Why we are 'stepping up' the heat on Devon's management...

Why we are 'stepping up' the heat on Devon's management... You can't fix stupid... Devon's response... How you can help – and double your money in the process... Paging Uncle Icahn...

Longtime readers are by now familiar (aka, exhausted by) our penchant for lecturing in the Friday Digest.

Longtime readers are by now familiar (aka, exhausted by) our penchant for lecturing in the Friday Digest.

We feel compelled to tell you what we would want to know if our roles were reversed. Frequently – more often than you would probably believe – this basic desire to simply tell you the truth gets us into hot water with our customers.

More people call on Monday to cancel their subscriptions and demand their money back than on any other day. They frequently cite these Friday Digests as the cause. There is no doubt in my mind that what follows will set a new record for cancellations and refunds...

In today's Friday Digest, I (Porter) resume my lonely and (so far) fruitless efforts to convince the management of oil and natural gas producer Devon Energy to sell its Canadian oil-sands assets.

For most of you, then, this letter represents a gigantic waste of time. You rightfully don't care a whit about the intricacies of the oil business. You merely want a stock that will go up. Devon's shares have proven reluctant to do so... because of the problems I've identified with its management.

For 99% of you, the path is clear. You have no interest in supporting my quixotic quest to fix Devon. You, being vastly smarter than me, have figured out that it's far easier to avoid stupid than it is to fix it. As comedian Ron White says, "You can't fix stupid."

Nevertheless, I hope you will play along at home. If you do, you're going to learn a lot about how important (and valuable) it can be to manage assets in a business correctly. You'll learn a lot about the oil business. And I believe you will almost certainly make a lot of money.

Sooner or later, Devon management will take my advice. Whether the current leadership comes to its senses or other investors take over the company's board and force them out... the choice is up to them. But believe me, activist investors like T. Boone Pickens and Carl Icahn will read this letter. The opportunity to make a quick 50%-100% in a safe stock like Devon is going to attract a lot of capital.

And if the current managers think they will survive the company's current deeply discounted stock prices simply because they control a large company... they're simply wrong. Look back at the takeover wars of the 1980s, and you'll find plenty of activity against large oil companies.

Why is Devon's management team particularly vulnerable to an activist investor? The board of directors and the management team of Devon own almost none of the stock. Insiders as a group only own 6% of the shares. As a result, their incentives are skewed. Their jobs are worth more to them than the productivity of the assets they manage. So they're motivated to pile up assets and protect their jobs. They're encouraged to do so regardless of the profitability of the assets in question. So not surprisingly, Devon's managers have amassed a huge pile of marginal assets in Canada.

Let me show you the huge damage this does to us, the shareholders.

Currently, Devon's market capitalization is only 1.4 times its book value. Don't let the jargon confuse you. All this means is that the total value of all of Devon's shares trade at a tiny premium to the estimated current value of its proven reserves and other net assets. Oil companies with excellent prospects normally trade at a more substantial premium to book value. EOG Resources, for example, currently trades for 3.5 times its book value.

As you likely know, the nominal price of a stock doesn't tell you much about its quality or value. In the oil industry, the price-to-book-value ratio tells you far more about the quality of the company. On average, U.S. exploration and production companies carry a book value of almost 2.5 today. The market believes these stocks are worth more than twice their current net asset values (based mainly on proven reserves).

At 1.4 times book value, Devon is valued at an amount that's far below average. Only a handful of the top 75 North American oil and gas production companies get less respect from investors. And nearly all of these – notably Hess, Chesapeake, and Marathon – have seen their management teams replaced. Our bet: Devon is next.

The book-value ratio is a "big picture" way to quickly compare asset and management quality across the oil business. But it's not the best way...

In our Stansberry Data service, we analyze every major oil and gas exploration company in North America on a monthly basis. Rather than merely looking at book value, we also factor in the company's production costs. Through this analysis, we deemed Devon's stock to be the cheapest well-financed oil company in the world.

Well-financed, by the way, doesn't mean well-managed. Devon's stock ended up this cheap because of some extremely bad decisions by the previous management. Devon's current management has sold more than $20 billion of assets over the last dozen quarters.

