manager... send flowers.

Many of the world's biggest hedge funds have seen significant losses this year. David Einhorn (of Greenlight), William Ackman (of Pershing Square), Larry Robbins (of Glenview), and even Dan Loeb (Third Point) have all seen big losses.

Several prominent funds have even shut down – including funds run by successful groups, like Fortress and Carlyle. Altogether, around $100 billion in capital has left the industry as a whole, the biggest decline since the 2008 crisis. As a result, more capital is now invested in exchange-traded funds (more than $3 trillion) than in hedge funds!

![]() And if you're friends with Warren Buffett... better send a coffin. Buffett is getting killed this year. Berkshire Hathaway owns around $125 billion worth of 48 different common stocks. But his top 10 holdings make up the vast bulk of his investments (more than $100 billion).

And if you're friends with Warren Buffett... better send a coffin. Buffett is getting killed this year. Berkshire Hathaway owns around $125 billion worth of 48 different common stocks. But his top 10 holdings make up the vast bulk of his investments (more than $100 billion).

Out of these 10 stocks, only one (Phillips 66) is up this year (up 24%). Coke is flat. Everything else is down – and several stocks are down big. Buffett's single biggest position, Wells Fargo (down 1%), makes up almost 20% of his portfolio – $25 billion. His Kraft Heinz position is nearly as large, at $23 billion (down 2%).

But the real damage starts at the next tier. Buffett owns $11 billion of both American Express (down 24%) and IBM (down 13%). Wal-Mart, a $3 billion position, is down 31%. Buffett also owns $4 billion of U.S. Bancorp (down 17%) and Procter & Gamble (down 16%).

On average, Buffett's top 10 positions are down almost 9% so far this year, substantially more than the Dow Jones Industrial Average's 2% decline. Looks like this will be yet another year in which Buffett can't beat the market's average, a bogey he never missed for 40 years until the late 1990s.

![]() As longtime readers know, I spend my Friday mornings trying to give you the information I'd want if our roles were reversed. And for most of this year, that has meant trying to warn you about the large and dangerous excesses I saw in consumer lending (auto loans and student loans) and the looming dangers of the next corporate credit cycle. As you might have guessed by now, I'm trying to paint the same picture here.

As longtime readers know, I spend my Friday mornings trying to give you the information I'd want if our roles were reversed. And for most of this year, that has meant trying to warn you about the large and dangerous excesses I saw in consumer lending (auto loans and student loans) and the looming dangers of the next corporate credit cycle. As you might have guessed by now, I'm trying to paint the same picture here.

![]() There's something in all of these numbers that most people will not see or ever understand – not until it's way, way too late. Our bankers have been world-class in providing more capital than ever before for corporations and consumers. They're doing a splendid job. Don't hate the bankers. They only did what the government told them to do. Besides... it's not their money. It's yours.

There's something in all of these numbers that most people will not see or ever understand – not until it's way, way too late. Our bankers have been world-class in providing more capital than ever before for corporations and consumers. They're doing a splendid job. Don't hate the bankers. They only did what the government told them to do. Besides... it's not their money. It's yours.

The trouble is, nobody – not even the world's best investors – can find a way to make a profit with all of this capital. That's a huge red flag. Declining profitability for both investors and corporations is a sign of big trouble.

A recent Barclays study shows that a decline in profit margins at public companies led to a recession in every example (except one) since 1973. And recent data show that U.S. corporations' profits fell 4.7% in the third quarter of 2015, the largest annual decline since 2009.

And here's the really interesting part of the numbers. Domestic profits were up slightly (0.4%). But declines in foreign earnings (which fell $30 billion) dragged down the results. However, the entire increase in domestic profits came from banks. As loan totals have grown, interest payments have, too. My bet is we can't borrow our way to prosperity.

![]() This combination of falling profits, rising interest expenses, and record levels of low-quality consumer-borrowing presages a world of hurt. If entrepreneurs and investors can't make a profit with all of the capital being created by our wonderful bankers, it must mean that far too much of the money is going to completely unproductive activities... like students studying basket-weaving and homeless people pretending to buy cars.

This combination of falling profits, rising interest expenses, and record levels of low-quality consumer-borrowing presages a world of hurt. If entrepreneurs and investors can't make a profit with all of the capital being created by our wonderful bankers, it must mean that far too much of the money is going to completely unproductive activities... like students studying basket-weaving and homeless people pretending to buy cars.

![]() Perhaps more credit isn't what our economy needs. Perhaps too much money and credit is already floating around. Perhaps the bankers are making a killing, but no one else can because the Federal Reserve and other central banks have lowered the cost of capital too much, for far too long.