We recommended Devon in Stansberry's Investment Advisory in August 2012 after the current management began to sell assets and restructure. We anticipated that the market would soon "re-rate" the value of the remaining business. That hasn't happened... yet. Why not?

Differences in valuation across oil companies are mainly driven by the quality of the management teams and the profitability of the assets.

Take EOG, again, for example. Even though Devon holds almost $20 billion more in assets than EOG, Devon's market value is only $30 billion. EOG's market cap is nearly twice as large ($57 billion). If Devon's shares were valued by investors like EOG's shares (at 3.5 times book value), Devon's share price today would exceed $100 – instead of sitting near $70.

EOG has operating margins of nearly 25% and annual returns on equity above 15%. Devon can't match these figures. Its operating margin is less than 20% and its returns on equity are around 7%. Devon must live with these figures because so many of its assets – largely Canadian oil sands – aren't as productive.

The market places nearly twice as much value on EOG's assets as it does on Devon's for a simple reason: EOG's assets are worth twice as much.

Sticking it out in the Canadian oil sands is a stupid choice. We want Devon's management team to sell its marginal Canadian oil-sands assets and focus on its highly profitable assets in Texas, specifically oil production in the Eagle Ford Shale and Permian Basin regions. If it will do so, the market would quickly value its stock more like EOG's because it would be far more profitable. We know this by looking at data that Devon provides all investors...

Here are the key facts. Last year, Devon earned gross profit margins of $30 per barrel from its Canadian oil-sands operations. Meanwhile, it earned gross margins of $77 per barrel on its U.S. oil production. You see, Canadian oil sands produce "bitumen," a heavy, low-quality crude. Unlike drilling for conventional oil, producing bitumen involves digging the tarry mud from the ground and heating it to separate the hydrocarbons.

Bitumen trades at a substantial discount to the benchmark for U.S. oil prices, West Texas Intermediate ("WTI") crude oil. In the first six months of this year, bitumen was fetching around $60 per barrel on the spot market, while WTI was worth more than $100 per barrel.

In addition to this big price discount, Devon's operating costs in Canada are twice its production costs in Texas. You don't need a PhD in math or geology to grasp the problem: Higher operating costs and lower production value mean Devon will never make much money (if any) producing bitumen in Canada. And these investments will never compare with its opportunities in Texas.

Here's what's even worse. According to sources at the company, the bitumen Devon is producing in Canada has never been used as an energy source. Instead, most of the company's production is processed into asphalt and used on roads and roofs.

And... guess what the No. 1 input cost is to produce roof tar (bitumen) at Devon's Jackfish properties? Natural gas. Yes, that's right. Devon is spending billions – $2 billion a year currently and more than $10 billion overall – to build out a roof-tar mine, while consuming a globally valuable energy source to produce it.

Currently, about a dozen liquefied natural gas (LNG) export facilities are being built in North America. They will enable the U.S. to export about 35% of its natural gas production. We believe this coming export demand, plus a major shift from coal to natural gas as fuel stock for electricity generation, will cause the price of natural gas to soar relative to crude oil.

If we're right about this trend (which has been happening since 2012), Devon may soon find that it can't make a profit producing bitumen because the required natural gas is simply too expensive. If the price of natural gas goes back to more than $10 per thousand cubic feet (mcf) – which we view as nearly a sure thing, eventually – we doubt the company can earn a profit on its Jackfish investments.

How do you "fix stupid"? If we took over the company, here's exactly what we would do: Devon's Canadian oil-sands assets are worth at least $10 billion, based on the company's expectation of $1 billion a year in free cash flow after the completion of Jackfish No. 3 operation.

Using those assets as primary collateral, Devon could borrow $10 billion and buy its own stock. It has 400 million shares outstanding. They trade at $70. Devon could afford to buy 142 million shares. The company could do this immediately. Doing so would reduce shares outstanding by 35%. The Canadian oil sands could then be sold over the next year and the loan repaid. This reduction of outstanding shares and the resulting re-rating of the stock higher (based on the high quality of the stock's remaining assets) would lead to a 50%-100% increase in stock price.

An even more elegant solution would be to retain a small royalty on the oil-sands sites. At some point, high oil prices might make production there valuable. This strategy would recoup most of the capital invested in the project and also retain a royalty interest that would allow Devon to greatly increase the profitability of its asset base... which would greatly increase the value of its stock.

So far, though... rather than taking either of these actions... the company has merely responded to our work by making confused (and in some cases, deliberately misleading) replies to disgruntled shareholders. In a letter that we saw from Devon to an investor, the company claimed that: "a balanced portfolio of light oil, heavy oil, natural gas, and natural gas liquids will provide the best opportunity to generate the highest returns."

Oh, please. No oilman in the United States would argue that including oil-sands assets in your portfolio is likely to increase your return on assets. This statement is either a blatant lie or evidence of serious mental illness in the CEO's office. Get some help. Seriously.

But the letter went on... "While shale-oil plays have increased U.S. oil production in recent years, our nation still must import more than 6 million barrels of oil per day, largely heavy and medium-grade crude. In light of that, we are confident in the long-term demand for energy from Alberta."

Remember, Devon Energy in 2001 purchased Mitchell Energy, the firm that pioneered horizontal drilling and hydraulic fracking technologies that led our country forward by transforming the production of oil and gas in America. This same company is now making the argument that its best strategic opportunity lies in importing low-quality crude to America.

This argument, made by these people, must go down in the annals of American history as one of the most ironic and stupidest strategic decisions of all time. It's tantamount to smartphone maker Apple deciding to invest $10 billion in Blackberry... because some people really like those trackballs.

Perhaps the managers at Devon haven't noticed... but since July 2014, the U.S. is the largest producer of liquid hydrocarbons in the world. Yes, that's right. We're now producing more petroleum than Saudi Arabia. And... guess what? Nobody is planning to invest $10 billion to import oil to Saudi Arabia.

But Devon's management wasn't through. Its letter continued...

Heavy oil, including the bitumen we produce at Jackfish, is converted into a multitude of energy products, such as gasoline, kerosene, diesel fuel, naphtha and other light products. Additionally, there are several industry projects underway designed to deliver Canadian heavy oil to the U.S. Gulf Coast, as well as to the East and West coasts of Canada.

Taken together, we see the U.S. refining capacity, the increasing takeaway capacity and the global demand for crude oil as very likely contributors to improved pricing for synbit and dilbit barrels out of Canada.

According to my sources at the company – direct and emphatic statements made directly to me – not a single barrel of Devon's Jackfish production has ever been refined into a fuel stock. Not a drop. But beyond this issue, it is delusional to believe that the capital to build pipelines from Edmonton in Alberta, Canada to the U.S. Gulf Coast can be raised when we're already transporting 500,000 barrels per day from the North Dakota's Bakken Shale oilfields. That's up from 9,500 barrels per day in 2009. And this growth will continue for at least a decade.

North Dakota is a lot closer to the Gulf Coast than Edmonton. Just because heavy-oil refining capacity exists on the Gulf Coast does not mean that supplying it is the highest and best use for your company's assets.

Maybe you've noticed that Targa and others are making a killing by exporting the same resources you're producing in the Permian and Eagle Ford. Even more so than the Bakken, these resources are dramatically closer to the Gulf Coast and the world's export markets. Instead of building a giant straw to Canada's low-value crude, why not start exporting your own propane and butane to the world, which is happy to pay top dollar to get it? This is basic economics.

Devon's management also wrote...

With the completion of Jackfish 3, we begin an era of free cash flow from our Jackfish complex. These projects have the potential to generate approximately $1 billion annually for many years, after maintenance and other capital requirements. Importantly, assuming the current commodity price and cost environment, we see our Jackfish complex generating full-cycle returns of greater than 20 percent over the life of the projects...

Devon's management is making assumptions about commodity prices that have no basis in reality or in history. Its core assumption is that natural gas prices will remain low, and it knows (or should know) that's not going to happen.

Natural gas prices have always been radically volatile. We ran a simulation based on Devon's operating model in Canada. Rather than use then-current commodity prices (2013), we plugged in the actual commodity prices from the 20 years before Devon began making investments into Jackfish. Our simulation – based on actual, historic prices – showed an average profit of $3.24 per barrel, about one-tenth the $30-per-barrel Devon projects.

If the price ratio between natural gas and crude oil drops back to a more traditional range on an energy equivalent basis (and it seems to be doing just that), Devon would end up making $100 million a year in cash flow, before Canadian taxes... not $1 billion. And the return on investment will fall to around 2%. If the actual results are that good, we would be shocked.