Perhaps more credit isn't what our economy needs. Perhaps too much money and credit is already floating around. Perhaps the bankers are making a killing, but no one else can because the Federal Reserve and other central banks have lowered the cost of capital too much, for far too long.

Maybe the bankers have produced tremendous excess capacity in the world's most important industries – like energy, agriculture, and technology. Maybe that's why so many corporations have seen their bonds come under distress... their profit margins disappear... and their stock prices get hammered.

![]() Maybe it would be wise to take some of this excess capital and buy something that's not so easy to create... like gold... or silver. I suggested doing exactly that (for the first time in a long, long time) this summer. You might recall that I put together a list of the 10 most promising emerging gold and silver investments I knew about through our friends at Casey Research. The report was called "Porter's 10-for-10."

Maybe it would be wise to take some of this excess capital and buy something that's not so easy to create... like gold... or silver. I suggested doing exactly that (for the first time in a long, long time) this summer. You might recall that I put together a list of the 10 most promising emerging gold and silver investments I knew about through our friends at Casey Research. The report was called "Porter's 10-for-10."

The idea was simple: Buy a diversified portfolio of 10 precious-metals businesses as a hedge against a big credit collapse in 2016-2019. The returns, so far, have been mostly good. You might not have noticed... but the gold sector is definitely coming back to life. From that portfolio, NovaGold is up 32%, Pretium Resources is up 25%, Agnico Eagle is up 17%, and Franco-Nevada is up 18%.

![]() So... is it only me? Am I just another gold bug? Maybe. Or maybe I'm exactly right: Yesterday, Standard & Poor's (one of the three main credit-ratings agencies in the world) downgraded four of America's biggest and most important banks (Bank of America, Citigroup, Morgan Stanley, and Goldman Sachs) from "A-" to "BBB+." Bank of America holds something like 40% of all retail-banking deposits in the U.S. Morgan Stanley and Goldman Sachs are the most influential and powerful investment banks in the world. And now, none of these institutions is an A-rated credit risk. That's mind-boggling.

So... is it only me? Am I just another gold bug? Maybe. Or maybe I'm exactly right: Yesterday, Standard & Poor's (one of the three main credit-ratings agencies in the world) downgraded four of America's biggest and most important banks (Bank of America, Citigroup, Morgan Stanley, and Goldman Sachs) from "A-" to "BBB+." Bank of America holds something like 40% of all retail-banking deposits in the U.S. Morgan Stanley and Goldman Sachs are the most influential and powerful investment banks in the world. And now, none of these institutions is an A-rated credit risk. That's mind-boggling.

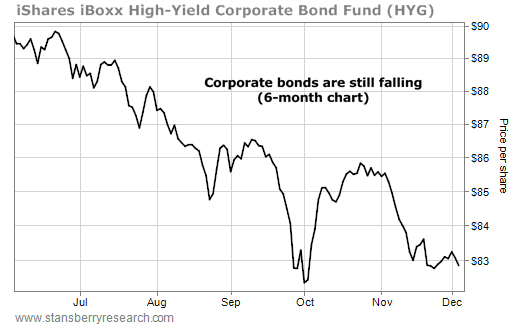

![]() Think about what's going to happen when people finally realize how much risk they're taking by keeping their money in these banks. Winter is coming, friends: We know the default rate on corporate debt has already doubled this year. We know that corporate bonds have "rolled over" and are beginning to decline in price. These credit-market concerns are what sent stocks down 1,000 points back in August. Conditions have not gotten better since...

Think about what's going to happen when people finally realize how much risk they're taking by keeping their money in these banks. Winter is coming, friends: We know the default rate on corporate debt has already doubled this year. We know that corporate bonds have "rolled over" and are beginning to decline in price. These credit-market concerns are what sent stocks down 1,000 points back in August. Conditions have not gotten better since...

![]() We know hundreds of billions of dollars have been lent over the past three years to subprime auto buyers and students. These are borrowers who, like subprime homeowners, have no equity in their loans. They have no economic incentive to pay. As a result, it's almost certain that many of these loans will default in the next 36 months. If there's a recession, the default rate on those car loans will be astronomical.

We know hundreds of billions of dollars have been lent over the past three years to subprime auto buyers and students. These are borrowers who, like subprime homeowners, have no equity in their loans. They have no economic incentive to pay. As a result, it's almost certain that many of these loans will default in the next 36 months. If there's a recession, the default rate on those car loans will be astronomical.