So Devon is taking a lot more risk than it's willing to acknowledge. That's a bad sign. But more important, the return on investment that's available right now in Texas is vastly higher. EOG reports that it was able to earn back 100% of its total costs on its Eagle Ford drilling campaign last year. Surely Devon's managers have noticed how much more profitable it can be to drill an oil well in Texas than try to cook oil out of a mud bog in Canada?

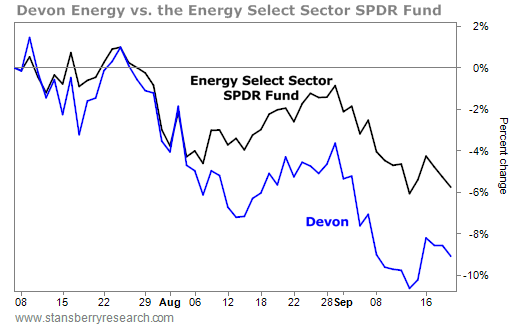

In summary... at the moment... with a large chunk of the company's assets earning almost nothing in an effort to convert oily mud into energy, the company's shares have suffered a serious decline over the last 90 days (since we published our first letter urging Devon to sell its oil-sands assets).

Devon is down 10%, the Energy Select Sector SPDR Fund (XLE) – a basket of independent U.S. oil producers – is only down about 5%. That's because falling oil prices make it much, much more difficult to make even an operating profit selling roof tar.

These trends will continue until Devon takes decisive action to improve the quality of its assets and its operating performance.

British social critic Bertrand Russell once famously observed: "Many men would rather die than think; many do." The capitalist corollary goes as thus: Many CEOs would rather be fired than admit a mistake; many have been.

John Richels (Devon's CEO)... if you're reading this... don't wait until your secretary tells you there's a Mr. Icahn on Line 1. By that point, you will have no room to maneuver. Trust me, Larry Nichols (Devon's founder) isn't going to take the fall for the Canadian losses. They're yours. But it's much, much better to own them now, while Devon is doing well, than to end up being forced to unload them later, at much lower oil prices.

As a lone voice – a newsletter, no less – I have little influence with the board of directors at Devon. But currently, almost 500,000 people read the S&A Digest. Many of you are Devon shareholders. All of you should be Devon shareholders.

Devon owns tremendous assets – especially in the Permian Basin. It is developing into one of the world's great energy companies. It is a cheap stock. It will continue to thrive... as soon as it starts making better capital-allocation decisions.

It's also likely that at least one or two major investors pick up this banner. Perhaps some already have. I know my arguments resonate well with experienced and knowledgeable institutional investors. As dear ol' Obama might say, "Change is coming to Devon." And unless he acts fast, it ain't going to be a change that the CEO likes much.

Here's what I need you to do. First, read the July issue of my Investment Advisory. I've put an "unlocked" copy of the issue here. You can link to it in e-mails to friends and associates. (We don't normally share our work this way, but I believe what's happening with Devon is more important than our copyright on this particular letter.)

Think about our arguments. Ask yourself if they make sense. Talk with your investment advisor. Show him our letter. Ask him to think about it, too. Show the letter to your friends – especially anyone experienced in business, investing, or the oil and gas industry. Ask: Do Porter's arguments add up?

If you can find anyone who's reasonably intelligent and experienced in business or investing that disagrees with me (outside of Devon's management team), don't buy the stock. And be sure and forward his or her arguments to me. There's nothing better than having thousands and thousands of other investors review and check my work.

But here's the thing. You won't find anyone who can refute these arguments because they're nothing more than facts and common sense.

No amount of capital is going to make the Canadian oil sands a better investment than the oil shale in Texas. No amount of pipeline is going to be a better investment than exporting Devon's propane and butane. And there is no better way to move the stock forward quickly than by selling the Canadian assets and buying back more stock.

If you do agree with me and buy the stock (or if you already own it), I need you to write a letter to the non-management members of the board. You can reach them directly by sending U.S. mail to:

Non-Management Directors

C/O Office of the Corporate Secretary

Devon Energy Corp.

333 W. Sheridan Avenue

Oklahoma City, Oklahoma 73102

Or by e-mail: nonmanagement.directors@dvn.com.

It would be best to send a copy of your letter through both channels – e-mail and U.S. mail. People tend to take "real" mail more seriously, especially in big corporations.

I urge you to make sure your letter does three things...

First, please tell the non-management directors that you would like to see Devon greatly increase its operating margins and its return on equity by continuing to sell its low-margin operations, most importantly, its Jackfish Canadian oil-sands operations.

Second, remind them that nearly all of the other management teams at similarly positioned, low-margin energy producers (like Chesapeake and Hess) have been replaced because they were not responsive to investor demands to improve results.

Third, note the number of shares you hold and how long you've been an investor. Finally, tell the board that you plan to vote against ALL of the incumbent directors next year unless immediate changes are made to improve Devon's profitability by selling the Canadian oil-sands project.

This last part is most important. Nobody who sits on a board wants to be voted against. It is embarrassing, and it is our greatest weapon in forcing change at Devon. You must make sure that you vote your shares when the proxy materials are sent out. And you must vote "no" against all of the incumbent members of the board and any of their nominees. As individuals, our votes hardly count. But if every reader of my newsletter votes "no," it will have a substantial impact.

The proxy materials will be sent to you next spring – usually in April. You will have until June 2015 to vote. You also can do so online at: www.proxyvote.com. I will remind you about all of this when the time comes next spring. Until then, just make sure to send the company a letter and let them know that you will be voting no against every board member. Believe me, this will definitely get their attention. Most individual shareholders never respond to proxy voting matters.

One last thing... please send me a copy of the letter you write to Devon. You can copy me on your e-mail (feedback@stansberryresearch.com). This will give me some idea of how many of my subscribers are participating in this shareholder uprising. Thanks very much for your help.

I will be speaking about Devon at the upcoming New Orleans Investment Conference. It is being held at October 22-25. To learn more about the conference and register to attend, click here.

I'll also be appearing alongside former Federal Reserve Chairman Alan Greenspan during a panel I don't think you'll want to miss.

Remember: You can't fix stupid. But you can ask him a bunch of questions he can't answer honestly.

New 52-week highs (as of 9/18/14): Berkshire Hathaway (BRK), Discover Financial Services (DFS), WisdomTree Japan Hedged Equity Fund (DXJ), iShares U.S. Insurance Fund (IAK), Johnson & Johnson (JNJ), KLA-Tencor (KLAC), Eli Lilly (LLY), Medtronic (MDT), 3M (MMM), Altria (MO), Pepsico (PEP), PowerShares Buyback Achievers Fund (PKW), PowerShares QQQ Fund (QQQ), ProShares Ultra Technology Fund (ROM), RPM International (RPM), ProShares Ultra Health Care Fund (RXL), ProShares Ultra S&P 500 Fund (SSO), Steel Dynamics (STLD), Skyworks Solutions (SWKS), and W.R. Berkley (WRB).

In today's mailbag, a subscriber shares a sign of the top in bond markets. What signs of a top do you see? Send your thoughts to feedback@stansberryresearch.com.

"I am sure that you are all over this story but...

"Friday morning, Twitter said it raised $1.8 billion in the convertible bond offering it announced earlier in the week, up from the $1.3 billion it planned to raise as the deal met with robust demand.

"The five-year tranche of the offering, with notes due in 2019, carried a 0.25% interest rate, while the seven-year 2021 notes bear 1% interest, payable semi-annually in March and September.

"The conversion rate, 12.8793 shares per $1,000 in principal, is equal to about $77.64 per share, according to Twitter's filing. That is almost 48% above the stock's $52.57 level Friday morning.

"Talk about a sign of the top in the debt markets. Twitter, a company that is poorly managed (Peter Thiel's words, not mine) and can't make any money issuing nearly $2 billion of debt. The issue created so much excess demand they raised an additional $500 million. And the yield is puny at just 0.25% on a 5-year note. Sure, convertible debt is supposed to yield less because of the equity conversion 'kicker,' but this is just insane. The stock needs to rise 50% for the conversion to make any sense! Pure madness." – Paid-up subscriber Ross Slaneff

Regards,

Porter Stansberry

Baltimore, Maryland

September 19, 2014