We also know something around $500 billion worth of corporate debt that's tied to the oil industry is likely to default, too. And now we know America's four biggest and most important financial institutions have been downgraded to less than "A."

![]() This is how a huge credit-default cycle begins. It'll be as I've predicted: the largest legal transfer of wealth in history. Hopefully, you will heed these warnings. Hopefully, you have raised cash (and will continue to do so). Hopefully, you'll join us in our strategies to take advantage of the opportunities that are already emerging in distressed credit.

This is how a huge credit-default cycle begins. It'll be as I've predicted: the largest legal transfer of wealth in history. Hopefully, you will heed these warnings. Hopefully, you have raised cash (and will continue to do so). Hopefully, you'll join us in our strategies to take advantage of the opportunities that are already emerging in distressed credit.

[Editor's note: As Porter explains in today's mailbag, your chance to join our new Stansberry's Credit Opportunities ends this coming Wednesday. If you've been considering a subscription, you must act soon. Click here to learn more.]

And next Friday, I'll show you an incredible way to take advantage of distressed equities. I promise... it's something you've never done before. And nothing – absolutely nothing – makes more money during volatile periods.

![]() Oh... one more thing... I know that many of you don't read these Friday Digests every week. And I know that most of you didn't open the Friday Digest the day after Thanksgiving. (I checked our open rates, so I know.)

Oh... one more thing... I know that many of you don't read these Friday Digests every week. And I know that most of you didn't open the Friday Digest the day after Thanksgiving. (I checked our open rates, so I know.)

If you missed last Friday's Digest, you missed out on a truly great opportunity that I'm extending personally – but only to Stansberry Research subscribers. It's the perfect solution to your Christmas dilemma... It's an offer that gets you a world-class gift to give... and one for yourself, too.

And no, it's not another newsletter to read.

It's a magnificent new tool for men... a tool that has already received positive reviews from dozens of magazines and news outlets, including Details, Fast Design, Gear Patrol, and Sharpologist. Enthusiasts are calling this the most beautiful new product on the market and the highest-quality device ever built. This is the Christmas gift you'll want... and there's an easy way to get it for free.

What is it? Learn more here.

But don't delay... This exclusive offer is strictly limited to orders received before midnight Eastern time on December 7.

![]() New 52-week highs (as of 12/3/15): none.

New 52-week highs (as of 12/3/15): none.

![]() In the mailbag... a great question about our insurance stock portfolio... and a horrible situation for someone who was intentionally buying a bond he knew would default (oy vey!). Send your notes – praise or blame, we read them all – to feedback@stansberryresearch.com.

In the mailbag... a great question about our insurance stock portfolio... and a horrible situation for someone who was intentionally buying a bond he knew would default (oy vey!). Send your notes – praise or blame, we read them all – to feedback@stansberryresearch.com.

And again... if you've been considering a subscription to our new Stansberry's Credit Opportunities service, you must act soon. We will be closing the service to new subscribers this Wednesday. Click here to learn more.

![]() "You've maintained for some time that insurance companies are some of the best investments out there. But insurance companies invest their money in bonds. How will the bond crisis affect the solvency of insurance companies and your opinion of them as a quality investment?" – Paid-up subscriber Marta N.

"You've maintained for some time that insurance companies are some of the best investments out there. But insurance companies invest their money in bonds. How will the bond crisis affect the solvency of insurance companies and your opinion of them as a quality investment?" – Paid-up subscriber Marta N.

Porter comment: Great question, Marta! We wondered the same thing, so we asked our analytical team to look at every recommended insurance company in our portfolio and figure out how much exposure they have to dodgy debt. We found a wide range of risk-taking. Travelers (TRV), for example, has 46% of its portfolio in municipal bonds, an area of the market we think is super safe. Likewise, Chubb (CB) has 47% of its portfolio in muni bonds. American Financial Group (AFG), on the other hand, has a relatively high exposure to corporate debt (39%). If you receive our supplemental Stansberry Data service, you can see the full results of our insurance company bond "audit" right here.

But just to reassure everyone, I'm happy to share our core conclusion...

Only $8.8 billion of our portfolio holdings' investable assets are in securities below investment grade. To be conservative, let's assume ALL of these securities go bad. (They won't.) To be extra conservative, let's assume ANOTHER $7 billion or so of investment-grade securities also goes bad. (Hey, those ratings agencies aren't perfect.) So, extra conservatively, $16 billion is at risk. Let's assume that our companies only recover about 30% of that amount through the courts. (This is also conservative, as historical trends suggest 40%-50% recovery.)

Even in this ridiculous worst-case scenario, our companies would only lose around 5% of their investable asset bases... or around 3% of their total asset bases. Yes, this would be a disappointing development. But even a worst-case scenario would be far from catastrophic.

![]() "Interesting reading your subscriber input today on being able to buy your distressed bond recommendations. It's obvious that they paid more than your 'buy-up-to' price, since those bonds have not traded at your recommended prices since you made the recommendations (I have looked at them daily). One might say that the subscribers such as these (I know there have been many others) are holding the bond prices up. What is your comment on subscribers' buying above your price recommendations? I know that you spoke to that last week, but in a rather 'veiled' manner (I thought)." – Paid-up subscriber Dick L.

"Interesting reading your subscriber input today on being able to buy your distressed bond recommendations. It's obvious that they paid more than your 'buy-up-to' price, since those bonds have not traded at your recommended prices since you made the recommendations (I have looked at them daily). One might say that the subscribers such as these (I know there have been many others) are holding the bond prices up. What is your comment on subscribers' buying above your price recommendations? I know that you spoke to that last week, but in a rather 'veiled' manner (I thought)." – Paid-up subscriber Dick L.

Porter comment: I wouldn't suggest paying a penny over our recommended buy price. The reason is, bonds are binary. There are only two outcomes. You'll either be paid precisely what you're owed (and no more), or the bonds will default. Therefore, your returns are dictated by the price you pay. Likewise, your risk is largely dictated by the price you pay, too. That's why we work hard to come up with a buy price that we believe represents an excellent risk-to-reward profile. But... that advantage goes out the window when you ignore our price limits.

By the way, having watched the market, we know both of our recommended bonds have traded in large quantities below our buy prices. I don't know why you would say that they haven't.

![]() "I made my first bond purchase today. It's not one of your bond recommendations, but the bond price was so low I figured it was worth the risk. On pure speculation, I purchased $395 worth of Arch Coal bonds (ACI 9.875% Jun15'19 039380AJ9). I originally bought $50K of bonds for $0.49 each. I also had another order in for $250K of bonds for $0.06 each, which to my surprise was filled this morning. The problem is my trading account was suddenly missing more than $14k. Per Interactive Brokers, it is because they charged me 'Accrued Interest' (the pro-rated coupon rate that is to be paid to whoever I bought the bonds from). This doesn't make any sense to me. Shouldn't I be the one receiving interest payments? This is not a stock. If I am the bond holder on the payment date, I should receive all the interest.

"I made my first bond purchase today. It's not one of your bond recommendations, but the bond price was so low I figured it was worth the risk. On pure speculation, I purchased $395 worth of Arch Coal bonds (ACI 9.875% Jun15'19 039380AJ9). I originally bought $50K of bonds for $0.49 each. I also had another order in for $250K of bonds for $0.06 each, which to my surprise was filled this morning. The problem is my trading account was suddenly missing more than $14k. Per Interactive Brokers, it is because they charged me 'Accrued Interest' (the pro-rated coupon rate that is to be paid to whoever I bought the bonds from). This doesn't make any sense to me. Shouldn't I be the one receiving interest payments? This is not a stock. If I am the bond holder on the payment date, I should receive all the interest.

"Now, I fully expect ACI to file chapter 11 bankruptcy, and I don't expect them to pay the coupon that is due this month. I figured that throughout the course of the bankruptcy, no matter what happens, $300K in bonds has GOT to be worth more than $395. If nothing else, they will issue me a portion of the $300k in newly reorganized stock. Even in the worst case scenario I figured I would lose $395 plus $90 in commissions. When I decided to make this bond purchase, I NEVER, EVER expected that I would get charged over $14k in interest upon the purchase of the bonds. I am expecting a call from a manager at Interactive Brokers tomorrow morning. I am going to get his response and explanation in writing. I think I am going to need a good securities attorney. Does this make any sense to you? Have you ever heard of this?" – Paid-up subscriber Bryan T.

Porter comment: I wouldn't bother with the attorney. Anytime you buy a bond, you're responsible for the interest the former holder had accrued but had not yet been paid, on a pro-rata basis. Normally, that's not a big deal, as coupon payments are typically made twice a year and, unless a bond is extremely distressed (like these), the accrued interest doesn't amount to much. I feel bad for you in this situation – that's expensive tuition. Please note that we show accrued interest in our deal box when we outline exactly how each recommended bond deal should unfold.

But... that really misses the point.

Accrued interest is one of the main reasons you must avoid a bond that's going to default. And avoiding defaults is pretty much the first thing I stressed to all of our readers in the essays I wrote about bonds. Likewise, I stressed repeatedly that investors who went out and just bought the riskiest bond they could find would probably get killed.

And – not to belabor the point – I also stressed repeatedly the importance of picking up the phone and talking to a bond broker to make sure you understood the mechanics of the trade. The next time you think you've found free money in the markets, it's probably better to try buying one share or one bond and see what happens. If it looks too good to be true...

![]() "My discount broker Scottrade was not listed when Schwab, Fidelity and TDAmeritrade were mentioned for bond purchases. I have been with Scottrade for some time now and have been very happy with their website, their local office as well as their national call center. I did have a glitch I want to share with everyone. When trying to make my first on-line bond purchase (this can be done without making any phone calls by the way) I was mistakenly told to retrieve the bond with the CUSIP number then enter how many bonds I wanted to purchase and click on the Buy button.

"My discount broker Scottrade was not listed when Schwab, Fidelity and TDAmeritrade were mentioned for bond purchases. I have been with Scottrade for some time now and have been very happy with their website, their local office as well as their national call center. I did have a glitch I want to share with everyone. When trying to make my first on-line bond purchase (this can be done without making any phone calls by the way) I was mistakenly told to retrieve the bond with the CUSIP number then enter how many bonds I wanted to purchase and click on the Buy button.

"Their fixed income department would send me a quote. This was incorrect and actually caused an immediate purchase without prior verification of the price. When I saw this happen I called Scottrade and was advised I was given an incorrect procedure. This representative walked me through the correct screens whereby you retrieve the bond then enter the amount wanted followed by clicking on a Bid Wanted button.

"I have since tried this procedure and it is flawless. I received an email within 15 minutes advising me to log on and check the quote under the Order Status area. I did this and was able to either continue with the purchase if the price was acceptable or cancel. So I continue to be very satisfied with the service and fee schedule of this discount broker." – Paid-up Subscriber Tom G.

Porter comment: Good to know. Thanks for the review of Scottrade.

![]() "I don't normally write in but have been a subscriber for many years and have seen your company's offerings evolve. I have made money and also lost money with your company's various newsletters. Over time I have learnt to do more research and take the recommendations as a beginning rather than an absolute... In any case I am writing for two reasons. Firstly congratulations on your new venture, OneBlade. I think it shows great entrepreneurial thinking and is a good way to leverage your subscribers. I have taken you up on your offer and am eagerly waiting to see and use the product as is my son, as I took up the offer for 2. I would ask you to look at the shipping element of the blade subscription as there is no option but FedEx and this more than doubles the cost of the blades when shipping to the UK!

"I don't normally write in but have been a subscriber for many years and have seen your company's offerings evolve. I have made money and also lost money with your company's various newsletters. Over time I have learnt to do more research and take the recommendations as a beginning rather than an absolute... In any case I am writing for two reasons. Firstly congratulations on your new venture, OneBlade. I think it shows great entrepreneurial thinking and is a good way to leverage your subscribers. I have taken you up on your offer and am eagerly waiting to see and use the product as is my son, as I took up the offer for 2. I would ask you to look at the shipping element of the blade subscription as there is no option but FedEx and this more than doubles the cost of the blades when shipping to the UK!

"Secondly I wanted to thank you personally on your recent series on Bonds. I found it very informative and a good addition to my financial arsenal. Unfortunately I am not in a position to take up the subscription as it is. Is there a way it could be added to my current subscriptions by dropping one of the other letters and paying some additional funds? Anyway, thank you for your efforts to help people learn the financial pitfalls of investing." – Paid-up subscriber D.J.

Porter comment: Regarding OneBlade, thanks for your business. I'm excited for you to see and use the product. I'd love your feedback about that, too. I'll talk with OneBlade's management team about shipping options. For a small company like ours, it may not be possible to offer multiple shipping choices, simply because we don't have a large fulfillment staff yet. But it's definitely something we will look to build out – including a separate European customer center with blades shipped directly from Japan.

In regards to subscribing to our new Stansberry's Credit Opportunities newsletter, the offer ends this coming Wednesday and, unfortunately, the direction I'm taking the business next year (to be far less promotional) means that it probably won't be offered for sale again for several months.

But call our customer-service office Monday through Friday between the hours of 9 a.m. and 5 p.m. Eastern time and see if one of our representatives can credit your account for the products you're no longer using and apply those credits toward a subscription to the new bond letter. I'm sure our representative will do whatever he can to help you get the product you want. The customer-service department's phone number is (888) 261-2693. For international subscribers, the number to dial is (443) 839-0986.

Regards,

Porter Stansberry

Baltimore, Maryland

December 4, 2015

|